How will you vote?

No, not on the election, on the forecast of growth and inflation

Benjamin Graham has lots of good quotes, but perhaps one of his more famous is “In the short-run, the market is a voting machine, but in the long-run, it is a weighing machine”. The quote is in reference to how sentiment may drive prices in the next day, week or month. However, the fundamentals of a business, that determine its ability to generate and sustain cash flows, will determine the path of price over many years. This quote is somewhat corroborated by quantitative evidence as well. Savita Subramanian at BAML did a study a few years ago that showed over a 1-year time horizon, valuation has no statistical significance on stock performance. However, over a 10-year time horizon, it is the only statistically significant variable.

This week, the US goes to the voting booth, not to choose stocks, but instead to choose the next President. While there are many thoughts about which candidate is good or bad for the economy, the Congressional Budget Office scored each of their set of policies. (An aside: it is really difficult to even know what the policies are as neither has a cohesive set of plans, but instead a number of disjointed thoughts during stump speeches.) That said, the CBO determined that the deficit would grow under each candidate. Perhaps this is why the bond market has had yields move straight higher since the FOMC decision to cut by 50 basis points.

You can see that in the last 6 weeks, 10-year Treasury yields have risen by 76.6 basis points (white line). I have overlaid a couple of other possible drivers of this move. The first is inflation expectations in blue. For this I look at the 5 year/ 5 year forward inflation expectation from the swap market. This level has risen by 20 basis points over this period of time, explaining about 25% of the move.

The second possible driver, actually the largest driver, is the term premium in orange. The term premium is the extra amount investors charge for locking up money longer term. This has been suppressed in an age of financial repression by regulators and central bank QE. Perhaps, however, this is starting to reverse. Over the past 50 years, the 10-year term premium has averaged about 165 basis points. Since the Great Financial Crisis, the term premium has averaged 33 basis points. Since Covid, it has averaged -100 basis points. You can see the massive impact that central banks and regulators have had on the bond market. Well, over the last 6 weeks, the level has risen from -25 basis points to +22 basis points. Still below the average since the GFC, and well below the average over the last 50 years, but well above the post Covid ‘norms’. This explains another 61% of the move.

Is this the bond vigilantes telling politicians that the rampant fiscal spending has to end? I think it may well be. To give an idea of how large government has become relative to our economy, many are touting the strength of the recent Q3 GDP number at 2.8%. The government contribution to this number was 0.9% suggesting that the true economy is growing at a more pedestrian (but still positive) 1.9%. This level of growth does not suggest we see SPX earnings growth in the double-digit range as expected (more below).

I tend to agree with the bond vigilantes on this one, but the trade may be a little crowded in the short-term. The left chart comes from the October BAML Global Fund Manager Survey. It shows a record outflow from bonds the past month (ending mid- October). The magnitude was the largest this century. Are investors telling officials that rates below 4% are simply not attractive? What does this mean for the government’s ability to fund $35 trillion and rising in debt? On another note, the real bond vigilantes - levered bond funds - are the shortest US Treasury futures they have been in the last 5 years. This may suggest that in the near-term, it could be harder for yields to rise. However, I think both show you how investors are feeling about rates. Remember my scenarios from a few posts ago? You think more people are worrying about a 1970’s redux?

Rates definitely factor into my views too. Why? Because I care about housing, as I feel it leads the economy into and out of recession, into and out of growth mode, into and out of every cycle. This is H.O.P.E. Housing leads (new) orders, which in turn leads profits and then employment.

The white line is total US housing sales. It is abysmal. Much of the focus on housing is on new home sales, which is an important but smaller (10-15%) of the market. Total sales are at the lows we saw in the Great Financial Crisis. This is why new orders continue to struggle. We have yet to see the impact on profits or employment yet. I think we will.

This is a super busy chart but let me explain because this is 100% the housing market dynamics right now. The blue line is new home sales (read Millennials). The white line is existing home sales (read Boomers who want to move). The purple line is the mortgage rate. The orange line is household formations i.e. people starting families and moving in together. You can see that the blue line and the orange line move together. Millennials are forming families (even if it is two dogs instead of kids) and buying new homes. This has been happening for 5 years and most expect it to continue for the foreseeable future. The white line and the purple line move in opposite directions. As rates move higher, no one is selling their existing home and moving. They are locked into a mortgage around 4-4.5% and won’t move to pay a higher rate. In fact, even at 6.68% it is not attractive for this supply to come on the market. It really needs to be nearer to 5% or lower. Again, this is good for the builders because this supply is competition. Think of a young family buying a house – they can buy someone else’s house (usually closer to town) or they can get something brand new (usually further away but with no headaches). This is the trade-off. This is a major tailwind for builders right now, but it is not a tailwind for the economy.

