Buried

The market, led by the banks, is finding itself under a mountain of bad news of late

Buried - this is the view from my 3rd floor hotel room in Lake Tahoe. They have gotten so much snow, with more coming this weekend, that it is piled up this high outside the hotel.

The market is feeling a bit that way, lots of news piling up. However, while it is difficult to sort through snow for the locals of Tahoe, it will be fun for them, with the ski lifts open until the middle of summer. It will not be that fun for market practitioners to sort through the mountain of news. When faced with such situations, market participants seek safety first and then sort through the events.

Silicon Valley Bank - you may not have heard of that bank before but you are certainly hearing about it now. The bank of choice for Silicon Valley start-ups is going under and the Feds are looking for a buyer this weekend.

What happened and why should you care? I sent out a Linked In about this on Friday:

Chart of the Day - action

“Now in matters of action the reason directs all things in view of the end” - Thomas Aquinas, "Summa Theologica"

I know what you are thinking, he is pushing the envelope if he thinks he can tie Thomas Aquinas to the fincl mkts. However, it is a Friday during Lent, so I have to try.

Today in the markets, we finally got some action. Believe it or not, participants were actually using some reason to deduce the end game.

“The science of mathematics treats its object as though it were something abstracted mentally, whereas it is not abstract in reality.”

The mathematics here are the mathematics of the banking system. Banks take in deposits & make loans, trying to capture a spread in this borrow short/lend long position.

It doesn't always work as planned. Ask George Bailey at the Bailey Building & Loan. As customers come & demand the deposits back, banks need to sell down some assets to cover this liability. That is why banks are meant to keep high quality liquid assets.

Except not all banks do that. This week we saw two banks fail to take in enough selling assets to cover the liabilities & therefore steps had to be taken.

The top chart shows you the 3 mo vs. 5 yr part of the yield curve in blue. It has inverted like the rest of the curve. It is a proxy for bank net interest margin in purple - it leads this.

The stocks know this and that is why the XLF's relative performance to SPY follows the yield curve. As the curve flattens, fincl stocks start to lag the mkt.

"Nothing can be known, save what is true” - Silicon Valley Bank loans to the VC crowd - founders & companies. As you can imagine, there isn't the same robust secondary mkt for shares in start-ups as in the public mkts.

It therefore had to sell stock in itself, at more than a 50% discount (because investors were marking down the assets on the balance sheet) to get the necessary capital. Not good.

Silvergate Capital chose to have its assets in a different illiquid medium - crypto. It was great the last few years when crypto went higher. When crypto crashed, and customers wanted the deposits, there was nothing to do but turn to the FDIC.

Why was this bad for the mkt overall? Because banks are the veritable canary in the coal mine. The banks will feel the effect of higher rates. Banks are the transmission mechanism of tighter Fed policy.

In the bottom chart, you can see that in this hiking cycle, smaller regional banks lead the SPY. Those banks, led by the two above, were crushed today. What does that mean for the overall mkt? Especially if the Fed is still hawkish due to inflation?

Success & money are fleeting. In fact, Aquinas also says you won't find happiness in money, honor, fame, power, or pleasure. If this is your goal in the fincls mkts, you will be disappointed. I will vouch for that.

Use reason, take action if necessary and most of all, Stay Vigilant.

#markets #investing #stocks #yieldcurve #banks

In fact, SVB was the largest component of the KRE regional bank index. Thus, it along had a disproportionate impact however, now the worries of contagion and the Great Financial Crisis will kick in. As I said to a friend on Friday, I think this is more like the Continental Bank collapse of 1984 than the Great Financial Crisis of 2008 because SVB is not a systemic institution like Leham was, with its tentacles touching major banks across the world. However, SVB will leave a pretty big impact, particularly in the VC and VC-backed company community.

You see, SVB had only 2.7% of its deposits under $250k. That is the magic number where the FDIC insures the deposit and customers can get their money back. Genevieve Roch-Dechter had shared this chart in a post on SVB. You can see in the lower right, SVB was one of the lowest percentages of deposits under this threshold.

