A holiday-shortened week

Even though this is a 4 day week, it is the beginning of a very important stretch into the next FOMC meeting

With the holiday weekend, the official ‘end of summer’ and some time at the lake this weekend, this week will be a little abbreviated. However, I did want to collect my thoughts as we head into the post Labor Day markets, because traders and investors will be returning in earnest, desks will be fully staffed again, and volumes will return. Ahead of this, I always find it useful to look at what has happened in the last 4-6 weeks of the summer through the lens of my Fundamental/Behavioral/Catalyst framework. With the central banks being data dependent, the markets will be as well. However, not all data is relevant for the markets, with some quite lagging data often getting too much attention (I am looking at you GDP) while other data that actually leads the market (new orders) getting very little attention.

Adding to the difficulty of navigating the markets and the headlines is the positioning, which is still near extremes. Much as a stock analyst must determine both the fundamentals of a company as well as the fundamentals of a stock (what is priced in), when analyzing in a top-down perspective we have to take into account how investors are positioned for events to have a sense of how prices will respond to news.

Let’s jump into the analysis.

FUNDAMENTAL

As we think about an economy, stimulus (monetary or fiscal), flows through in a reasonably predictable pattern. A typical scenario: input prices fall, easier money available, demand starts to increase, capital spending rises, GDP rises. On the downside, it is the reverse of this: demand declines, inventories accumulate, companies slow production, employees are laid off, and finally, GDP falls. In fact, a key driver for the economy into and out of a recession is the housing market. The acronym, coined by Cornerstone Macro, is HOPE: housing -> orders -> profits -> employment. At this point in the cycle, the first slowdown we will see is housing cooling off due to higher rates, this leads to a slowdown in orders for everything from lumber to drywall to windows to landscaping. With orders falling across the economy, profitability starts to suffer and companies start to lay people off. Employment is the last measure to fall.

As we look through the data of the last week using this cycle, we can see housing as measured by the NAHB housing index has fallen and the ISM new orders data has also fallen almost coincident with that. These are the blue and white lines. The next stage has not yet begun as Q2 earnings help up better than expected and showed some small positive growth. The expectation for Q3 earnings are for a marked slowdown and we will start to get this data in October. We can see the employment picture still is solid as the Friday non-farm payroll number came in at 315k, a number that missed consensus but is still solid in absolute terms. Recessions don’t start with 315k NFP number suggesting the slowdown is pushed out for now.

Digging into the housing market data a little more deeply, I wrote this on LinkedIn this week:

“However you slice it, the data is weakening. It is now getting to where it is not just coming off the boil of 2020-2021, but moving to levels we haven't seen in some time. Let's look through a few of these measures.

In white is the FHFA house price index of price changes on purchases nationally. Price change has fallen back down to levels we have seen really in the entire post GFC period. Still not horrible but also still not bottoming. What I don't have on here (would be too many lines) but is relevant is the Case-Shiller 20 city natl average. That index tries to adjust for quality considerations as well. It is also rolling over but has not fallen nearly as much. So prices are down, how much depends on where & of what quality. Given housing affordability had gotten out of control, this should be good news for consumers & buyers, but not good for builders.

The blue line is the NAHB home builder index assessing housing conditions nationally. It has also fallen rapidly but again is in the area we saw in the 2012-14 period. Not great, but not a disaster. Yet. It also has not bottomed & so the bears are in control.

The purple line is the amount of new home sales. These constitute only 10-15% of all sales but are much more susceptible to mkt swings & are important to watch to assess mkt health. This line is back to the white horizontal line I drew, considerably below 2020. However, it is just back to 2017-18. It is well above the the 2009-16 period. It is also 1/2 that of 2005-06. This means we did not have the froth that we saw in the housing crisis. This is indicative of two things in my mind: things are just coming off a near term cyclical boil &, importantly, an indication of how much supply we are lacking. New homes in the entire post GFC period are 1/3 to maybe 1/2 of what we saw in the last housing bubble. Throw onto this that mortgages are not going to those who can't pay them back & we do not have anything that resembles the 2004-07 period.

