Credit tightening revisited

Looking back at the "Plot Twist" post from March and some recent LinkedIn posts

We are three months on from the banking crisis that occurred in March. I thought it would be worthwhile to look back at what I thought would happen, what has happened, and what might still happen.

This week, Chairman Powell had his semi-annual testimony to Congress. In his prepared remarks and comments after, he came across as quite hawkish. More on that later. However, he was also grilled on the bank failures that have happened this year. Senator Elizabeth Warren, who has been a constant critic of JayPo’s and who has often been rumored as a potential replacement, did not hold back on her views of his handling of the banking crisis we saw in March. Per CNN:

The Vice Chair for Supervision is Michael Barr, who started in that role in the summer of 2022. As a former Assistant Secretary of the Treasury under President Obama, he had an active role in the creation of the Dodd-Frank Wall Street reform as well as the Consumer Protection Act. Thus, would seem to be well positioned to know what to look for. JayPo might have been skirting the question, but is the bank crisis as big as Senator Warren is making out?

According to the FDIC website, we have had three failed banks in 2023 and we know them well - Silicon Valley Bank, Signature Bank and First Republic. How does this compare to history?

Of the 565 bank failures from 2000 to 2023, 465—or 82%—occurred from 2008 to 2012. Bank failures hit a peak in 2010 at 157 in one year—more than double the number of bank failures we've seen in the last 10 years combined.

However, the three banks this year had total assets of over $600 billion. Again, according to the FDIC website, from 2001-2020 there were 561 bank failures and the total assets of these banks was $721 billion. So, the assets of the three failed banks this year are approximately the same size as all failures this century and larger than the total assets of banks that failed even during the Great Financial Crisis. In fact, over 98% of the banks that have failed since 2007 have had assets under $10 billion. We should not be surprised that the bank failures this year are a big deal.

Has this had much of an impact on the industry and the availability of credit? This has been the subject of many of my posts this week. But first, let’s revisit some of the things I wrote in “Plot Twist” three months ago.

In the March FOMC press conference, JayPo had thoughts on what these bank failures might mean:

I said at this time: “This is exactly the topic I was speaking to many friends in the market about on Thursday and Friday. The FOMC is passing the torch to the banks to do the heavy lifting on slowing the economy and bringing down inflation.”

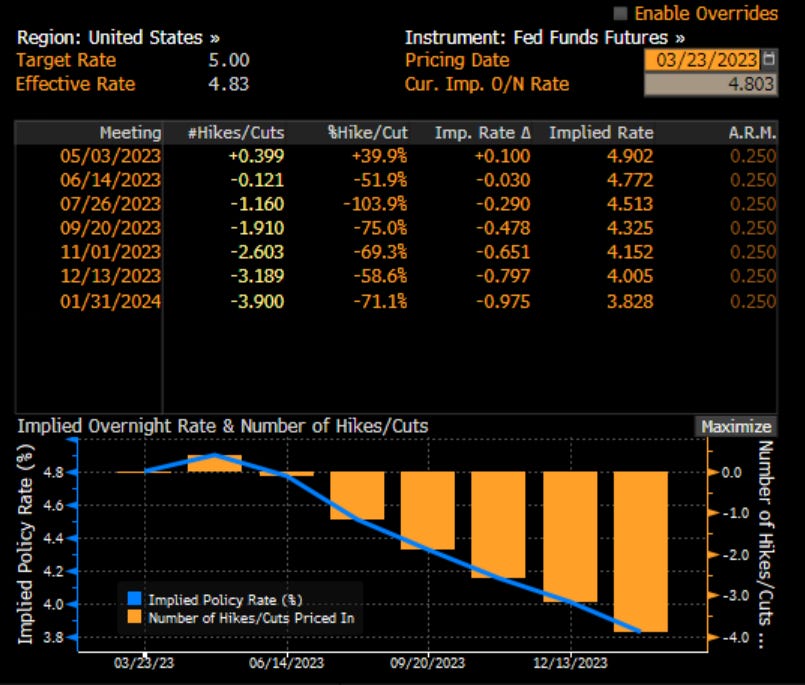

Has this happened? Not exactly as planned. If we look at what I refer to as the terminal Fed Funds, which is just the Fed Funds future 6 months forward, we can see that in March, at the time of these failures, the market really moved down the expectation for Fed action, pricing in cuts. Since then, that has largely been removed. The FOMC has actually raised rates 25 bps since then and took a pause this month. However, the 6-month forward futures have gone up more than 60 bps.

