“History Doesn't Repeat Itself, but It Often Rhymes” – Mark Twain.

Exploring how past market crises can help us navigate the current one

It has been quite the week. Last Friday we were still trying to determine what the ECB failures meant for risk when the market was hit with a CPI number that was much higher than expected. In rapid fashion, the bond market went from pricing in 50 bps in June and July FOMC to 75 bps at each. It was so rapid and so apparent the FOMC needed to send out a trial balloon, which it did via WSJ and CNBC, signalling to the market that it was on board. Jay Powell then said as much in the presser after the meeting in which the Fed raised 75 bps, the largest such move since 1994.

It didn’t have to be this way. I have been saying for over 18 months that inflation was not going to be transitory. I have been saying all year that I didn’t think growth would slow enough, or fast enough, to reign in inflation. However, the Fed still blindly followed the path and now finds itself, and all of us, in some pretty hot water. I recall hearing Charlie Evans in early 2021 at U of I saying the Fed should be willing to let inflation run hot, because ‘we know how to handle that.’ Unless you lose control that is.

It was obvious to many that the Fed should have begun hiking, and hiking aggressively, in September 2021. Many would say ‘but QE after the GFC didn’t lead to inflation, why should this?’ I will give you to answers and a follow-up. The first answer is that this Covid QE is different than the GFC QE. See, the Fed doesn’t create M2 money supply, banks do by extending credit. After the GFC, banks took the balance sheet the Fed was growing and absorbed it as bank reserves that allowed them to de-lever and repair their balance sheets. This was necessary and actually allowed the US economy to pull out of the malaise much faster than Europe which did not provide the means for banks to repair. However, at the time, you may recall Obama complaining the banks were not getting the money into the real economy. In 2020, not only did banks get the money to the real economy via PPP type loans etc. but the Fed itself skipped Wall Street and went directly to main street. Thus we saw the fastest M2 money supply growth in the history of the US.

The second reason this is different is because this money growth was augmented by massive fiscal stimulus. Again, if we look to the post GFC period, politicians and bureaucrats were actively trying to slow spending as central banks were easing in 2008. In the US we had the Tea Party trying to reign in spending. In Europe, we had austerity for the peripheral countries. In both cases, the fiscal restraint offset the monetary growth. This time, we saw very fast growth on both fronts for the first time since WWII.

Whether they want to admit it or not, this was an exercise in Modern Monetary Theory (MMT). Advocates of this theory suggest the government can and should print money and spend it until the market gives a signal it is too much. That signal? Inflation. Well folks, the market is giving that signal.

I have also been saying for the last decade that many in DC understand inflation is the goal. You see, we have a debt problem in the West. Too much of it. Post GFC we managed to get most of it off of consumer and corporate balance sheets and onto the government balance sheets. Corporates have reloaded some. Consumers not so much. Either way, when there is too much debt there are three ways out of it: default which governments outside of Argentina are loathe to do; restructure which US politicians are loathe to do because this would be reforming the entitlement system; or inflate the debt burden away. Yes, some would say we could grow our way out of the debt problem which is exactly what the US did post WWII. The US also had a very high debt to GDP ratio then. Over the next decade, the debt did not grow much but since it was spent on industrial abilities (initially for the War), human capital (GI Bill) and infrastructure (highway system), it had been allocated in a way that allowed for rapid US growth and therefore the debt to GDP came down as GDP grew faster than the rate on the debt. That is not going to happen this time because the West faces demographic issues which put a lid on growth, and the debt was not optimally allocated in the fist place.

That leads us to today. We now have inflation. The Fed took too long to act and now must ratchet up the pace. This means things will break. It will break first in the areas where capital was most misallocated, but ultimately it will break most things. This is why history will not repeat but it rhymes. Many have asked me if this is like 2000 or 2008. There are similarities and differences. I posted this in Linked In today:

The chart today looks at 1997-2002 in blue, 2005-2010 in white & 2018 - now in orange. We can see overlays are rarely perfect & only modestly helpful. Be careful when people use them to give specific mkt levels. However, they can be useful to help us understand what the unwind of excesses can look like. To be most instructive we really need to look at the mkts where the excesses most took place - tech in 2000, housing/fincls in 2008, fintech/crypto now. However, even as the excesses unwind in certain corners of the mkt, the broader mkt & the broader economy will feel that burden. How much of the consumer & housing strength this cycle or the inability for companies to find labor was due to the gains being made in people's crypto & Robinhood accounts? We may never know but there is some positive correlation.

The commonality to it all is that the unwind takes time. This cannot and will not be the V-shaped experience of Covid. That was an exogenous shock to the global economy with a record response by authorities. This is quite different. Unwinds take time. The hit to investors psyches takes time to improve. The willingness to extend credit after a deleveraging event is measured in years and not weeks. But as the Greek poet Menander said "Time is the healer of all necessary evils." Time heals all wounds.