I wrote about this a lot on LinkedIn this week. Here are those posts back-to-back.

Chart of the Day - economy update

Had a travel weekend with friends this weekend as we traveled out to Oregon to taste some wine & go to an Illini game in Eugene. If you haven't visited this part of the country, especially in the Fall, do yourself a favor & make the trip. Absolutely beautiful

While the Ducks fans were incredibly hospitable at the pre and post-game events, they didn't treat our team very nicely on the field as the Illini were clearly outclassed by a much better team

The wine events on both Friday & Sunday were quite fun and while we moved around from town to town, it definitely had the feeling of an economy that is solid but not spectacular

That is the vibe I get most places I have visited. Solid but not spectacular. That is the soft landing that is clearly consensus in the market. Whether that will be good enough to take stocks higher, we shall see

As we look deeper into 2025, it will all hinge on housing. Publicly trade builders are still doing fine & have an advantage over the smaller builders that rely on bank financing. That is presumably a reason the Fed decided to be aggressive. These builders need to bring on supply but don't have funds

In addition, the 85-90% of the housing mkt that is existing homes will not come on until mortgage rates get well below 5%. People's locked in rates are just too attractive to move right now

What have mortgage rates been doing? You can see in the chart today it is back up to 7.21%. Looking at this technically, and I know it isn't traded on a mkt, might suggest that while it is 'overbought' near term, it is likely breaking out higher and headed back to the 7.5-7.6% range

That would not be good for the housing market next Spring. If housing isn't a catalyst next Spring, that spells bad things for the economy which spells bad things for the labor mkt

This might factor into the Fed's calculus next week as it meets. Of course, the risk is it is too aggressive, and inflation re-ignites. It is a bit of a balancing act right now

For those that are looking at no landing, which is a growing percentage, I think you need to focus a lot on the housing mkt. That price action is going the wrong way

Chart of the Day - mortgage spread

Building on my post from yesterday and the importance of housing, I wanted to look at the mortgage spread. What do I mean by mortgage spread? I look at the difference between the 30yr mortgage rate & the 10yr Treasury yield

For me this is the proxy of what the banks are charging people vs. where they can hedge themselves, taking the credit risk (when they don't lay it off with Fannie & Freddie)

You can see in the top chart, that this spread has a good relationship with the NAHB housing index which I have overlaid and inverted. When this spread widens, it coincides with a weakening housing index. When this spread tightens, the housing index does better

This isn't surprising because this spread impacts the price of the loan. You can see right now that this spread is near 3% which is among the highest it has been this century

In the bottom chart, I overlay this spread with the Chicago Fed Senior Loan Officer survey of CRE loans. This is a proxy for the banks willingness to make real estate loans, which impacts this spread

Again, you can see both of these measures were near their highest of this century in 2023. Over the last year, the Chicago Fed measure has been moving lower i.e. banks are becoming more willing to make CRE loans

The mortgage spread has not caught up yet but if history is any guide, this would suggest a good amount of downside back to the longer-term average of about 1.7% vs. 2.96%

This might suggest that all else being equal, if the 10yr Treasury stays at 4.2%, the 30yr mortgage rate could fall from 7.16% to 5.9% just from the impact of this mortgage spread normalizing in line with the Chicago Fed senior loan officer survey

This would be good news indeed for the housing market. This would be good news indeed for the economy. This might make the Fed's job a little more difficult if it led to a re-ignition of inflation but that is another story for another day

