I'm not sayin', I'm just sayin'

Investors responded to the jobs number thinking the bull market is about to accelerate. I'm not so sure

After the much better than expected 254k non-farm payroll number, which included a better-than-expected household survey, bringing the unemployment rate down to 4.1%, financial markets and financial X responded by acting as if we are back to the bull market of 2021 which gave rise to the meme above. In fairness, this number was a bit of Goldilocks on the surface, with growth good enough to push off recession and earnings collapse fears, inflation probably not a concern (though we will know more on Tuesday) and discount rate solidly moving lower. This is the perfect cocktail for the equity market.

Raoul Pal had this picture posted on LinkedIn suggesting total global liquidity is set to rise considerably, which will take risky assets like Bitcoin higher. He argues recently announced Chinese stimulus is not even in the number:

I saw a similar idea that someone shared from the FT/Cross Border Capital suggesting liquidity is marching higher (though sadly I can’t find it to share it). Though we should not be surprised, because as Michael Hartnett at BAML shows, September was the 4th largest month for central bank cuts this century. This is shocking to me. Think about the months around the Great Financial Crisis or Covid or the Tech Bubble. However, here we are with many markets at all-time highs and central banks are stimulating. STONKS!

Though, not everyone is on board. Eric Johnston at Cantor Fitzgerald, a noted equity bear, has his own measure of liquidity which is the largest central bank balance sheets, TGA and reverse repo. He sees this going the wrong way. Something to watch.

Clearly, another concern is that pretty much everyone is on board with this rally. The consensus CAN be correct of course. However, when everyone is leaning one way, with leverage, it makes my antennae perk up. This chart (also from EJ) shows that non-dealer positioning in S&P futures are at levels we have not seen in a long time.

So, maybe there is money sloshing around. Maybe it has been put to work long stocks. It doesn’t matter right? After all, growth = good, inflation = falling, rates = falling. Thus, as Will Smith used to say, “it’s all good”.

Unless of course, the market re-assesses and all of a sudden realizes that maybe the FOMC was closer to what could happen instead of the market which was much more dovish. In fact, the market has moved toward the FOMC dots, not the other way around. The green lot is the FOMC median. The blue line is where the market was right after the September FOMC meeting. The white line is where the market is today. That didn’t take long. Growth is good, however, growth MAY not mean a fast normalization of policy. Imagine if CPI comes in hotter than expected?

This move impacted the 2-year yield, which has bounced sharply the last few weeks. As the short-term rates adjust, one can only expect the earnings yield of the SPX (inverse of P/E) to adjust too.

That is on one leg of the stool supporting stocks namely the discount rate leg. The other leg that could get wobbly is the ‘gently falling inflation’ leg. What could impact this? I have a couple of ideas. First, is the most obvious, oil. WWIII may be erupting in the Middle East and right now, few in the markets seem to notice though it is all over my X feed. If they do notice, they have become numb, which I do understand as the market moves less and less on these geopolitical events until and if they ratchet up. Could this happen after Yom Kippur this Friday?