Here I want to dig in a bit as to the places where the bubbles have happened. In this graph I have the Nikkei from the mid 80s to mid 90s, not the first bubble but maybe the biggest of the post War era where we had a lot of data. It is the bubble against which we typically compare the others. It is in white. Overlaid is the Nasdaq bubble from 1995-2005 in blue, the oil bubble from 2003-2013 in orange and the DeFi bubble from 2018 until present. You can see that the more gradual the unwind, the longer it takes. Oil was the fastest crash but it came back sooner. The Nikkei didn’t get back to the 1990 high until 2021. That is some long and painful adjustment. Right now, the DeFi bubble as measured by XET appears to be following more of the oil crash. In some ways this could be good news.

The latest bubble is not just in crypto. I had done a Macro Matters podcast for the CFA Society Chicago (https://www.cfachicago.org/podcast/macro-matters-series-yield-curve-inversion-is-duration-durable-or-doomed/) where I suggested to my colleagues that the bubble we have witnessed is in duration. We saw this first happen in 2020 peaking in December of 2020 in the amount of negative yielding debt in the world. This is in nominal and not real terms. It peaked at over $18 trillion and now has plummeted to $2 trillion. I still wonder why there is any. However, the combination of central banks taking real rates negative combined with regulation such as asset liability matching (pensions), Basel III (banks) and Solvency 2 (insurance) forced these institutions to buy long term sovereign debt. It was the financial repression Reinhart and Rogoff spoke about in “This Time is Different”. The poster child for this trade was the Austrian 100 year bond which during 2020 outperformed even all of the FAANG tech stocks. Everyone needed duration. We also saw this lead to a move below zero of the term premia in the bond market, or the extra yield investors demand to hold longer dated bonds. They were demanding less (blue, inverted) to lock up their money for longer. This makes no sense in theory or in practice yet it still happened. Thus, the TINA (there is no alternative) market developed and this meant that assets with zero or negative cash flow (but a lot of EXPECTED growth) were en vogue elsewhere too. We can approximate this by the performance of growth (mostly tech) vs. value (energy and fincls) and by Bitcoin. As the duration bubble goes away, so too will the performance of assets that benefited from it

Drilling into some specifics, we can look at the SPAC Index, that measure of companies with no earnings that came to market via special purpose acquisition corps instead of via IPOs where investors were more discerning. We also saw a bubble in private markets as proxied by the PSP private equity index. If companies could see an exit strategy in not just acquisition or IPO but also SPAC, it meant private investors could afford to pay more. This benefited the innovative public stocks like FinTech (ARKF here) as well as the disruptive tech embedded in crypto (BGCI here). This is all being unwound now.

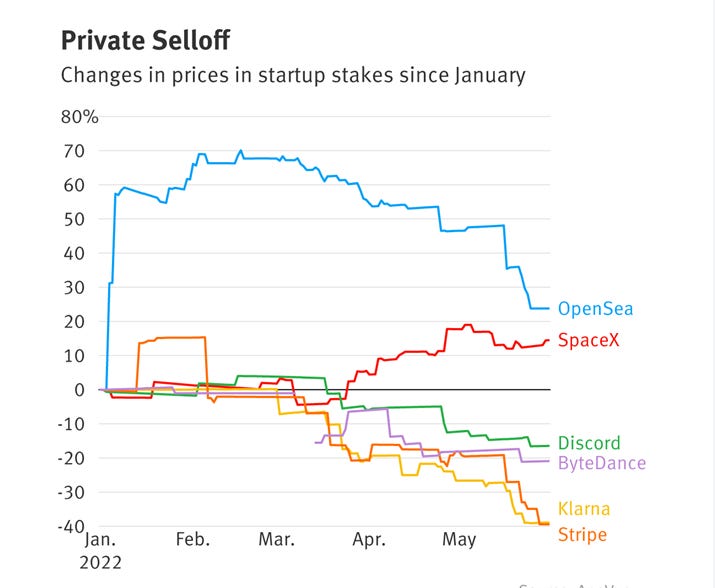

Some specific venture companies, that were worth billions, have seen their values plummet in the private market because they could not get to the exit soon enough. OpenSea is the NFT platform. I think you know the other names. No ones capital, in public or private markets, has been safe.

It all comes back to that original point about the growth of money that had nowhere else to go. With money growing but not as much need in the real economy as many companies have moved to asset-light business models, it must go somewhere. It makes its way into financial assets, ultimately in the most speculative. It also goes in search of yield for a yield-starved world. Recall the amount of negative-yielding nominal debt at $18 trillion? How can an aging Japan, China, Europe and US afford to retire on 0% or negative rates? It cannot. Thus is must take risk and it seeks yield. Where was the yield on offer? DeFi offered the best yields. People were attracted. We can see how Ether benefited and Bitcoin was dragged long too. However, monetary policy acts with a lag. As money growth slows rapidly, from all-time high levels, so will it come out of these assets. After all, one can get almost 4% in US Treasuries now. That 6% yield in crypto does not look nearly as attractive to many investors even before the capital losses.

DeFi and its disruptive power of the financial services industry is the prime example. Industries are most likely to be disrupted when consumers have a negative view. Think cable TV. Think bricks & mortar retail. Does anyone have a positive view of the traditional finance world - investment bankers, hedge funds and the like? Having worked at investment banks and hedge funds I can tell you they do not. Even my parents cringed when telling their friends of me. Well, here comes DeFi to disrupt the TradFi world and offer attractive yields via this new technology called a smart contract. The measure of the usage of smart contracts is in total value locked (TVL). We can see that the usage of smart contracts peaked in January of 2022 and is off about 70% since. This value creates the fees that are the fundamentals of DeFi and the tokens involved. The fundamentals are still declining.

