April showers bring ...

Looking through the potential catalysts in the market this month, and what we might expect them to bring

catalyst

1. : a substance that enables a chemical reaction to proceed at a usually faster rate or under different conditions (as at a lower temperature) than otherwise possible

2 : an agent that provokes or speeds significant change or action That waterway became the catalyst of the area's industrialization.

Often when we think of catalysts we hearken back to our high school days in the chemistry lab. Many of these readers probably sat in the back of the lab, pushing the risk envelope a little further than the teacher wanted you too, but you enjoyed it nonetheless. The catalyst we learned then was the metal or oxide used to speed up the chemical reaction. I mean the teacher couldn’t let the process take it’s natural time because she only had you for 40-50 minutes.

We have and look for catalysts in Finance as well. Finance is a science after all, even though many in the STEM crowd don’t want to admit it. The catalysts in Finance do very much the same thing - they speed up the time of the reaction or movement. Markets move at the margin - when there is a new or different buyer or seller.

Every day there are buyers and sellers that have different opinions of what can happen. We form our own view of what we think can happen in the markets by looking at the Fundamentals. This gives us the foundation for what we think will drive the economy which in turn will drive earnings leading finally to the movement in risky assets. We try to assess when too many people are leaning the same way. We do this in the Behavioral portion, trying to assess when many are thinking the same thing. If everyone has the same view, it is difficult to think you can make much money. Only when you have a variant view, and are correct, can you expected outsized returns relative to the market. However, it isn’t enough that you have a different view than others, what will get the others to change their minds? When others change their minds, this creates the margin flow, which changes prices and generates returns for those who are correct.

I would bucket the catalysts into short, medium and long term. For the short term, I look at economic surprises. Economic data comes out every day and while each piece varies in importance, each daily data point is a chance for someone to change their mind. Earnings information comes out once a quarter, this is the medium term catalyst. I look at how this data is being revised, and how it is coming in relative to expectations. This is another chance for people to change their minds. Finally, the long term catalysts are geopolitics. These take longer to happen, but when they do, they can shift the risk dynamics for months, years or even decades. Let’s look at each of these catalysts.

In the Fundamentals section, I walk you through some of the data that I look at to help me decipher the economic trend of various economies. I focus a lot on the US because that is where I am located. However, I do acknowledge that what is occurring globally mattes a good deal. Economic trends are slower moving typically. Trends don’t typically change quickly to get people to change their minds. However, data does come out frequently and whether it is better or worse than expectations can get people to change their minds. For this I look to the Citi economic surprise indices. You will often see these improving or decaying before we see the real shift in the trend data. I have put on here charts of the US, Europe, China and EM. This time series tends to be mean-reverting because as data disappoints, forecasts are lowered until it starts to beat and vice versa. A couple things stand out to me. First, while the US economy is expected to slow (I fall in that camp too), the data lately have been coming in better than expected on net. This is frustrating for bears. This may also be why stocks bounced higher, also frustrating bears. Second, EM data has been disappointing a fair amount lately. While this series is prone to more volatility, this is something worth watching, because EM is the manufacturing engine of the developed world so if that is slowing, DM may be set to follow.

