15 is the magic number

With the conclusion of a busy week in the markets, I take a look at 15 charts broken into my Fundamental, Behavioral, and Catalyst buckets

The image above is of Jackson Hole, Wyoming, where central bankers from around the world met to discuss “Structural Shifts in the Global Economy.” It really was a bit of a non-event all in all, however, there were some words from Jay Powell:

Jay Powell clarified three things in my mind: 1. The FOMC is NOT moving it’s inflation target from 2% to 3%; 2. The FOMC is not going to hike in September but there is a chance of it in November or December; 3. Interest rates overall are going to stay higher for longer.

The markets largely did not pay attention to his words. There were some small moves in the Fed Funds futures market pricing some odds of cuts out of the curve. The market is still not where the Fed dot plot is and Jay Powell sounds like he is the most hawkish dot on this plot. You can see that over the last 2 months, the market is moving closer to where the Fed is and is beginning to embrace this higher for longer message which is an important one.

The key to the labor market message is coming down to the wage negotiations, with the United Auto Workers the next up. The talk is there will be a strike, which could shave economic growth in addition to keeping inflation sticky.

After getting through Jackson Hole and some more earnings reports, I thought I would quickly run through what the three buckets I follow are currently saying.

FUNDAMENTAL

The Fundamental bucket is the core trend. I have been downbeat due to Fundamentals all year and I still am. Yes, we haven’t had an economic slowdown yet but this still looks to be the most likely scenario in my mind. Let me run you through why I think that still.

First, I mentioned higher for longer above. The pink line here is the difference between Fed Funds and CPI. Restrictive policy is keeping rates well above the inflation rate and trying to bring inflation down further. When policy has gotten restrictive like this in the past (areas that are circled), what have we seen with both the stock market and GDP? We have seen meaningful declines. No, the stock market did not anticipate this so I don’t think you can see we had the big decline last year as many are saying. I still think this is still to come.

Another way to consider this is in financial conditions. That line is in white (and inverted here) showing that conditions had gotten easier in the first part of this year but might be getting tighter again. When we have seen tighter financial conditions, it typically has meant lower stock prices and higher Treasury returns. We have seen the opposite this year because conditions have gotten easier. If they tighten, we could see a re-allocation in markets.

We are getting more headlines that consumers are starting to get tapped out. Consider this headline on credit card delinquencies. Not at a dire level yet, but all trending in the wrong direction if we think the economy is going to get better from here.

I also wrote about this on Linked In this week, discussing the earnings we saw from retailers,:

Chart of the Day - US consumer

Earnings are still ongoing believe it or not. This week is particularly heavy for retail and consumer discretionary stocks that are reporting post the back to school spending that we got at the end of the summer

I am old enough to remember the retail sales number on August 15 that was much better than expected and got the mkt so excited about a soft landing, or even no landing, that it began to worry about more rate hikes

However, as we get thru the earnings reports from the companies selling into the US consumer, the picture seems to be a little different. I have put a collection of companies that have reported in the chart today

You can see that basically all of them are lower over the last year, some of them sharply so. The one that had been doing the best was Dick's, but it had a shocker yesterday, dropping 30%. Sales are down. Even scarier, they say theft was up

Today Foot Locker, used to be a big place for back to school, said trends are negative, so negative they are cutting their dividend. The chart isn't even picking up the 20% fall in pre-market

It isn't just back to school. It is across the board. Best Buy, Target, Macy's, VF Corp, AMC Entertainment. Nothing but negative news on the trends they are seeing from the consumer. Macy's also pointed to the 'shrinkage' though it also sounds like more theft than it is damaged goods etc.

This on the back of a bigger story last week where Gump's in San Fran is talking about closing after 166 years because of the very negative environment for retail in that city. It seems they are not alone out there

The consumer came into the year with a lot of savings. However, we are working thru those savings. In addition, we are seeing mortgage rates eat more, gasoline prices eat more, and soon, student loan debt needing to be repaid

Perhaps people are doing all of their spending at Amazon though we don't hear as much about rapid market share gains. Perhaps all of the money is being spent in restaurants. Who cares about the kids going to school, Mom & Dad need a good meal and a glass of wine!

We can find a number of reasons to explain away what we are seeing. If it was one or two names, I think we can say that those companies might be just losing share or out of touch. There is certainly some of that

However, when you hear the same thing across a number of retail names, across a wide range of product or services, we have to start to think there is a bit of a bigger issue. Definitely something to monitor

Of course, the market today will only care about Nvidia, which has become an asset class in its own. I will leave that to others to discuss

The Fundamental category is still negative in my view.

