Abbreviated look

With the data of late, time to revisit H.O.P.E.

I didn’t write last weekend for a couple of reasons. One, I was celebrating my daughter getting her PhD. Doesn’t happen every day, so I devoted some time to the family. However, another reason was that my opinion was not going to change until we saw the data this week. You know how important I think the ISM is, so I figured we might as well wait for it to come out.

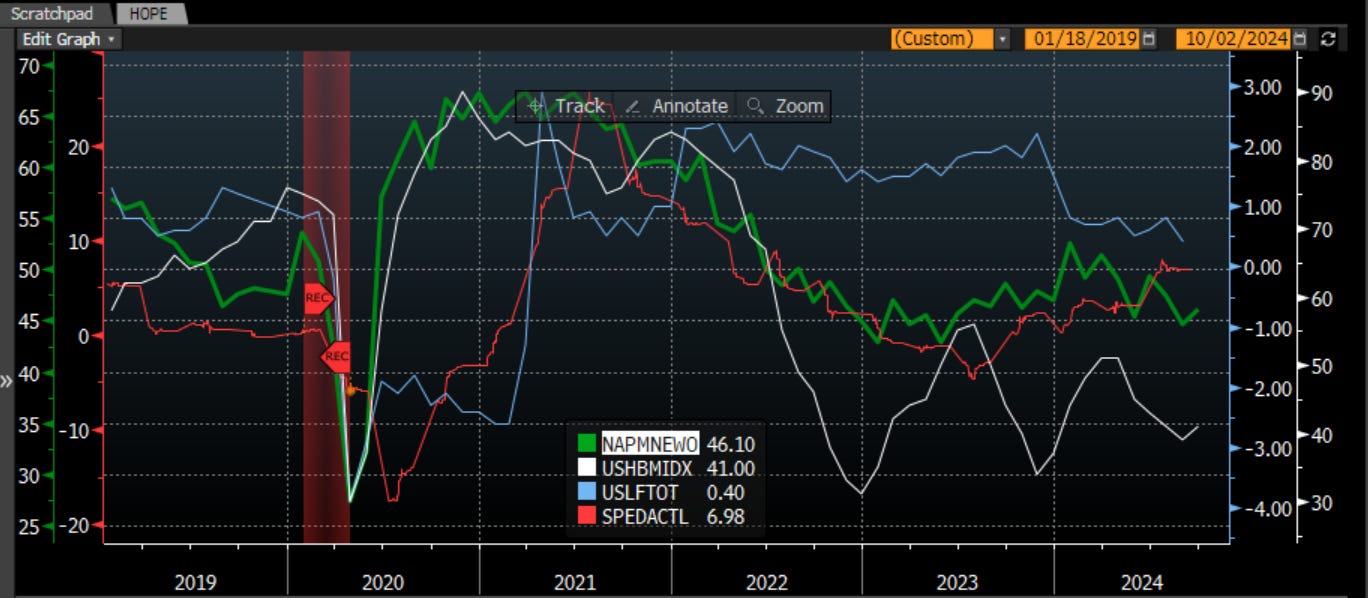

The headline index came in unchanged at 47.2 which was worse than expected. This is still above the 45 level that would call for a recession, but it isn’t what the market wanted. On the positive side, new orders to inventories did move higher, primarily driven by a fall in inventories but new orders we up as well.

Housing has been struggling to find traction this year. Yes, mortgage rates are coming lower. However, there are so many home owners still in a lower mortgage house. Thus, new orders have been heading lower which negatively impacting profitability and thus employment. H.O.P.E. is playing out exactly as you might expect.

One key difference may be that S&P profits have held up much better than you might expect. With ISM languishing at this level, the fact we have seen expected profits move a bit higher this year is surprising. Will this quarter be the great reset to reality or is the AI profitability that strong, at least for a few?

What about new orders outside of housing. The port strikes all down the east cost to the Gulf may well matter. Perhaps this will be explained away as an anomaly and give companies & politicians and excuse. However, the hit to GDP, the shortages of product & subsequent price increases, a bit of stagflation, is not welcome to consumers. Still early days but the Longshoremen seem to be digging in their heels. They are not the only ones as we have discussed before.

Speaking of housing, while mortgage rates are down nicely, I am skeptical about the impact it may have. For one, 85% -90% of homes are existing homes with a 4% mortgage. At 6.5% no one is selling. This means only new homes can fix inventory. However, Millennials are forming new households at a strong rate so demand is still there. This is putting a stress on affordability. Look at the chart above. Worst affordability this century. Giving money to first time buyers only makes this worse too. The biggest problem is that only 40% of the decline in affordability is from mortgages. The rest are real wages not keeping up with home prices. Supply/demand says prices aren’t going lower. Thus, the focus on wages. That is why the debate had such a focus.

Real wages impact consumer sentiment, measured here by the U of Michigan sentiment survey. Things have ticked up a little. Productivity gains help. However, as the labor market softens, and every sign is that it is, it will be harder for wages to keep up. Does this mean it will be hard for sentiment to rise?

Consumer sentiment matters. In fact in JP Morgan research, it is the ONLY thing that matters for the election. Right now it has picked up. Let’s see how it looks over the next month.

It seems to me that while there are some green shoots, there are still a number of risks to the market stool. The market stool has three legs - growth is fine supporting earnings, inflation moderates helping margins, and Fed cuts helping discount rates. Do you think there is anything that can cause that stool to wobble?

I do

Stay Vigilant

Congrats on your daughter PhD success! Very proud papa moment…enjoy it, Richard!