Finally, in yellow & inverted is the 30yr mort rate. Yes, it is double where we were. However, it is back to where we were in the 2004-2007 period, a time when a housing bubble happened. This rate by itself is not indicative of a crisis. Is it an adjustment? Of course. Can and will people still buy? Yes, as long as jobs and wages hold up. To me, that is the key to watch right now. The Fed is watching that too.”

I also wrote about the jobs market this week in anticipation of the non-farm payroll report. This week alone, we got data on Job Openings & Labor Turnover (JOLT), Jobless Claims, ADP Employment Report, Challenger & Gray layoff news and ISM employment conditions in addition to the non-farm survey. Overall, across these many measures, we can see a picture of a jobs market that is solid, no longer improving, but also not slowing rapidly like other data. It is a picture that people can still find good jobs. I like the JOLT data in particular because I find it moves coincidentally with the SPX much more so than non-farm payrolls. As I said on LinkedIn – which of these is not like the others? The NFP number will be revised each of the next two months before we know the final. Even that revised number, in blue, has more noise than signal. As I said, though, we did get a more full picture across a number of other data that jobs are still holding up.

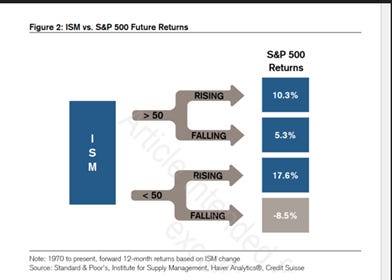

When all is said and done, we ultimately need only one chart to tell us what we need to know about the markets. This chart, courtesy of Credit Suisse, shows us the performance of markets in different phases of the ISM. The ISM (the longest measure of US PMI available) can simply be placed into one of four regimes – rising or falling, above 50 or below 50. We can see that the only regime that generates negative S&P returns on average is when we are below 50 and falling. Fund managers know that the time they can most easily beat their benchmarks are buying getting defensive, and raising as much cash as possible, when we are below 50 and falling. Right now, the S&P has negative returns year to date, yet we are still above 50, though it is falling. This is indicative, to me, that the market is pricing in a more imminent recession, than we are seeing.

As we can see, the ISM at 52.8 is still holding on above the 50 level of expansion/contraction even though the anticipatory ratio of new orders to inventories is still pointing to trouble ahead.

However, this trouble has already been anticipated by the stock market:

BEHAVIORAL

As I mentioned before, we need to also consider investor sentiment and investor positioning. I refer to these as the behavioral section because all of the behavioral finance biases that we study can be seen in these various charts. I won’t go into all of them now, but there are a few that I want to show to prove the point.

One potential hot spot that is happening before our very eyes is the budding FX war in Asia. It all began when Japan decided it wanted to import inflation. It is attempting to do this by keeping its rates pegged to a limit of 25 bps. As a result, levered account use the Yen as a funding currency, borrowing in Yen to invest abroad. Since the US and Europe are happy to find any way possible to reduce their inflation, there was not the pushback you might see from a country clearly weakening is currency. However, it did not go unnoticed by China. In response, China, which manages the float of its currency, has begun to weaken the Yuan up to and potentially through the 7.00 level. This is having a negative impact on the other currencies in the region, at a time when we have very fragile currencies in Asia. Sri Lanka and Pakistan have already fallen (the latter needing a bailout from the IMF). Veterans who remember trading the Asian Financial Crisis, which turned into the Russia/Brazil crisis and the LTCM crisis, recall it all began with China actively weakening its currency.

I looked at the impact and correlation of USD/JPY vs. other measures of risk appetite in the market. I compared the move to US 10-year Treasury yields, SPX forward EV/EBITDA and credit default swap indices. We can see as USD/JPY moves higher, we should expect higher US rates which leads to a lower multiple investors will pay for stocks, and wider credit spreads with higher credit risk. With a large capital surplus, Japanese investors notoriously send their money abroad in search of other investments. In times of market stress, the money flows back home and out of these other riskier global markets. As a result, with the FX war still ongoing, we need to be cognizant of these money flow risks.

If we look at levered funds, we can see their short position in S&P 500 futures is at the highs it has been in 5 years. This could well be because the funds are using futures hedges in their long/short book, having had to scramble and cover shorts all of August. This could well reduce as PMs look to add single name shorts with the news that comes through from the conference and then earnings season. It is hard to say that traders are overly bullish when we see this positioning.