JayPo signaled at the FOMC meeting and again this week to Congress that the Fed may have more to do in order to get the inflation back to 2% target. Again, according to CNN:

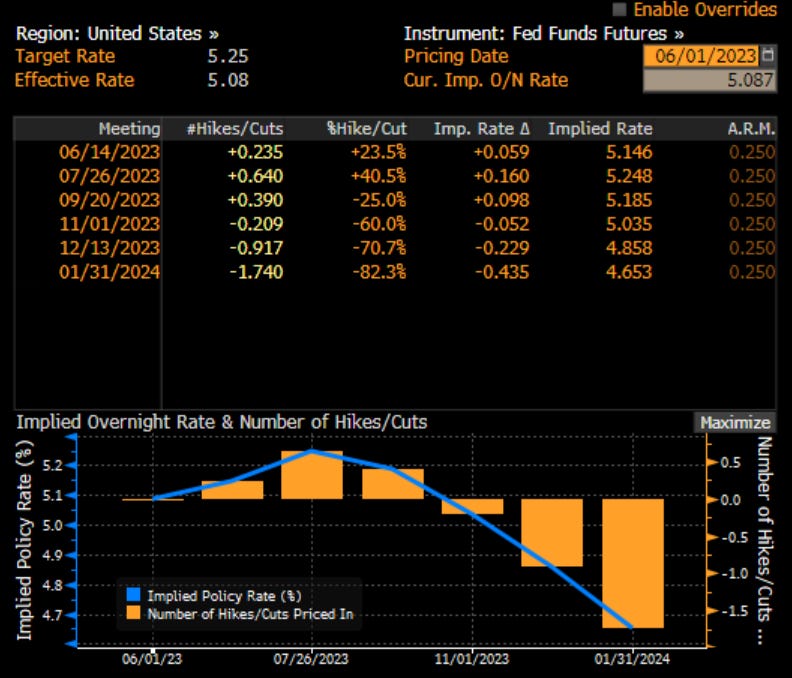

We see another hike priced in and actually don’t see cuts to the Fed Funds until 2024 now:

This is very different than March, which saw low odds of another hike and had cuts starting in June:

It is even very different than the start of June, which still saw cuts starting before the end of the year:

You will recall from the podcasts with both Fred Goodwin and Barry Knapp that Peak Fed is a major driver of market performance. All of this year, the market has seen Peak Fed. Thus, the multiple of the market (here I look at the inverse, the forward earnings yield) has disconnected from the terminal Fed Funds. Should it? Will we start to see this forward earnings yield move higher, meaning a lower forward P/E for stocks?

This is even more interesting if we go back to the “Plot Twist” post. Why? Because the FOMC is still being hawkish even when it’s own research suggests we are going to have a recession. Why do I say this? From March:

"Frankly, there's good research by staff in the Federal Reserve system, that really says to look at the short - the first 18 months - of the yield curve. That's really what has 100% explanatory power of the yield curve. It makes sense. Because if it's inverted, that means that the Fed's going to cut, which means the economy is weak." - Fed Chair Powell, March 21, 2022

Looking at that indicator, which I call the JPOW Recession Indicator, you can see that it has down a pretty good job that last 40 years in predicting a recession. When the forward TBills are more than 50 basis points below the current 3-month TBill, a recession occurs. The loan ‘exception’, which was really a double dip, happened in 1997. This was a period when we had the Asian Financial Crisis beginning and the market anticipated the FOMC cutting rates. It did, because of uncertain effects from abroad, which served to boost the US economy and market again, leading to more severe hiking cycle that ultimately brought the economy and market lower in 2000.”

