Back!

The market is climbing back just as the students are heading back

It is that time of the year again. The talk is turning to the return to school. Parents are telling me of their travels all over the country to take their kids to university. The caddies on the golf course tell me they are starting high school again the week after next. Soon enough, I will even be taking my youngest off to school, but as she is going into a 6-year graduate program, it is a bit more of a permanent ‘drop-off’. Wish me luck on that!

The market came back a bit this week too after the Monday bloodbath. I think we should probably have mixed feelings about this the same as we do about the kids going back. I wrote about that a little in the chat this week when I asked if it is ‘All clear?’

An update to the chart using Friday close shows the VIX and VVIX (implied volatility of VIX options) actually closed lower on the week. The VIX curve is almost back to flat. The risk episode is basically over, but the damage has been done. I think this is important to note because there were many that suggested this episode had a lot to do with investors changing their expectations of growth or the possibility of recession. I think it had very little to do with that. We can see that the exchange volume fell below the average for the year at the end of the week. People were squeezed out of positions and then stopped trading. This was a de-risking.

The spread between the Japanese government bonds and US Treasuries had been collapsing. The Japanese Yen ignored this as long as it could but after the BOJ raised rates more than expected, and the Fed gave hope rate cuts would start sooner, people realized it was not coming back. This caused levered investors to reduce risk in order to reduce their Yen loan books. A LOT of hedge funds borrow in Japan, convert the currency and invest abroad. My last hedge fund did this and we had few overseas investments in our fund. It was the cheapest leverage we could find and the prime brokers were glad to help facilitate.

This led some commentators to suggest that since the 10-year yield had round-tripped on the week (like VIX and VVIX), the bond market was clearly not worried about a recession. I would suggest it means that the bond market has not had a chance to price one in yet because it was too focused on the de-risking!

After the ISM services data and initial jobless claims this week, there were many that suggested that the recession fears were bunk anyway. Yield curve …yawn. ISM manufacturing … yada yada. Sahm Rule … not again. Housing … sure been weak but lower rates cures all. There will be no recession, it is a soft landing.

I have said all year that I thought there were three possible scenarios this year: 1. Fed cuts rates back toward neutral and we get a soft landing in the economy. 2. No landing in the economy and the Fed has to keep raising. 3. Fed cuts rates because there is a hard landing in the economy. The no landing scenario is looking less and less likely. Thus, we are back to whether the landing is hard or soft, and the difference between the two is whether there is a recession. Only NBER can tell us when we had one but the easiest definition for most comes down to whether there is job loss or not. As the saying goes, a recession is when your friend loses her job, a depression is when you lose your job.

First, on the bounce back in ISM services. It was better than expected as were the components. This is important given the large service portion of the economy. However, the three-month moving average of the data from PiperSandler shows the headline, the employment and the new orders are all at low levels relative to history. It is hard to signal an all-clear on these.