Referring back to the expectations of the economy from investors, in the latest BAML Global Fund Manager Survey, global growth pessimism is still easing from an all-time high but it is elevated.

As is the pessimism, therefore, for profits in the quarter ahead. Investors don’t seem to have much H.O.P.E .

Thus, the cash levels are very high, just not as apocalyptically high as they previously were.

Investors cut their underweight in stocks but they are still 26% underweight. Investors are rooting for a lower market to outperform their benchmarks.

If the market is going to hold on this downdraft, this is exactly the level we should expect it to. Recall last week we suggest 392 in SPY was a likely target for the market. We are there now:

Though the weekly charts are pointing to 349 and then ultimately 318 on the downside. I had said before 3300 was going to be the low end of the range as we chop back and forth, for that to happen, the bulls have to step up right now.

CATALYST

Moves don’t tend to happen until we have a catalyst, until we get some news that either causes people to change their minds, or to dig in their heels and press their bets. After earnings in July, and then a quiet summer for family after, companies will be back on the road in earnings over the next two weeks. Below you can see a partial list of the conferences that are going on but they are happening across every sector: energy, technology, consumer, financials and healthcare. With the expectation for earnings to really slow down this quarter, investors are heading to these conferences with some reasonably negative views. Will these views be confirmed? Will it be even more dire? Or will there be reason to cover shorts and underweight positions? This is what traders will need to respond to in the coming weeks.

There is also a slew of more data including CPI, PPI, housing, regional Fed surveys and jobless claims in the lead up to the next FOMC meeting on September 21:

Finally, the geopolitical news is not getting better. It is rarely a positive catalyst for the markets, but with all of the focus on the energy prices in Europe, this news in the FT won’t help:

AFR had a story that is talking about the potential for a Lehman Brothers moment in the EU energy market, as energy firms are running out of cash to cover the losses on the mark to market of their hedges, which also may be impaired by the governments capping what they can charge to consumers. We have not heard the end of this story.

As I look at the three parts of my framework, I see the fundamental trend is holding in there but the forward-looking data is still suggesting we have some sort of recession probably in early 2023. Can profits hold up and keep markets strong through the end of the year? That is the questions on every investors minds as they head to the various conferences occurring in the next 2-3 weeks. Investors are already positioned for a recession if we look at both levered and long only positioning, in addition to the performance of the market already this year. However, the bears are in control of this tape as we saw from the late day move lower on each of the last two Fridays.

We also have to ask will we get incrementally more negative news in the economic data and in the conference season to propel even more bearish positioning? This may be more difficult. Right now, though, we zero positive catalysts and the geopolitics of Europe coming to a head, investors will be biased to stay short and underweight and look to be proven wrong. For me, this sets up as the type of market where I want to own options. They are not egregiously priced, and both the leverage if you get the direction correct, as well as the embedded stop loss if you don’t, can add a good deal to portfolio performance. Good luck in this shortened week and …

Stay Vigilant

Love the whole discourse as laid out by you above. Especially appreciate the CS ISM levels 1-pager. I am going to save that one for future reference.

RE: European energy crisis, there seems to be more upside risk at this point. Short term pain for European countries perhaps through end Winter. However if we get a spark of good news on the Ukraine war front, this could bring energy commodity prices crashing.

The article was going so well. I was thinking, boy I agree with much of this. Then all of a sudden it came, the reference to a "Lehman moment" and suddenly I needed to reach for Diazepram. My takeaway is the market is extremely dangerous--does their need to be a cathartic moment? Should one wait for the Sept seasonal to play out? Or given sentiment and positioning, there is a pop coming. In the end I am going for the later, but honestly it seems hard to argue with the HOPE theory of ISM 40 and a much larger bear market and in the back of mind I keep thinking about the difference between volatility and uncertainty and think the latter is probably psyhco, and am not ruling out an 85% decline in stocks as the cult of equity is first challenged, and then the whole passive bubble gets unwound. Is this most probable, definitely not, but you think about it when energy gets weaponized and we go in the Zoltan multi-polar world, extreme political polilarization, robots taking jobs, and climate change , blah, blah, blah....