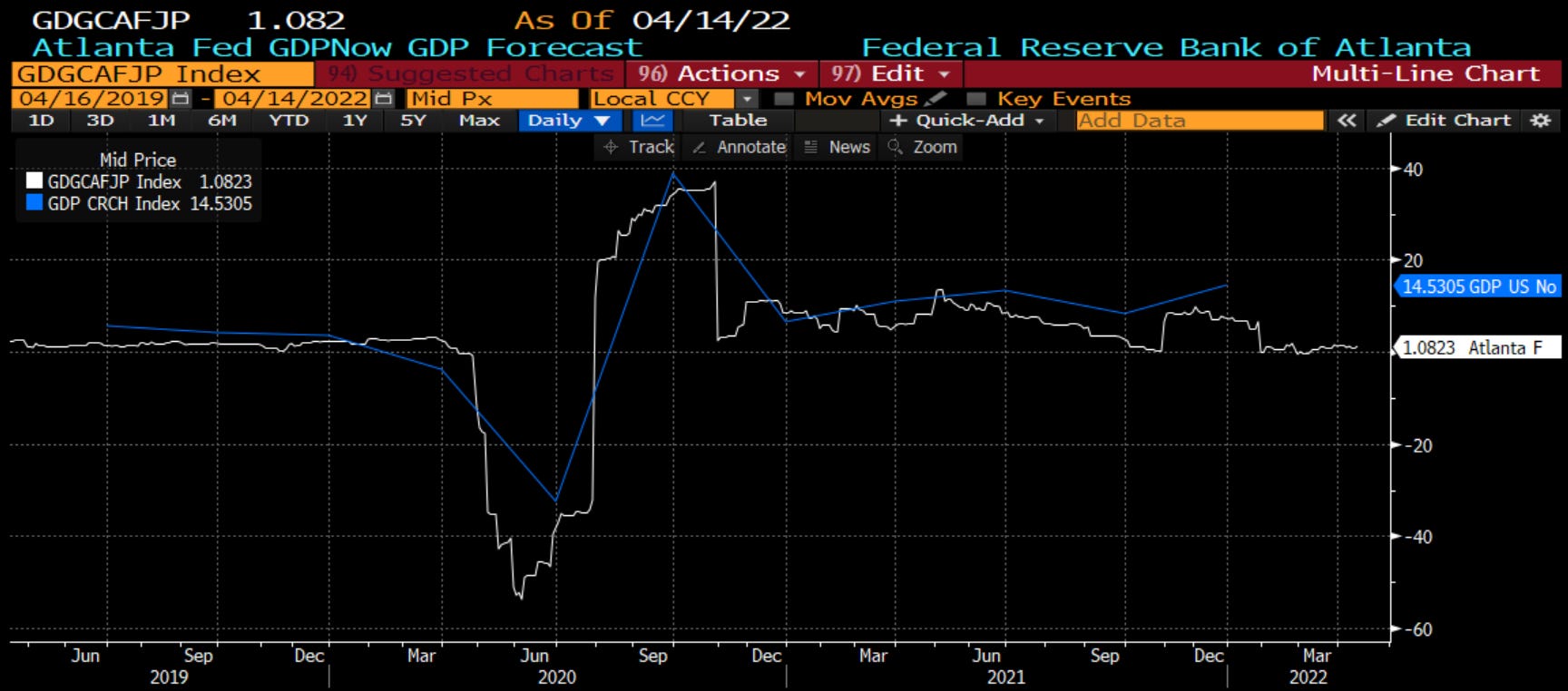

Another place we might see this show up is in the nowcasts. Nowcasting is the prediction of the present or very near future. It is the idea that we get more and more real time data and it is easier to predict what will happen next month than next year or 10 years from now. The Atlanta Federal Reserve puts one out that is followed the most. The shape (not the magnitude) has had some predictive ability of GDP. It is still saying we could slow down in the near future:

For the medium term I look to earnings. Earnings are just starting in the US as we got the big banks and investment banks this week. They will pick up in pace in the coming weeks but sometimes we can get an early look on what is happening, but importantly what is the reaction to the news. It has been my premise for the last 18 months that we are in a period in which we should not expect multiple expansion because of central bank tightening. This does NOT have to be bad for stocks, as long as stocks are growing earnings. If earnings suffer, look out below. So the earnings surprise data is picking up in importance. I have to preface this by saying that because of the games played on Wall Street with the analysts and investor relations, earnings almost always come in a little better than expected. So we want to look at how the ‘beats’ compare to history and how the market perceives the ‘beats’. You can see from the chart below, while the beats are positive, the trend in the magnitude of the beats continues to decline. However, perhaps because the market is a bit bearish, the reactions to the news are about what you would expect, with the bigger surprises seeing positive one day price moves. The one sector that stands out on this front is the financials. This sector put up some pretty big beats this quarter so far. However, the reaction has been muted. Why? I don’t know for sure. Perhaps it was because people read the Jamie Dimon earnings letter, which said things are good now but he is worried about the impact of high inflation on the economy going forward. Perhaps it is because the 2y 10y nominal curve had been flattening. I have been on record saying that this is the wrong yield curve to look at for banks. the 3 month/5 year matters for bank earnings. It has been steepening. Bank earnings were strong. However, I must respect the lack of reaction and understand investors are skeptical it can continue.

Another measure to look at is another Citi metric. It calculates the global number of positive vs. negative earnings revisions. I plotted this index in blue vs. the year on year change of the MSCI World Index. You can see that the change in earnings expectations is driving the change in stock prices. This revision data had been falling quite severely up until recently when it ticked higher. Stocks have yet to respond to it, again perhaps there is doubt about the persistence. However, it is something that bears watching.

The long term catalysts are geopolitics. Blackrock has a great repository on information on this at its investment institute website. Geopolitics are almost never positive. When these events are in the news, it is just the degree of bad. Often though, we can go long periods and not think of it. So in many ways, when geopolitics are neutral, this is a positive. Of course with a war in Europe, things are bad. However, it isn’t just the war in Europe that has this risk score moving higher (bad) and accelerating. It is the US-China risk concerns, cybersecurity risk concerns, and food security risk concerns. For me, if the falling of the Berlin Wall and the end of the Cold War were a positive, with a peace dividend in risk premia and the move toward globalization which helped eradicate poverty, increase standards of living, and improve company margins were all positive for the last 30 years, in my mind, this is all unwinding to some degree. This make take years or decades, but we are at peak risk-taking and time to understand that risk premia will continue to trend higher.

The last chart I will consider also comes from Blackrock. There may be risks in the world but the market doesn’t always care. There was Covid in the world but until it hit the financial centers in London and NY, the markets did not care. This matrix tries to show the risks the market cares about the most and we can decide ourselves if those are getting better or worse. The two cited on this with high likelihood are the Russia-NATO conflict and technology decoupling. Personally, I do not see those risks mitigating any time soon. Perhaps you feel differently.

Pulling this all together, the short and medium term catalysts right now are relatively benign. The economic data has been mixed globally, with a bit better US data offset by worse EM data. The nowcasts still think things could get worse in the near term, but we are not seeing this yet. Earnings data has been pretty good so far, and the reactions have been positive. It is still very early days and even where we have seen some very good earnings like financials, investors are questioning how long this can last. Finally, we cannot ignore the very high geopolitical risks that are negative and seem s to be getting worse and not better. In aggregate I would say the category is leaning neutral to slightly negative for now. However, a very solid earnings season could change that. We will know over the coming weeks and need to watch it closely.

Much like when we were mixing potions in our chemistry class, sometimes things were not happening, but we knew if we watched closely, something was soon to occur. That is very much where we are with the catalysts in the market.

Stay Vigilant