This means a large portion of SVB’s customers are NOT protected by the Fed’s insurance. Why would someone do that? Because these were primarily business accounts. As I heard from a friend describing the situation:

“The problem at Silicon Valley Bank is compounded by its relatively concentrated customer base. In its niche, its customers all know each other. And Silicon Valley Bank doesn’t have that many of them. As at the end of 2022, it had (https://cdr.ffiec.gov/public/ManageFacsimiles.aspx) 37,466 deposit customers, each holding in excess of $250,000 per account. Great for referrals when business is booming, such concentration can magnify a feedback loop when conditions reverse.

The $250,000 threshold is in fact highly relevant. It represents the limit for deposit insurance. In aggregate those customers with balances greater than this account for (https://cdr.ffiec.gov/public/ManageFacsimiles.aspx) $157 billion of Silicon Valley Bank’s deposit base, holding an average of $4.2 million on account each. The bank does have another 106,420 customers whose accounts are fully insured but they only control $4.8 billion of deposits. Compared with more consumer-oriented banks, Silicon Valley’s deposit base skews very heavily towards uninsured deposits. Out of its total $173 billion deposits at end 2022, $152 billion are uninsured.”

You see, it had a lot of customers that were not insured and therefore got very nervous very quickly. Not only did these customers rush to pull out their money, but they told their friends to do so as well. This money is the lifeblood of many start-up companies in Silicon Valley, so you can imagine the deleterious effects this is having on the VC world, which now must come up with more money to fund its companies.

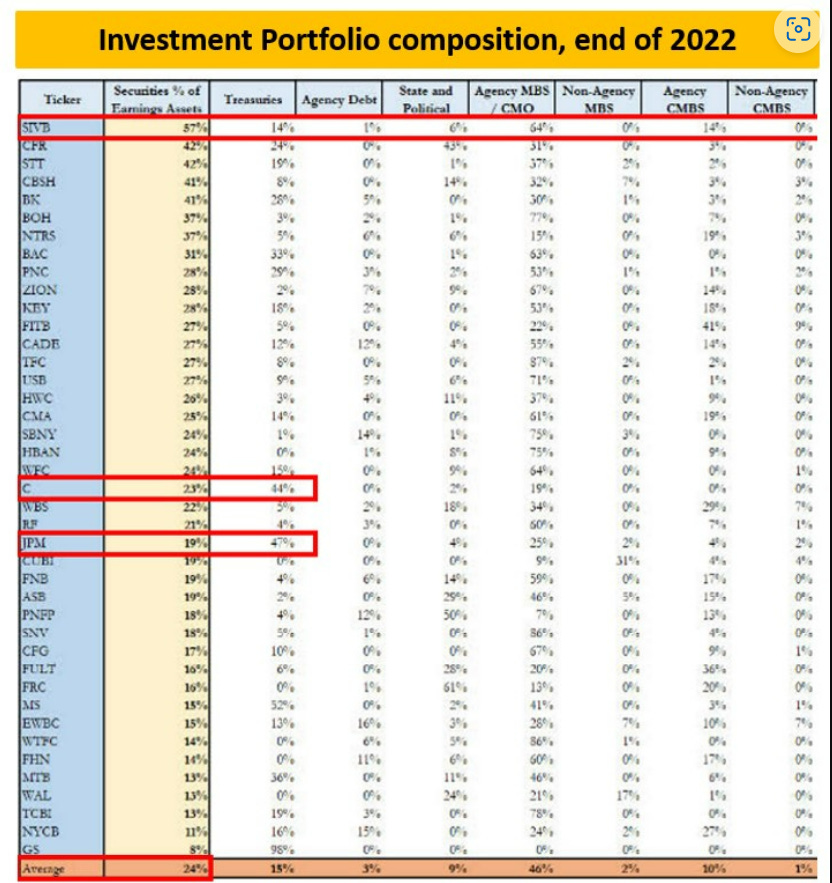

So there is a run on the bank. Deposits are the liabilities of the bank. It has assets to cover this right? Yes, since the GFC, banks have been urged very strongly to keep assets in HQLA or high quality liquid assets. These include Treasuries and mortgage-backed securities. SVB did this.