From a housing perspective, this could be a positive

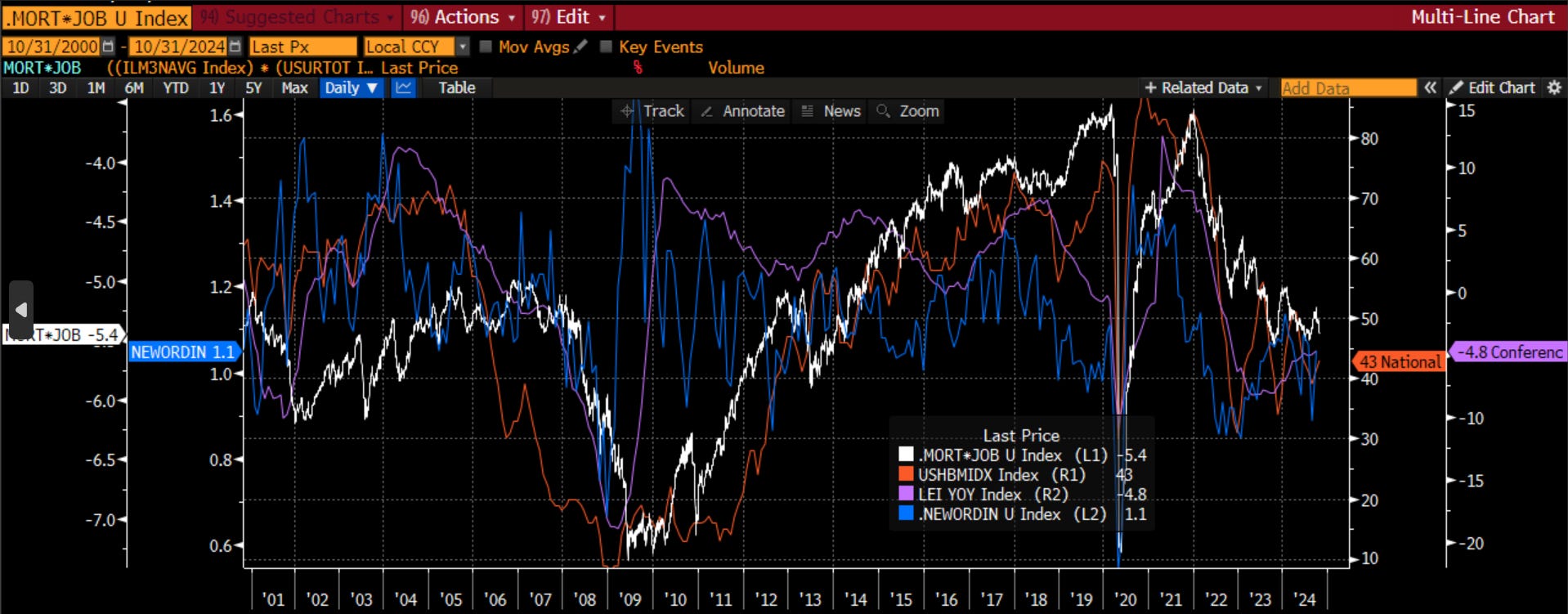

Chart of the Day - mortgages & jobs

Continuing on with the focus on housing this week, I want to look at some other factors that may be impacting the housing market

We saw on Monday that the mortgage rate is perhaps moving in the wrong direction right now if we want to see a continued improvement in housing. However, yesterday, there was some hope that the mortgage spread to 10yr could narrow which would be helpful

Today, there are three other things that I want to look at to see what the impact on housing may be

The first is an anticipatory indicator, that should lead even the leading indicators. For this I use the ratio of ISM new orders to inventories in blue. When orders are rising/inventories falling, this is a healthy sign for the economy. When orders are falling/inventories accumulating, its bad

The second is the leading economic indicators from the Conference Board in purple. A tried & true measure that leads economic activity

The third is the mortgage rate but multiplied by the unemployment rate in white. The logic is your decision to buy a house is a function of the cost of capital surely, but it is also a function of how healthy you view your job. A lot mortgage rate does ntg if you fear for your job

I compare all to the NAHB housing index in orange. We can see they all directionally move in the same direction, with some leading vs. others. As the GFC was led by housing first, it is not surprising to see housing move into a recession first, but come out of it more slowly

Most importantly, as we look at the data right now, all seem somewhat depressed, lingering at levels we saw back in 2013. This was not a recession for the record, however, it was also not characterized as a robust economy either

The data also continue to meander near the lows, showing no real signs of picking up any time soon. It may be too soon to call. The economy still looks like it it set to grind slower. Call it a soft landing if you will

What I find interesting, is that to me, the stock market continues to rally like it is a bull mkt in the economy. The economy leads earnings and earnings lead stocks. The expectation of earnings is much higher than the economy is suggesting (will look at that tomorrow)

Thus, the disconnect may not be that the market's view of the economy is wrong, but what is priced into stocks is wrong relative to the view of the economy. I will look at this tomorrow

For now, solid but not spectacular might be the view based on this data. If there is risk to that forecast, it seems less than solid is more likely than robust. 1-2% real GDP likely with a risk of below 0% higher than a risk of >3% in other words

Chart of the Day - solid but not spectacular

The posts this week have focused on housing & the economy. The conclusion I keep coming to is that the economy seems solid but not spectacular. I characterize this as 1-2% real GDP. This is not the 3%+ we have seen. It is also not below 0%

So, the question is 'what's the problem, that seems just fine?' This is a completely fair question. That is fine. This may even let the Fed reduce rates some more. Perhaps jobs hold on just fine as well. All good, right?

