Defense against the Dark Arts

As Mad-Eye would say: “When it comes to the dark arts, I believe in a practical approach.”

I had to bring out the picture of Mad-Eye Moody this week, as we all need some refresher work in the Defense Against the Dark Arts. It is getting pretty ugly out there, people. This was highlighted by long-time reader Phil D. who sent me this factoid:

Thanks for the reminder, Phil. The fact I read this literally right after I read the story of UBS buying Credit Suisse, in a merger engineered by the Swiss Government makes it that much more special.

I worked for UBS, or its predecessors, for 20 years. I started with Swiss Bank Corp which had to buy UBS in 1998 after the Long-term Capital Management debacle. UBS had been bigger but then imploded and the stronger SBC, with a more conservative and risk-management culture, had to bring aboard the cowboys at UBS. Ironically, 25 years later it is UBS that is bringing aboard CS, which seemed to always feel like it was more sophisticated than UBS, at least to its employees. Stay humble everyone.

This all comes on the back of the SVB, Signature NY and Silvergate debacles I discussed last week. As an aside, I can give you an idea how panics start. George Stephanopoulos used the Signature Bank Illinois logo in the story about Signature Bank NY. There is ZERO affiliation between the two. If anything, the corporate cultures couldn’t be more different, as Signature Illinois is quite conservative. However, this story was out:

Source: Medium.com

This meant the management at Signature Illinois had to spend all week calming down customers that saw the news story and wanted to get out. That is how bank runs start. We all need to be more careful about what we share and write about but coming from a professional journalist at a major network, that is pretty appalling.

This is why the Fed had to step in with a $2 trillion life-line and allow banks to bring collateral and get 100 cents on the dollar even if the assets are as low as 60 cents. Banks have responded by going to the discount window at a record pace, faster than even during the 2008 financial crisis:

Before I speak about what the impact might be from this, let me go off on a brief tangent. This week, in speaking about the SVB crisis with many people, I came across a couple bits of information that I want to give my two cents on.

First, I was a guest with another professor on the No BS Newshour hosted by Charlie LeDuff (thank you for the invite, and hope your team keeps reading, Charlie). The other professor is a Socialist and has written books about it. We had a good discussion from two different views which is hard to do these days. However, I was struck by something Prof. Wolff said. He said his work has never been more popular in his 50 years of teaching. In his mind this is because of the failures of capitalism. I didn’t bring it up on air, as it wasn’t the right time or place, but I would like to point out that every government that has tried Socialism has failed with the exception of two: China and Cuba. Some might say some country in Scandanavia, but those governments and systems failed in the 90s and in fact places like Sweden are now more capitalist than the US.

On the Cuba front, I would like to draw a comparison between Cuba and Singapore, two island countries founded in the 1960s by powerful leaders who led for decades. Singapore has a ‘managed democracy’ but has fully embraced capitalism. Having lived there most of the 90s, I watched with amazement as it was the only country in Asia to not have riots during the Asian Financial Crisis. Why? Because the country has raised the standard of living of all of its people. In fact, if we compare the per capita GDP of Singapore and Cuba, I ask you which one might you say is the more successful?

Ahh, but what about China you may say. Well, first of all, I would argue that China did not see economic success until this century, after it joined the WTO and embraced a more capitalist view even within a Communist ideology. Second, I would compare China per capita GDP to that of Hong Kong or Taiwan, that have/had democracies and capitalism all along. Again, just comparing the per capita GDP in USD across the three, which is more successful?

So every country that has tried Socialism has failed except two, and those two have massively lagged other similar demographics. Can we agree that capitalism, in spite of its many flaws, and I admit to those, is better than socialism? I agree there are income inequalities that should be addressed, but switching to a system we know will fail or at least lag badly, is not the right choice.