TECHNICAL

While I have been negative on the Fundamentals of the market all year, I have been upbeat on the Technical aspect of the market. I normally call this section Behavioral because I include more than just technical charts, but today I just want to quickly run through some charts for you. I think they give you a clear picture.

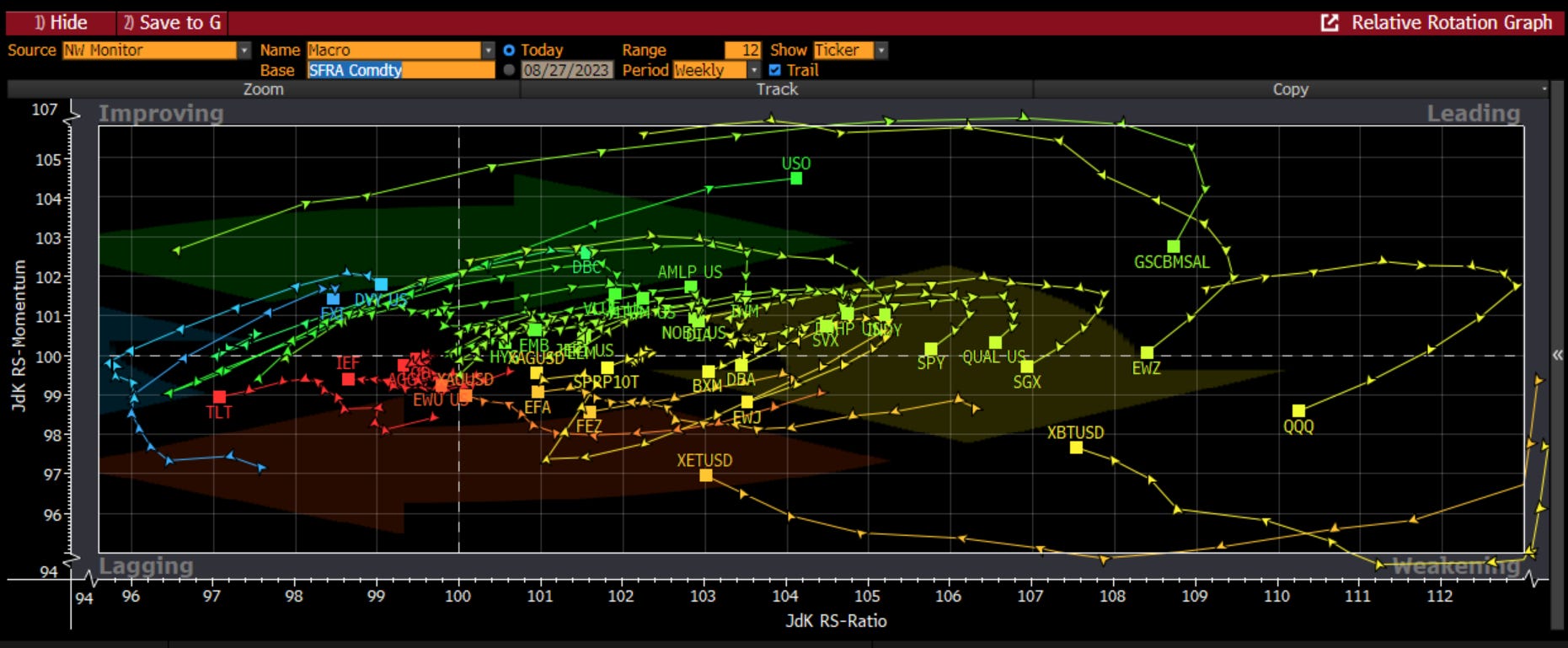

The first is a relative rotation chart that plots all macro assets against cash. We can see that the leaders of this year - QQQ, crypto, Japan (EWJ) - are all into the weakening zone. The next stop is most likely the lagging zone where we currently see the bond market. The leading category now is commodities (DBC and USO) and value stocks. It looks like we are seeing a rotation underneath the hood of the market.

The daily SPX chart suggests that there may be some near-term support around here. We can also see the daily MACD turning up so there is the potential that we might get a small bounce in the next week or so.

However, the weekly chart is giving us a different message. You can see the weekly MACD rolling over and suggesting that we might be targeting support around 4000 level or about 10% lower. This would just be a correction and not change the positive trend but it might catch a few people off guard because there is some late money that fueled the recent rally.