Per Alfonso Peciortello:

“SVB had a gigantic investment portfolio as a % of total assets at 57% (average US bank: 24%) and 78% was in Mortgage-Backed Securities (Citi or JPM: around 30%)…

Source: MacroAlf

In my Investment Management Academy class, we analyze bank stocks. About a week before this all went down, I had sent an email to the teams looking at banks this semester and told them:

“Some considerations as you are surely bearing down on this now.

We potentially could be headed to a recession. This means bank balance sheets will become a bigger focus.

This issue probably mattered a lot more pre-GFC when some banks funded in the market while others funded through deposits.

However, the ability to fund, even if it means attracting deposits, is a critical issue when the availability of capital is decreasing and the cost of capital is increasing.

Another issue you must all consider is credit costs and bad loans. Banks have been reserving for loan losses, is it enough? What does the loan portfolio look like? Is one bank safer than others because the areas in which it makes loans has historically held up better?

Recurring revenues via areas like wealth management. Investors like to pay more for this as long as the company can execute.

Geographic footprints – all else equal, a bank will be able to grow more profitably if it is located in a region where there is a lot of growth vs on that is not. Think of a Florida bank vs. an Illinois bank.

Sensitivity to rate moves. At this point we may be getting close to the end of the cycle. Maybe not based on Jay Powell’s comments today, however, you should all consider the same rate scenarios – rates up or down, yield curve steepening or going more negative – that DJ will lay out for you. The banks themselves report this sensitivity as the Fed requires it. Let’s consider the same scenarios for this for each bank.

Bank net interest margins are tied pretty closely to the 3 month vs 5 year part of the yield curve. Have a look at the banks you analyze to see how well it fits that.

The Fed does a number of studies (can get via FRED database) on Senior Loan Officer Surveys. You can get a sense for how optimistic or pessimistic banks are toward certain kinds of loans. You should consider this in your analysis.

Finally, from a valuation standpoint, I think the single best way to think about this is Price to Book vs. ROE.

Plot all banks in the Russell 2000 on these two metrics. Draw a 45 degree line. Is the bank you are analyze above or below this line?

If it looks cheap, is this because the ROE is low? Does it really stand out? Is something changing in its performance?

If it is above the line and looks expensive, is this because it has delivered above sector performance on ROE? Could something hurt this?”

One thing we had seen over the last 18 months was that banks knew there was going to be a rate hike. How do we know they knew? They have to report to the Fed their interest rate exposure. Every bank we looked at was positioned for higher rates. How do they position? They hedge.

You see, they all have to own Treasuries and MBS as assets in addition to their loan portfolio. However, as banks all knew rates were going higher, they knew there would be losses on these fixed rate assets. So they entered into fixed to floating swaps. They sold their fixed rate exposure and received floating rate exposure. They would not have the same losses if rates went up.

Except SVB didn’t hedge. Let me say that again. SVB did not hedge against losses from rates moving higher. Every single bank in the world knew rates were going higher and hedged with swaps (and the swaps dealers hedged themselves with options). Yet SVB didn’t hedge. You can see this in the company’s own report to investors.

Source: MacroAlf

Duration measures the amount of gain (rates lower) or loss (rates higher) on a bond portfolio. For its bond portfolio and 5.6 year duration, this meant that the bank would lose about $7 billion if rates went up 100 bps and $14 billion for 200 bps. Rates have gone up about 250 bps. This wiped out the entire owner’s equity of the bank. Remember Assets = Liabilities + Owners Equity.

For a bank this means Loans + HQLA = Deposits + Bank capital. As the assets went down, the bank didn’t have capital to cover the deposits. It tried to sell assets, it couldn’t. It tried to raise capital in the market, and even at a 60% discount, investors would not buy stock because they got a look at the balance sheet. It was a disaster.

Now the Feds will try to find a buyer over the weekend to cover these losses. We will know Monday if successful. You see, the Fed’s do this so there isn’t contagion and a run on other banks too. Nick Timiraos of the WSJ had a tweet about Jay Powell’s possible reaction function:

The bottom line is Jay Powell does not like bailouts, but he is also worried about contagion. We have already seen something similar go down in the world of crypto with Silvergate as I mentioned in the tweet. Could this happen at other banks too? Can banks sell down assets fast enough to cover deposits They will be selling Treasuries and MBS meaning they will be doing the same thing the Fed is doing with QT. The cost of capital is going. The liquidity in markets will dry up.