In the last three months, this indicator has gotten even worse and is flashing a recession signal:

However, the market is ignoring this. I say that because the only reason to buy stocks, if the rates are still going higher, is if you believe earnings growth will be even faster. Even faster earnings growth in the face of a recession? Seems hard to fathom. I wrote about this on LinkedIn on Friday after a reader asked me to take a look at something:

“Chart of the Day - yields

The chart today is a request from a reader (hat tip PS) who saw a similar chart in the FT & wanted it lengthened out beyond 10 yrs & wondered what gives

The chart today compares the corp bond rate which we discussed yesterday, with the earnings yld & the short-term government bond yld. The FT had the 3-month yield but data on that only goes back 20 yrs. I was able to lengthen to 30 yrs for all of them if I used 6m which is essentially the same.

Theory would suggest that the corp bond yld should be above the short-term risk-free rate, & the equity yld should be higher than all of them. The logic for this is that the more risk an investor takes, the more they should be compensated for that risk. Equities are the riskiest asset & govt bonds the least risky, in theory

However, as we see often through time, the theory & the reality don't always mesh. The argument for preferring equity to short-term rates is the potential reward. Investors trade off risk & reward. With a corp bond, the reward is the yield, same as a govt bond. There is no bigger reward than that

Why is the spread between corp & short-term govt the narrowest in 30yrs? The corp bond yield is a 10 yr yield. The spread to a 10 yr Treasury is still 195 bps which is close to the lowest of 30 years but not quite there. The 3m vs. 10yr yield curve is inverted to the tune of 157 bps which is the most inverted (by 80 bps) it has been in 30 years

Let's now look at equities vs. corp bonds. In the 90s, there was a preference for stocks to bonds for two reasons I can think of: 1. we were coming out of the late 80s junk bond crash led by a Savings & Loan crisis so investors were scared of bonds 2. We had the internet revolution so investors saw big rewards

The big rewards in stocks are high potential earnings growth. The earnings yield is just a multiple expressing investor sentiment. One can still make money at a low yield if earnings are really growing. These earnings did not materialize in the 90s so the investor sentiment converged to corp yields

After the Great Fincl Crisis, when everything crashed and bankruptcies occurred, investors began to prefer bonds again. In bankruptcy, you have a chance to get something as a bond holder. You get zeroed as a stock holder. No one saw the higher rewards, just the higher risk

For the last 13 years, bonds have been the preferred beta of investors. That is now changing with the AI fad. In fact, investor sentiment is so robust, investors are now looking for a lower yield in stocks than bonds. This must be due to a high expected growth in earnings as that is the only rationale

Will we see that? Its unclear but as we saw in the 90s, it may takes yrs for investors to realize this. There is no margin of safety in the riskiest asset but it all hinges on earnings growth from here. Any signs of economic slowdown that hurt earnings will affect equities the most”

We might think that the economy looks just fine. In fact, the restaurants, airports and hotels still seem busy, right? There is a dark cloud behind all of this. Credit conditions are actually getting worse and not better. It is not just the cost of money but the availability of money that drives the economy. I wrote about that this week as well:

“Chart of the Day - credit conditions

I have focused a good deal on the NDX and how disconnected from other parts of the equity market, and even other risky assets, it has been. However, there is another risky asset that has been rather robust of late too

That other asset is the credit market. If we measure the strength of the market by the spread of corp credit to US Treasuries, the spread of less than 200 bps is not the tightest it has ever been but is 1 std deviation below the 60 year mean, so there is some exuberance

Of course credit spreads are a relative measure since we are looking at the difference between the rate a corporation must pay for a loan and the rate the government must pay. Another way to think of this is the absolute level of the interest rate

On this basis, the Baa corp loan rate at 5.42% is the highest it has been in over a decade, last seeing these levels in 2011. Bear in mind, though, that preGFC and ZIRP, rates were consistently much higher in absolute terms. Thus, even this level by historical standards looks below average

There may be other ways for us to judge the health of the mkt though. It is not just the cost of capital, but also the availability of capital we should beware of. On this basis, things might not be as rosy as they appear at first blush