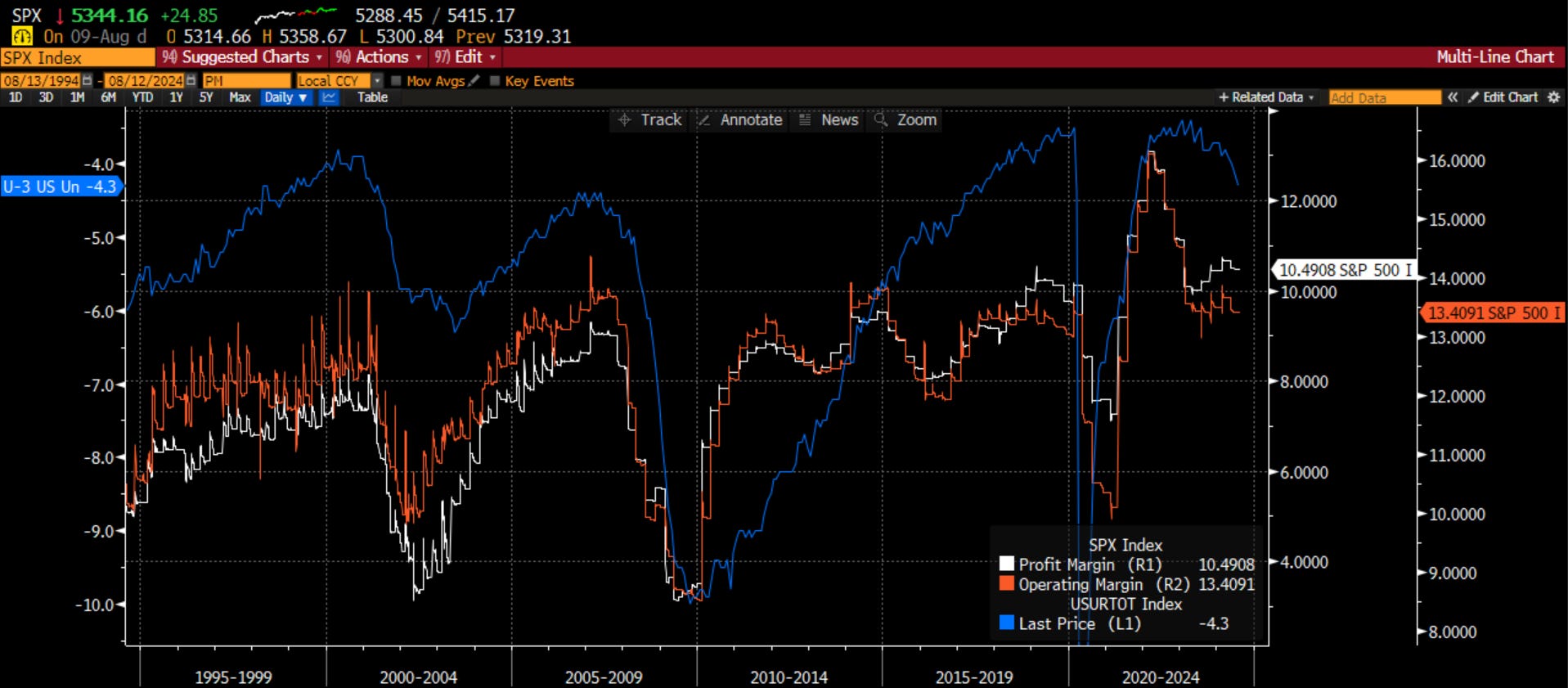

Next, I have talked about the jobs data, unemployment rate, and Sahm Rule. Here I look at the unemployment rate (inverted) vs. the SPX profit margin and operating margin. You can see that when companies make money, they hire more. When their profitability suffers, they lay people off. This is at the crux of H.O.P.E. Profits are struggling and thus employment is starting to struggle now. This will continue.

With earnings season coming to a close, the earnings surprises have been positive (almost always are) but are surprising at the lowest rate since Q4 2022. In addition, the stock reaction hasn’t been as positive reflecting some poor guidance from companies. Other than AI, investment banks and defense companies, pretty much everyone else is downbeat. 70% of the US economy is tied to the consumer, and companies are telling us the US consumer is tapped out.

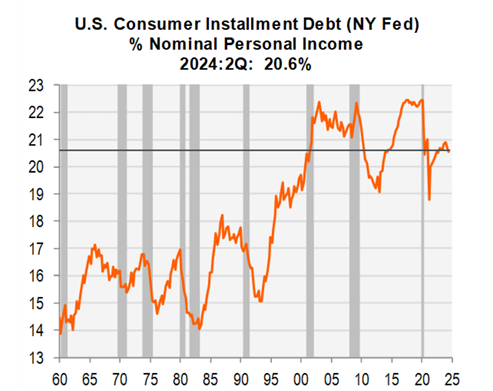

This chart and the next few come from Nancy Lazar who does the best work on parsing this data. US consumer installment debt is above 20% of personal income. Sure it has been as high as 22% a few times, but each of those has meant a recession. Also, when it has peaked before, it has meant a recession.

Interest payments as a percent of Personal income are 2.2%. Again, this level is suggesting a consumer that is tapped out.

Lower rates will help you say? Well, I don’t expect your credit card company to change their rates because the Fed moves. This is where people are struggling. Look at the 18-29 year old demographic. Over 10% are more than 90 days delinquent. Next worst are the 30-39 year olds. The youngest consumers, who tend to consumer at a higher pace, have no more room to do so. This is probably why we can see this type of price action:

Air BnB, Trip Advisor, Hyatt Hotels, Hilton Grand Vacations and Disney (theme parks as streaming was fine) all told investors that consumers are weak and expected to stay so. Look at the reaction in these stocks!

Staycation then? You know I love golf, but Achushnet (Titleist et al) and Callaway/Top Golf both told us the consumer is not spending on golf. A larger reaction in Callaway given the leverage present. So not just the young consumer but others too.

The counter-argument is that lower interest rates will spur housing which will start the H.O.P.E. in a positive cycle. However, that may be a bit too early to say. I showed this chart this week on LinkedIn - it is my own index of mortgage rates and unemployment rate (inverted) vs. two measures of housing activity - NAHB real estate index and MBA purchase index. Both measures are still falling and that it because even though the mortgage rate is going lower, the job market is getting worse as well (see above). If rates are 6% but you got fired, you still won’t buy a house.

Not to mention the fact that housing affordability, factoring in rates yes, but also prices, and incomes, is still at the worst level in the 30+ years of data I can find.

The consumers are also telling us they won’t buy. The University of Michigan Good Time to Buy a House metric just hit an ALL TIME LOW. This doesn’t sound like a H.O.P.E. cycle is about to start.

I could go on, but I know I have already gone too long. I have promised you to be better about that. However, I just wanted to show you the pieces of the mosaic as I am seeing them. Sure, the market bounced back, that is great. That can give us an opportunity to re-allocate our portfolio at better levels. However, don’t think that bounce back is because the market feels there is no recession coming. It hasn’t really begun to price in any sort of hard landing if it were to happen. A soft landing could still happen. That is a scenario. However, the jobs market is starting to suggest that this landing might be harder than many think.

For those that are sending kids or taking kids back to school in the coming weeks, I wish you safe travels. As teary as it can be, if they are going out on their own, it means you were successful as parents so be proud.

Stay Vigilant

Congrats on your youngest kicking off what sounds like a challenging graduate program. PhD? or MDPhd? Enjoy your time dropping her off. I know what it feels like. Cheers!

I think another aspect investors might be missing, is the composition of the mortgage stack. It cuts both ways. It was great everyone locked in low 30yr rates. It won’t be great when the fed cuts rates because the cuts won’t stimulate the economy as it did in previous cycles. To refi your 4% or 4.5% mortgage, the ten year treasury rate will have to be close to 3% and that implies the 2yr in the low 2% range. Cutting fed funds to fine tune the economy won’t have much impact. I believe roughly 50% of outstanding mortgages are 3.5% or lower. The ten year will have to be sub 3% to get those in the refi range.