We can’t look at US stocks without considering tech stocks as these have been the driver all year. The weekly chart of the Nasdaq looks the same as the SPX and is suggesting support in this index is more like 14% lower. That would really sting a few people.

We can’t think about tech without looking at NVDA. In spite of earnings that were far better than even the optimists hoped for, the stock ended lower on Friday, suggesting the whisper numbers (the unofficial talk on the Street outside of published reports) were already at this level which is why the stock had rallied so much into the numbers. NVDA’s weekly chart looks the same as the NDX and is pointing to downside all within a positive trend.

Commodities have pulled back to support after breaking out and might be looking for a new move higher. This is somewhat surprising given a downbeat view on growth but we have to respect the price action. The supply/demand dynamics in several commodities favors higher prices - oil, nat gas, agriculture, copper etc.

After getting thoroughly washed out, bonds look like they might be poised for an oversold bounce. The relative strength index had gotten oversold and now the moving average convergence/divergence is turning higher. There is still a lot of resistance above, and a higher for longer message makes it tough to get too bulled up on bonds, but it does look like the worst of the bond move might be over for now.

The dollar has been looking pretty weak the past year. However, it looks like it might be breaking out now. The dollar index (DXY) is primarily Euro and Yen and it has broken above the cloud with the lagging span also breaking out. The MACD is trending higher and we are not yet overbought. Another move that looks to be consistent with a higher for longer FOMC message.

This section looks to be a bit more mixed than it has been all year long. For me, the next month or so look to be negative for risky assets like stocks and more positive for the safe havens like US bonds and the dollar. This does not suggest that the bigger picture trend higher is over for stocks, but there might be a pause to reset coming up and that is something we have to be aware of.

CATALYST

The last category is the catalyst section. This week should be pretty quiet with a long US holiday weekend approaching. For some that means an end of summer vacation. For others is probably means a lot of travel sports if they have kids. There will be very little newsflow until after Labor Day when markets start to get busier again.

I wanted to take a look at the Global Geopolitical Risk Index. This is something that is always on my radar and I checked in because I have been hearing more negative stories or rumors of late. Russia/Ukraine war is still top of mind, as is the Chinese economy. However, there is also talk that the Chinese have been stock-piling oil in possible preparation for some sort of military action. These types of risks are always present at some level and we can’t avoid investing because of them. However, we do want to have a sense of when things could get worse than normal because markets will react to changes in overall risk. We can see that the number of risk acts (yellow) is still pretty low relative to the last 10 years. However, the threats number stands out to me. This suggests a slightly more cautionary approach in my mind.

What about changes in the economic expectations. The fundamental section discusses the trend, but the economic surprise index discusses more how the data might come in relative to expectations. In the US, the data looks poised to begin to disappoint. This should not be surprising with most people on board with either a soft landing or even no landing. Anything outside of that (weaker growth, higher inflation) will be a disappointment. In other parts of the world, the opposite may be true. Could Chinese data start to improve? Is this why the commodities are acting better? Is European and Japanese data getting better? Is this why global bond yields have moved higher? Either way, I believe we get bad news for the US economy which I think corroborates with weaker stocks and strong bonds. I think commodities get driven by China and EM which both look to be better.

I mentioned geopolitical risk above but what about market risk? We can see the idiosyncratic market risk - equity volatility as measured by VIX and credit spreads - are very low and complacent. However, macro risk as measured by bond volatility (MOVE) and FX volatility (JPM VXY) are both still elevated. Could we start to see a resynchronization of these risk markets? Is it time to add some protection in equity and credit markets while it is priced inexpensively? I think so.

The catalyst section is also giving me some pause. Pulling it all together, I am feeling a little more downbeat on markets than I have been for several weeks. Again, not calling for a major collapse, however, 10%+ corrections are not uncommon and September is seasonally the single worst month for stocks and all risky assets.

With market insurance inexpensive, it might be time to look to protect some of your gains from this year. If you have been in cash, it might be an opportunity to buy some stocks at a discount. Either way, it is time to …

Stay Vigilant

Hi Richard, thank you very much for your work here and daily updates in LinkedIn. Regarding your LinkedIn Chart of the Day - more China today, I recommend you listen to MacroVoices, Dr. Anas Alhajji: 2024 Energy Markets Outlook & More July 20th, 2023.

Cheers,

Carl