I have a few measures on this chart today to try and demonstrate. The white line is the level of the Baa corp bond rate that I discussed. The green line is the inverse of the percent of banks tightening loan standards. The orange line is the NFIB small biz credit conditions index. The blue line is the yoy change in commercial loans at banks

As you can see, all have moved sharply in the wrong direction in the last 1-2 years. Some of these, like the % of banks tightening and the small biz credit conditions, are in recession territory already. The banks change in loans is really close to that

I know, I know. Here is another chart that Rich is showing that says we are in a recession when the stock mkt says we are not and every restaurant says the same. However, without access to funds, how do businesses continue to grow and continue to hire people?

We saw the other day that central bank liquidity is moving in the wrong direction. JayPo told us yesterday QT will amount to $1trill a year. Today we see that banks, which have fewer deposits to back loans, are in fact making it much harder to get a loan

Sure, we can go to the private mkts for capital. Can every small biz access that mkt? I know the private credit mkt has been hot, but it is still funding a small percentage of the needs of the economy

I know there are many credit mgrs and bankers in my network. Would love to hear what you think about the cost and availability to credit right now”

In fact, a few people in a position to know did comment on this. Per Brook Scardina:

“Good piece and analysis. As a private credit lender, we’ve seen a significant retrenchment of capital from traditional lending sources (i.e., banks, credit unions, etc). The systemic risk introduced by the regional banks has accelerated the tightening of financial lending conditions. Bloomberg shared a statistic that less than 20% of private lending is funded by US banks. Credit markets tend to lead equity markets, so certainly something to keep in mind. As we are all aware, markets may not repeat, but they often do rhyme.”

Another reader, Ben McMillan who you saw interview me, shared the post with his network and commented: “Had this exact discussion with Alberto Pagan-Matos, CFA of Glide Capital (who are experts in the private credit space). Tread carefully and be selective!”

I spoke about this back in March and this is what the Fed worried about:

“The Fed knows banks are going to tighten standards. We discussed this last week. I think this is important enough that I want to highlight it again. In our fractionalized banking system, a bank’s loans + investments = deposits + bank capital. Typically for every $1 of deposit taken in, about $10 of loans are made. Right now, banks are struggling to retain deposits. That is the big problem right now. It is particularly acute for small banks. About half a trillion has already left big banks.”

This is why the one source of strength in lending right now is the private credit market where institutional money is pulled into the asset class in search of higher yields. However, even the experts in this space are getting extremely cautious. We still don’t see this showing up in the markets, but these are some extremely yellow flags that we should all beware of. It recalls a post from two weeks ago that I wrote on Linked In:

“Chart of the Day - pushback

I took a chance yesterday & offered a trading/risk management thought. Doing that, you always know there are going to be some that pushback because it is counter to their views. Others pushback because they dislike the entire notion of trade ideas

All good. I love pushback. I am from the school of Socratic debate. If you pushback against my ideas & I don't have a good answer, then I need to do some work on said idea as it is not ready yet

But if you pushback against my ideas, & I feel I can & do respond well, then I will become even more convinced that I have the right idea. It is an art & process that has become lost in the current polarized & angry online shouting which rarely resembles debate

There were two types of pushback that I got yesterday, mostly in DMs. The first is that we are in a period similar to the late 90s & not the early 00s because AI is revolutionary & driving stocks

The other was that this period is akin to when we came out of the GFC, with housing leading the charge. Given the low supply of existing homes on the mkt, home builders are making hay right now with good sales at good margins

These were both periods of easy money or at least easy availability to capital. In order to assess I chose to look at many measures of the availability of capital. This is a busy chart but I will walk you through it

The white line is Fed Funds, the starting point in the cost of capital discussion. Building from that we get the blue line, the 10 yr Treasury, which will reflect the path of future Fed funds over the longer term

I add to that two spread measures. In light blue is the mortgage spread. Mortgages are priced as a spread to Treasuries. When money is available, this spread is low and vice versa. The other spread is the Baa corp credit spread in orange. Again, credit trades as a spread to Treasuries