As such, the desire to trade these tokens has also fallen considerably.

The desire to borrow to trade or to provide liquidity has also fallen.

Which means as the fundamentals fall, the token prices will fall doing a round trip from the October 2020 lows.

This leads to things breaking. First, we had the Terra/LUNA algorithmic stablecoin break and go to zero, presumably costing investors $50bb. Then we had another popular DeFi protocol called Celsius break. Both of these were offering 20% + yields. Terra did it via marketing spend as well as from the fees in LUNA as popularity grew. Celsius told investors it was going to loan out the tokens to stake ETH elsewhere. This happened in TradFi in the GFC. We called it rehypothecation. Investors kept their assets at prime brokers who were able to offer more attractive financing by being able to loan out these shares whenever and wherever they wanted. It worked great until the original investors (the stakeholders) wanted their capital back. It just takes one domino and all the rest fall. Well Terra was perhaps that domino. Now then Celsius fell and now we here the largest crypto hedge fund - Three Arrows Capital - is also being unwound. At least those are the very loud rumors. It was an $18 bb hedge fund. If we assume even modest hedge fund leverage of 4x, that is another $70 bb in investments being unwound. There is quite the pain in crypto. This will take time to heal, maybe even more so than the crypto winter of 2018-2019.

These type of unwinds follow human nature. There is a model in psychology that represents this called the Kubler-Ross grief cycle. It discusses how humans handle tragic loss, typically associated with dying. However, it works pretty well with investing too. Right now, we are probably somewhere near the Bargaining phase, where investors are struggling to find meaning, reaching out to others, telling their story etc. This is the capitulation type of phase in markets as people start to give up. We are past the point where people are angry and want to fight, telling those that sell they are wrong. The Depression phase is when prices stay low for a long time.

However, I want to stay positive in some ways. I did a study many years ago that looked at the top 10 stocks in the Nasdaq. What if I bought the ten largest Nasdaq stocks in 2000 and held them until 2018 (the time I did the study). This assume I had the worst possible timing of investing. What I found is that even if I had invested at the worst possible time, I still made money over that 18 year period. Of course, I would have lost about 80% of my money from 2000-2002. Of those 10 stocks, 3 of them went to zero. Another 3 of them were basically flat. However, the others did remarkably well. After all, the reason they were the 10 biggest in the world was that they were terrific and disruptive companies. They adapted and changed the world the way we thought. This is an example of one you may have heard about - Amazon. It was up about 7000% in the late 90s. Then it proceeded to go down 95% until the 2002 lows. It proceeded to bounce 63000% over the next 20 years. Point is, if you buy amazing companies, even at the absolute wrong price, it can work out. However, I don’t want to be naive. Recall I said 3 went bust and 3 more were flat (0% return over that 18 year period). So you have to have a portfolio of these. This is the Babe Ruth Effect of venture investing that I referenced before.

What is the indicator to know when it might be safe to get back in? Well, the first I would tell you is to understand anecdotally at least, where investors heads are at. Where are they in the Kubler-Ross model. Why? Because unless you are the 800 pound gorilla of investing, you need other investors to follow and drive prices higher. However, the next best thing is to watch the financial conditions. Jay Powell has mentioned this indicator multiple times. It was developed by Bill Dudley when he was at Goldman, before he went to the NY Fed. When it is rising, financial conditions are getting tighter and you want to be in safer assets. As it falls, financial conditions are easy, and people take more risk with their money. I have plotted it here vs the bond vs. stock ratio, a measure of total return in Treasuries vs. SPX. You can see it fit extremely well until about 2015, when a combination of FAANG enthusiasm and central bank interference in the bond market started. It became very dislocated in 2020, the bubble in duration years. It is struggling now because we have inflation. So, Treasuries might not be the asset to watch even if financial conditions are.

I look at it here vs. a ratio of gold to Russell 2000 small cap stocks. It is another attempt at measuring ‘safe’ assets vs. ‘risky’ assets and comparing it ti financial conditions. You want to stay in safe assets at a time like this until the measure peaks and heads lower. We still have some distance, and time, to go.

You know I love overlays. However, no overlay is perfect. It can give us an idea of what we can expect. We are in the midst of a major deleveraging of DeFi and other assets. This will take time. This will cost money. Time may heal but we measure it in years and not weeks. Don’t look for a quick snapback, and if we get that, fade it. Remember the chart from a few weeks ago, this is a waterfall decline. However, the positive is that there will be amazing companies and amazing assets that trade to bargain levels. This does NOT mean all previous high fliers are a bargain. It does mean there will be amazing bargains though. In addition, there will be new players to step into the void. Facebook and Google were major forces in the internet revolution but did not go public until after the unwind.

Don’t be in a hurry to rush back in. Watch for the indicators. Listen to the pain being felt by others. Most of all …

Stay Vigilant