I think the problem with this scenario is that to me, this is not what stocks are pricing in. With the earnings growth we see for the SPX of 10% next year and 13% the following year, we need more than 1-2% real to get there

RTY has earnings growth of 30% for the next year and 12.5% the following year. Is this realistic?

If you look at the chart today, I plot the real GDP on a yearly basis vs. the best estimate of SPX and RTY earnings for the year. The growth rates are not on here but SPX expected to grow as above

You can see that the SPX has been punching well above its weight based on what the GDP would explain. You might suggest that this is perhaps because of global growth, however, Europe & China both appear to be in a recession right now

In fact, according to CapIQ, international revenues were down in Q2_24. The percentage of revenue coming from abroad was 28.9% which is down 202 bps. Thus, it is not international revenues driving this growth

The Russell is more domestic, and you can see earnings here have more closely followed GDP, but again, are well ahead of current growth, much less the expected growth to come. Hard to see GDP moving lower from here but earnings accelerating to the upside

So, the answer to the question 'what's the problem, that seems just fine?' becomes 'because much better than that is priced into the market' As investors, we care about the fundamentals for sure, but we care just as much about what is priced into the securities we are buying

In order for the securities to move higher, we need to see upside surprises to the level of growth priced in. If the economy is going in the wrong direction, it becomes that much more difficult to financial engineer our way to more profitability

Unless of course companies start firing a lot of people. Which impacts housing. Which impacts the economy. Which increases the odds of recession. Which brings in more downside for earnings

You can see where I am going

Chart of the Day - Blue Angels

Yesterday I suggested the economic growth in the economy was headed lower, not dramatically so, but lower and not higher. I suggested the problem with this is that the market was pricing in a much better outcome

The chart today shows that better outcome more clearly than I did yesterday even. I remember being introduced to this chart by the venerable Ed Yardeni (a perma bull even if he says he isn't) who called it the Blue Angels because it looked like the tail stream from those airshows

This chart shows the current year earnings (yellow) and the following two years estimates (blue, orange). I overlay the price of the SPX on here. I think this chart does a really good job of showing when the market is overly optimistic or pessimistic

Look at the last 10 years to see what I mean. When prices are plodding along much closer to current earnings, the market is not giving much credence to future growth. For whatever reason, the market is not seeing a high possibility of this

However, it eventually begins to rise and then starts tracking next year and at some point, enthusiasm kicks in, and the market is trading off the next two years of growth

Once we spend time and are trading at that level, there is ultimately some disappointment. We can see that in 2018, 2020 and 2022. We started trading off the fwd 2 years and before long, the mkt corrected even if this didn't mean earnings fell considerably

Look where we are now. We are again at that fwd 2 years growth. Sure, if history is a guide, we can stay here for several months as we saw in 2021 when the market defied gravity for quite some time driven by surplus liquidity

That said, we didn't stay at this level for very long in 2018 or 2020. You can blame the latter on Covid, but the economy was beginning to look weak even before Covid so it isn't clear we would have anyway

I am not hear to call for a major crash in stocks. That isn't the point. My point is about what is priced in and where is the scope for surprise - is it to the upside or the downside?

We are at the highest end of expectations. For me, the scope for surprise is the economy continues to grow at slower and slower pace, because housing does not recover like many think it will. I could be wrong. Maybe there is some other surprise like higher than expected fiscal spending as we have seen the last two years

Does this mean no Santa rally this year? Not at all. Does it mean that allocators may find that stocks are a bit more fully priced and want to rebalance maybe even more than expected into other parts of the market? That could be likely

Know what you are paying for before you make that decision

________________________________________________________________________

So, in summary, you can see where I am going with all of this. The key to the economy is the housing market. The housing market, existing home sales namely, is driven by mortgage rates. Mortgage rates are tied to 10-year yields. These bond yields may be moving higher in the medium to long-term because the bond vigilantes see rampant fiscal spending requiring a higher term premium and potentially leading to higher inflation. This will slow the economy from the 2.8% (really 1.9%) growth to something slower. This lower growth will make it difficult to grow earnings at the double-digit levels that are priced into stocks.

In the next month? All of this could be wrong. Bond yields could go lower because of crowded short positioning. Stocks could head higher because of TINA (listen to the podcast with Mr. Risk) and because of strong Q4 seasonals.

Into the next year? These are the issues, questions, and considerations all investors need to be considering as we rebalance portfolios for 2025.

Stay Vigilant