The last line in yellow is the Fed Senior Loan Officer Survey on whether banks are tightening standards, making it hard to get loans, or loosening standards & making it easier

You can see that in our current period: 1. Fed funds are at the highest in the cycle & highest since preGFC 2. 10 yr is also near the highs in over a decade 3. Mortgage spread is the highest in the last 30 years 4. Credit spreads are low 5. The tightening standards are at peak levels usually seen before a recession

Now look at all of these in the late 90s. Yes the Fed had hiked & 10yr was higher, but the spreads & survey were all very low. The cost of money was high but there was plenty of availability. I would argue that is different to what we see today

Look at the period right after the GFC. All of those metrics were falling quite precipitously to what would be the lows of the 21st century. Money was flooding in as we were being urged to take more risk

The only measure that is the same is Baa credit spreads. Not sure this tells me 2023 is the same as 2010 or 1999.”

Updating that chart, it is still flashing warning signs:

This is also going to hurt employment and we are seeing those signs. Back in March I wrote: “For loans to small businesses, it is even harder to get a loan than for large businesses. This hurts the outlook and optimism for small businesses. I have inverted the small business optimism index, or NFIB Outlook here, and compared to the percent of banks tightening standards. You can see there is a really good fit to this data with the immediate post GFC period the only period when loans were available but businesses weren’t optimistic. However, as standards will get tighter, we should expect optimism to fall. If businesses are not optimistic, do you think they will hire more people? There has been a disconnect between the outlook and employment this year. I expect these two series will recouple with employment falling. We already see that in the tech sector.”

Updating those charts:

We have seen this in the jobless claims data as well. Jobless claims is one of my favorite measures because it is timely, it is not subject to revisions or hedonic adjustments, and it does a really good job of leading earnings and asset allocation. I wrote about this about 10 days ago:

“Chart of the Day - transcendentals

Yesterday I was fortunate to play golf with my family at an awesome golf course. As you know, I play a fair amount of golf. My family, though, doesn't play much any more. Golf is a game that can be extremely enjoyable or extremely frustrating. It tends to be frustrating when you don't play much

If the timing is off by even a little bit, the shots become very wayward, very quickly. This can lead to ever more angst. In some ways it is like investing. When things are going well, it is very enjoyable. When things are off even by a little bit, it can be frustrating

I suggested to my family that we think about the Transcendentals. Plato, Aristotle & Augustine taught us about the Transcendentals hundreds of years ago. They are the Beautiful, the Good & the True

As it pertains to golf, the Beautiful was that we were in a special location, with people we love, having a very fun time. This is a Beautiful thing & to be enjoyed. The more we focused on this aspect, the more we had a very fun time

The Good would be that the more we enjoy the Beautiful the more we want to get better & play more. The True would be that the more we play, the more we would understand what is making the shots go awry & we could figure out a solution. That wasn't for yesterday. Yesterday was beautiful

From an investing standpoint, many in the mkt are also focused on the Beautiful. The price action in the stock market is Beautiful. It is in a relentless march higher with very few & short-lived down moves. Money is clearly being put to work & those that are long are having a very fun time

The Good would be that if you were long stocks & enjoying it, you might ask how you can do it more. You might want to focus on the economy, on Fed policy, on earnings or on multiples. The True would be trying to figure out how each of these things may affect the stock market & what they are doing now

Lost in the good vibes of this week is that the jobless claims have ticked above 250k for the second straight week. I show that (inverted) in white here. The job market weakens when profits are starting to weaken. We see the profits in orange have been weakening for 9 months & are expected to continue

The blue line is historically linked with profits & jobs. It is the ratio of the total return in stocks to the total return in bonds. When times are good stocks outperform. When times are tough, the opposite happens

Except that is not the case right now. Stocks are meaningfully outperforming bonds even as the drivers of relative performance move the other way

How far will it go? No idea. We took the Beautiful focus from the 18th hole to a terrific restaurant for dinner. Mkt bulls want to do the same thing. They are taking prices to new levels. At some point, it starts to get late and it has to end. Until then, it is time to relax and enjoy”

Jobless claims have been rising for a month. This is the chart updated:

The biggest standout is still the stock market in absolute terms and relative to the bond market, in spite of the move this past week. However, that may be changing. I wrote about that earlier this week:

“Chart of the Day - really quick

Back from my terrific vacation and already caught back up in the busy-ness of life. So I only have time for a quick post.