In fact, I have written about this before when I mentioned the ‘third way’ that was discussed back in the 1920s when we were having this same capitalism vs. socialism debate. Distributism, triumphed by GK Chesterton, acknowledges the failings of both and suggests that a better way is a more decentralized approach that doesn’t put too much power in the hands of one government or one company. There must be more predominance of small ownership. Think artisanal farms and shops. I have even thought about decentralized finance in this regard.

That brings me to another point. I follow closely the writings of high school classmate Michael Creadon. He is a terrific writer and entrepreneur and discusses the digital asset space very well. It helps me stay up on the events in the space. This week, though, Creads suggested we have a problem with our fractionalized banking system, it has too many flaws. The criticism was aimed at the fractional banking system generally and not just the bad banks. The solution was DeFi. While I agree DeFi and other parts of the digital asset space are potentially very impressive and disruptive technology, they are not a solution to fractional banking. You see, ANY bank that has a run will go bust very quickly. This is true for decentralized banks as well as our current banking system.

The way to avoid a run is to be very conservatively managed so customers are never nervous. It is to know your customers well and have them know you well. Even good ole’ George Bailey of the Bailey Building and Loan had a run on the bank. What did he tell his customers:

Run on the Bailey Building & Loan

George calmed this down because he told the customers their deposits were in so-and-sos house etc. He knew his customers. They trusted him. He was able to give them some, but not all, of their money and they got by together. He survived. They survived. If a banker doesn’t have this trust, the bank won’t.

What else do we know from that movie? We know that the growth of Beford Falls in the movie would NOT have happened if George didn’t take on this leverage and make these loans. Remember when George sees life without him? Many small businesses didn’t start or didn’t last. Housing developments didn’t occur. The economy was not as robust.

You see, the same thing happens in fractional banking. Without the leverage of taking in deposits and making loans, there is far less growth in the economy. If we want to do away with banking, are we content with far slower growth? I don’t think people are. It could happen. Senator Warren and others are calling for investigations and regulations which will surely come. However, ask the venture capitalists and tech entrepreneurs how vital SVB was to the ecosystem? Read this article about Chicago, which isn’t even the epicenter, to see the impact:

The same was true for Signature NY, that lent money to people to buy taxi medallions or people to start crypto businesses. I am not saying these are smart loans, I am saying that there are niche businesses of all types, from start-ups to taxi medallions, that don’t happen without banks like this. The economy is far less dynamic.

Yes, these banks made mistakes; however, let’s stop short of damning the entire banking system or capitalism as a result.

Back to your regularly scheduled programming.

About that dynamism … it’s about to be a lot less. Much like those who said what needed to happen to get to carbon neutrality and Paris Agreement goals got their wish and we saw a dress rehearsal during Covid, many others saw this lockdown and got really nervous about their future. The rest of this year for sure, we are probably about to get a dress rehearsal for what an economy without much bank lending will look like.