I mentioned Continental Bank before. The Atlanta Fed wrote about this: https://www.atlantafed.org/cenfis/publications/notesfromthevault/1604

“The 1980s and Continental Illinois

The FDIC's History of the 80s: Volume 1 analyzes some of the major issues the agency faced in the 1980s, including Continental Illinois.3 That analysis observes that Continental Illinois had long been a conservative bank, but that changed when its management decided to adopt a rapid growth strategy in the mid-1970s. In implementing this strategy, Continental's opportunities for in-market growth were sharply constrained by state laws, which, at the time, prohibited interstate banking and limited in-state branching to one drive-up facility, according to Federal Reserve economist Tara Rice and Erin Davis, a Morningstar equity analyst. Thus, it is not surprising that in order to implement this growth strategy, Continental increased its domestic commercial and industrial lending by 180 percent between 1976 and 1981, largely through aggressively competing in the national commercial lending market in terms of loan rates and quality. In order to fund this rapid growth in lending, Continental Illinois increasingly resorted to buying federal funds and issuing certificates of deposit.

The risks in Continental's rapid growth strategy first became apparent in late 1981 with notable deterioration in its corporate loan portfolio. Continental Illinois was also exposed to risky debt from less developed countries (mostly Latin American countries), which started showing weakness in 1982. As other banks were being downgraded, Continental managed to retain its AAA rating from Fitch in March 1982. However, market perceptions of Continental's condition deteriorated abruptly in July 1982 with the failure of Penn Square, a relatively small bank in Oklahoma. The late 1970s saw a sharp upward spike in oil prices, which led to rapid growth in opportunities to lend in the oil-producing states, including Oklahoma. Penn Square had aggressively exploited these opportunities even when doing so meant ignoring the basics of credit risk management.4 The volume of loans generated by Penn Square far exceeded its capacity to fund them, so the bank sold loan participations to other banks, and Continental Illinois was one of the largest buyers.

The failure of Penn Square led market participants to reevaluate the value of those loan participations and the health of banks with significant exposures to them. As a result, Continental found its access to domestic funding markets sharply impaired, forcing the bank increasingly to rely on paying higher rates in foreign money markets. Continental's condition continued to deteriorate through 1983 and into 1984, though it continued to pay some dividends even after Penn Square's failure, and its president and chairman remained in office through almost all of 1983.

Continental became the subject of various rumors in May 1984 and shortly thereafter overseas depositors started to run. In response, the Office of the Comptroller (OCC) took what the FDIC historical review calls the "extraordinary step" of declaring that the agency was unaware of any significant changes in the bank's operations, as reflected in its published financial statements, which would serve as the basis for rumors about financial distress at Continental. The run continued, however, so 16 major banks put together a $4.5 billion line of credit to help fund Continental Illinois. However, this action did not stop the run, so on May 17 the FDIC injected $1.5 billion in capital, the Federal Reserve committed to meet Continental Illinois's extraordinary liquidity needs, and the FDIC guaranteed all of Continental's depositors and general creditors.

These actions allowed Continental to continue operations until a permanent package was put in place in July 1984, which included the purchase of $4.5 billion of loans and the injection of $1 billion in capital by the FDIC. The chapter on Continental in an FDIC (1998) publication Managing the Crisis: The FDIC and RTC Experience, 1980–1994 reports the ultimate cost of the transaction was $1.1 billion, which was, as a percent of assets, a "modest" 3.3 percent (albeit, somewhat higher on a present value basis).5”

We should be looking for the Fed to find a buyer. If not, it will look to inject liquidity and facilitate an orderly disposition of the assets. It will do all it can to prevent contagion.

I don’t think this will be systemic like Lehman Brothers. However, I think this is going to leave a very real mark on the banks and on the markets. Now we have to see if it will adjust the pace of Fed policy.

Stay Vigilant

What a great case study for your class and timely too. Reminds me of when my microbiologist wife was teaching her grad and undergrad students online during the pandemic and they were analyzing the COVID bug. One of her most attended and highly rated classes even now.

As always great in-depth analysis of the story around SVB!