I have seen the moderate weakness in equities the last couple of days. Many are probably asking - is this the correction we have waited for or is this just another headfake?

I ask myself the same question. In order to answer it, I quickly went to two charts to try and understand the move - one fundamental and one technical

The blue line below is the SPX Index. The purple line that overlays it is the SPX forward P/E. The forward multiple has been the primary driver of the market for almost two years. Earnings have not been a major driver but instead investor perceptions have been

You can see this multiple rolling over. Why is that? Are people just getting nervous? The reason the multiple is falling is because the FOMC continues to tell us there are more rate hikes on the way. JayPo sent us the same message again, saying there is at least one more rate hike on the way. Fed Funds Futures are responding in kind

Forward P/E and Fed Funds track very closely (on an inverse basis) during rate cycles, either positive or negative. With the terminal Fed Funds moving higher, the forward P/E must come lower and it is. This suggests more downside

The white line on this chart is a technical measure. It looks at the Put-Call ratio which measures investors/traders desire to either hedge downside risk or tactically bet on upside in stocks. I use the 10 day moving avg to smooth it out. I present the inverse here

As I wrote in my weekly, the market would move higher until this measure rolled over. This week this measure has rolled over. As you can see, when it turns, it usually moves in the new direction for a bit

Thus the technical picture has gotten cloudier for stocks too. I could also point out how the relative strength index had hit an extreme late last week and has rolled over. In addition, the moving average convergence/divergence is also crossing lower. These are all short-term technical indicators that suggest more downside

I give you this info just so you have it at your disposal. This isn't a trade recommendation at all. I am not in that business. I just want to say that the fundamental picture, which has been negative, continues in that vein. The technical picture, which has been positive, is getting a little worse”

Remember, the forward P/E is the inverse of the forward earnings yield which I showed above. It has become disconnected from the terminal Fed Funds and looks to want to move much higher in line with terminal Fed Funds, meaning a lower forward P/E. We will see what earnings bring in July when companies begin to report again. Right now, the expectations may be too high relative to what we are seeing in the economy. The economy leads earnings but earnings are only off about 3-4% from their peak in 2022 even though the ISM has collapsed from well over 60 to below the 50 level:

I know I have been downbeat on risk for some time. I have gotten a great deal of pushback on that. I deserve it. I can assure you, I constantly question myself and the things I look at. You see that play out in real-time via my posts on LinkedIn, Twitter and Substack. Working through the thoughts today, though, it is still difficult for me to be upbeat. To wit:

The Fed is still hawkish on inflation and suggests there is more work to do in order to get to the 2% target

The market is pricing in a higher terminal Fed Funds and rate cuts have been pushed out into 2024

The multiple of the market will be negatively impacted by the higher for longer risk-free rate

Earnings will have to drive the market but earnings are ultimately driven by the economy which is looking weaker while earnings expectations have not reset fully yet

The Fed’s own recession indicator is strongly indicating there will be a recession

Credit conditions are getting worse so it is not just the cost of money but the availability of money that is a problem

This is negatively impacting small business optimism and small business hiring

We are seeing this show up in jobless claims which are a good leading indicator of the relative performance of stocks to bonds

The technical picture of the market, which has offset this negative fundamental picture all year long, is deteriorating and the best indication of this is the Put-Call ratio rolling over

In sum, betting on risky assets now, you are betting that the multiple will move higher and defy the higher Fed Funds, the earnings will improve and defy the negative economic signals, and the negative economic signals will improve and defy the negative availability of money via lenders. That is not a bet I am willing to make, especially when I can get a similar or higher yield in 6-month Treasury bills than I get on corporate bonds or stocks.

Stay Vigilant

Risk free rate became somewhat of a misnomer in a time where everyone expects fed to quickly rescue markets if they stop going up. The only risk left is being left behind with debased dollars.