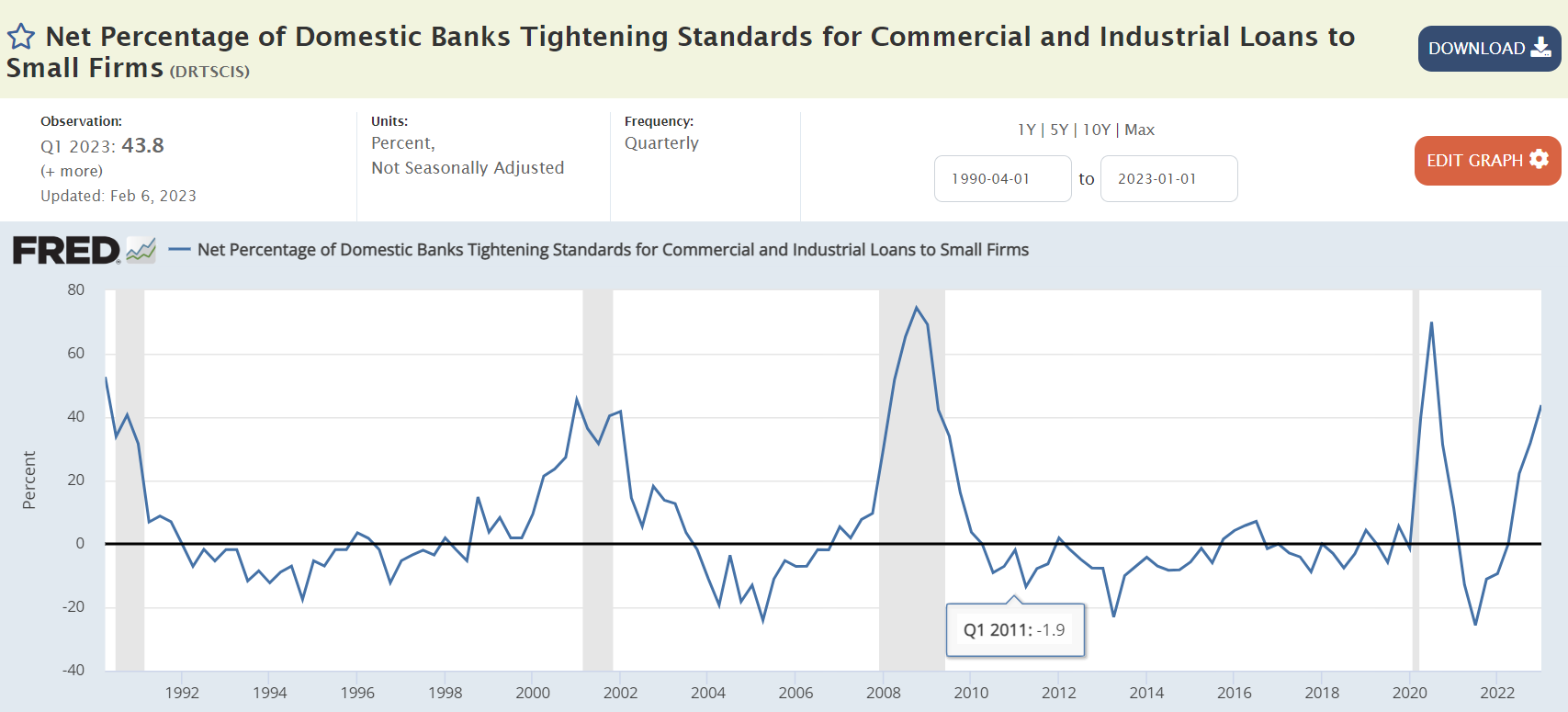

I say that because bankers were already getting more nervous about lending to businesses before their own businesses came under siege. We can only guess that banks’ willingness to make loans will plummet, which has traditionally led to a recession. You can see that as of a month ago, more than 40% of banks were already tightening standards. When this hits 60%, we have a recession. I am not sure if it will have gotten there yet, but I am comfortable saying it is a lot closer now:

We are already seeing this in the mortgage market. The spread between 30 year mortgages and 10-year Treasuries just hit the widest level for which I have data, wider than even during the national housing crisis of 2006-2009. Yes, this had been exacerbated by quantitative tightening, but now this is about banks not lending:

Remember that graph of 30-year mortgages and the NAHB Realtor Index that were popular on Twitter last year? Those will be coming back soon. This does not look good for the housing market:

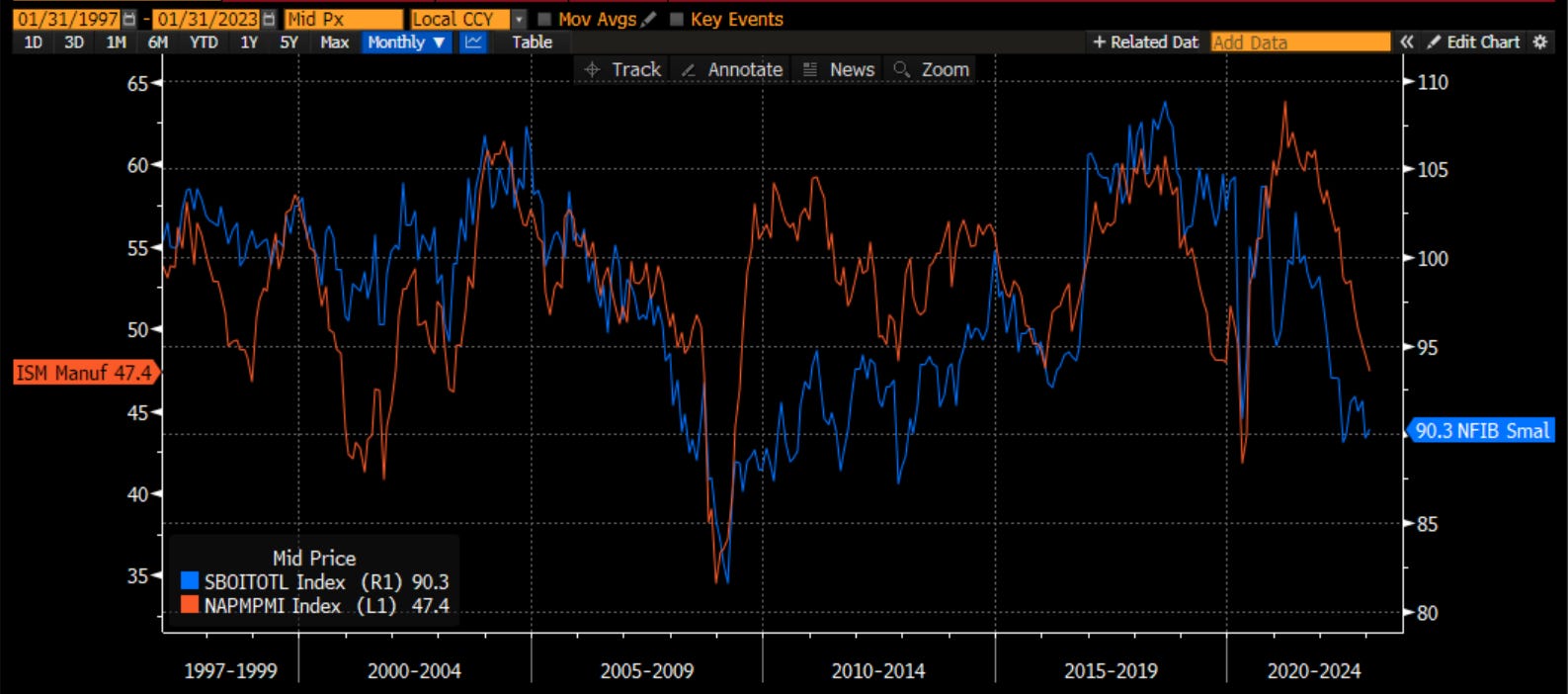

Also, as banks tighten credit, small business optimism falls:

As small businesses are the engine for the economy, if they slow, the ISM falls as well.

The ISM and the yearly changes in the SPX are tied at the hip:

What about the rally we have seen this week? Personally, I think that has more to do with macro funds blowing up and covering positions than I do with real money putting it to work. Why would these funds blow up? Look at the move in the 2-year notes:

Over 100 bps in 7 trading days. I have to credit Jim Bianco for bringing this volatility and the blow-ups to my attention. He put this on LinkedIn:

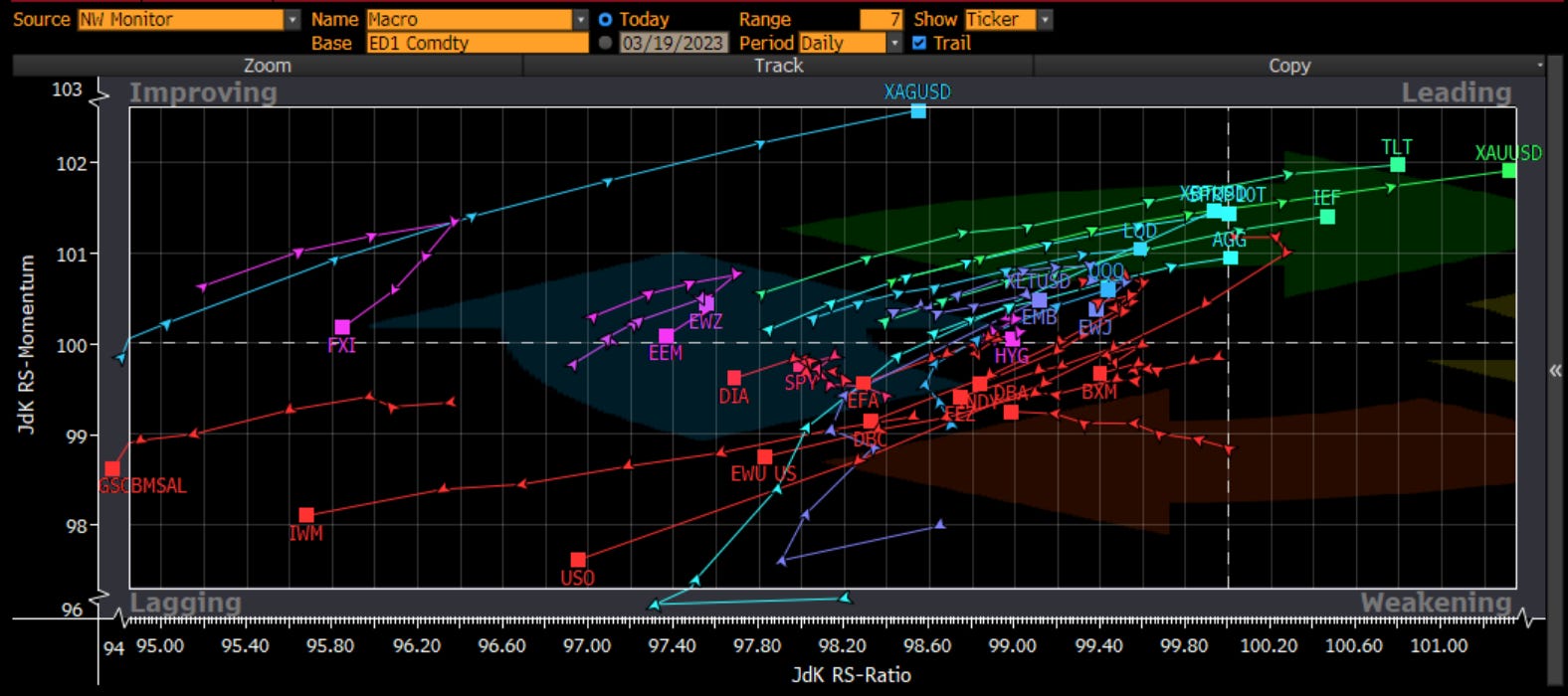

We have definitely seen a flight to safety in the last 7 days, as we can see bonds, and high quality bonds at that, leading the way and riskier assets clearly lagging:

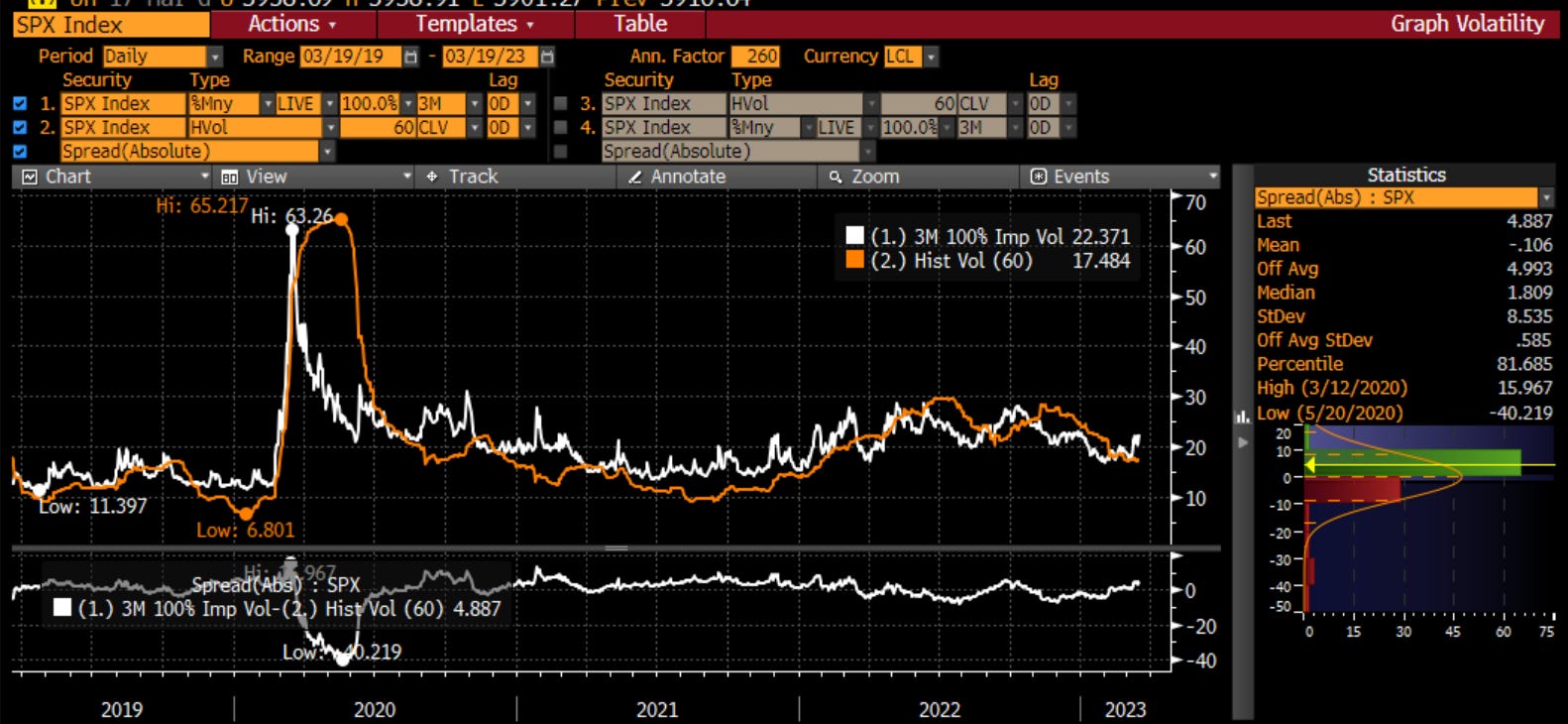

What to do from here? This bond market volatility we have seeing is leading to an increasing in the global financial stress index. The VIX is historically correlated to these and has yet to see a spike of the same magnitude:

In fact, SPX implied volatility (expected future) is les than 1 s.d. above the trailing historical volatility. The spread on the far right looks quite reasonable:

I have referred to the Chris Cole analogy between forest fires and volatility before but here it is again. We do not know exactly when a forest fire will start but we do know when the conditions are such that one has a higher likelihood of starting - drought, poor forest management, seasonality etc. The same is true with volatility. We don’t know when a major vol shock will happen, but we do know when the conditions are such that it will - less available capital, less certainty from companies, poor market microstructure. The conditions for a forest fire are present.

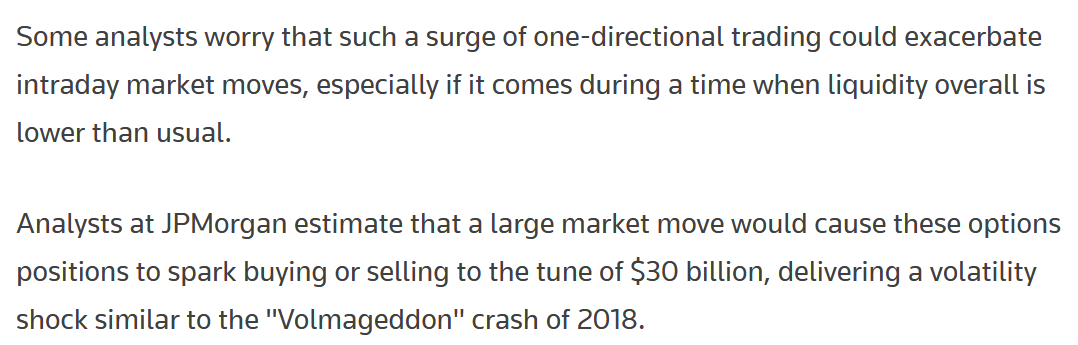

One last note on market microstructure. I haven’t chimed in on the 0 days to expiry (0 DTE) options craze. All I will say is that the short gamma these options cause is weakening the market microstructure. This means volatility of the market is dampened until it no longer is. You can read more about this craze from Reuters here

The article references work by JP Morgan which I always thought did a great job on the liquidity in the market. In the piece they say:

Thus, I would encourage people to consider adding convexity to your portfolios. I am not a financial advisor, nor do I play one on TV. You should do your own work. However, I am looking to get longer gamma now because of the tremendous uncertainty. I use puts instead of shorts and calls instead of longs. I am more inclined to buy straddles now than I ever would be. One trait of options is that they are insurance. You want to buy the insurance before you need it. You want hurricane insurance before a big disaster hits etc. Whether you are bullish or bearish, I would suggest you consider expressing views with options.

For me, I will be looking at a lot more puts than calls. I still do not believe this is a systemic crisis along the lines of Lehman and the GFC. However, I think there are enough problems and yellow (if not red) flags that I see, that sitting in cash (short-term Treasuries or FDIC insured accounts) and spending some premium still seems like a really good idea to me.

Stay Vigilant

One thing I forgot to add was this tweet from Eric Rosengren, formerly of Boston Fed:

https://twitter.com/EricSRosengren/status/1636749555395067904?t=UqyTMb-8O4Mk8ZspWYBxsQ&s=09

Punchline: Too soon to think the problem may be over

a few things on capitalism: I recently read a comparison on how capitalism works like a system similar to biological life form where it naturally evolves/develops to survive by reallocating capital to sustain relevance and profitability. The beauty of capitalism is, although it is more zero-sum then most other systems, variance and choice is celebrated. In other words, many people can be the beneficiaries of single use cases (i.e. pepsi and coke). The biggest enemy to a systems sustainability is centralization and monopoly, as the bottlenecks to financial well-being dramatically tightens under these circumstances. With socialism you start at the end, with centralization and monopoly. This is why I tend to align with views that fight monopoly and central authority and celebrate capitalism, competition, and choice. Preserving an equilibrium of corporate power will naturally cater to consumers best interests from a bottom to top flow of demand. In other words, people actually have great political power in their collective economic demand. Top to bottom flow of demand (like in socialism) holds no such power and leads to bottlenecks in development and growth that will decay competition and choice and ultimately power on a global stage. People forget we don’t live in a bubble and geopolitics can also get pretty “Game of Thrones” sometimes making GDP important element of security and freedom. So long winded for I hope people choice not to fight capitalism and instead chose to preserve the elements that democratize and empower