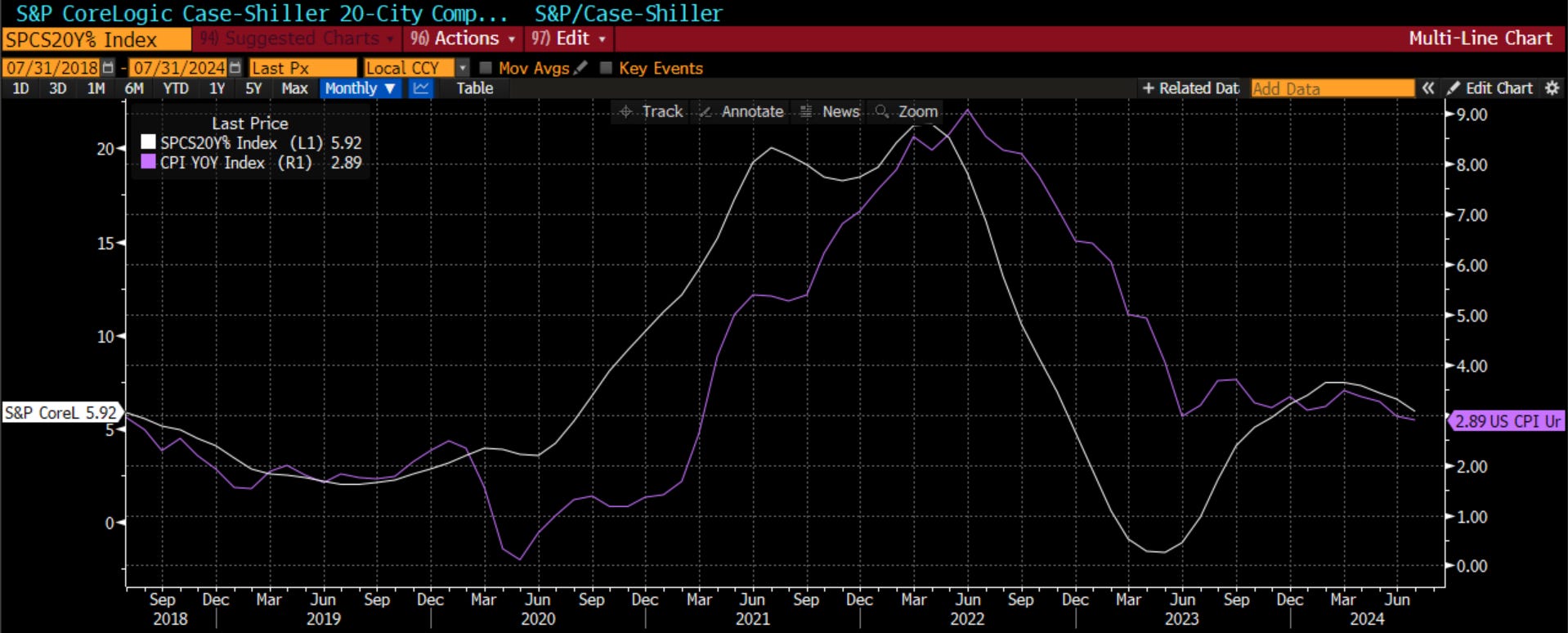

Okay, but maybe that doesn’t worry many people because gas prices are down so much right now. However, what about those Millennials that saw the Fed cut rates, mortgage rates drop, Kamala want to give them money, and said ‘honey it’s time to buy a house!’ Well, house prices are going higher. Mortgage rates are not nearly low enough to bring on those with a 4.5% mortgage or lower, so this money is still chasing limited supply. This data is lagging, but is still rising, just at a slower rate. Should it pick up, what is the impact on CPI?

My old buddy Milton Friedman (I still have the VHS of his Free to Choose - it is legendary) says inflation is always and every a monetary phenomenon. This is the change in M2 leading CPI by a year. You tell me:

His acolyte, John Cochrane, has changed the narrative, maybe more fit for this time, in his book about fiscal policy saying inflation is always and everywhere a fiscal phenomenon. With hurricanes and FEMA disaster, money going to Ukraine and the Middle East, and neither candidate looking to restrain, which way is this headed?

Finally, just a couple more charts on the growth side. That number was really good. However, there were some internals in the number that I think are simply interesting. It does not detract from the strength of the number but it is worth knowing. Francois Trahan, another current market bear, suggests that the Conference Board jobs hard to fill (which we also mentioned recently as part of a ratio) suggests unemployment still may head higher.

I thought this data brought up by Dan Greenhaus on LinkedIn was also super interesting. He pointed out how job growth for foreign born workers is vastly outpacing job growth for native born workers. Sure, there is a base effect on the growth rate. However, do you think this may have ANYTHING to do with the negative view from people on immigration? Do you think this may matter for the election?

Last chart, I promise. This is the breakdown of the blow-out jobs number. A big part of it was driven by part-time and education. It was back-to-school after all. So, before you extrapolate it into a trend that will carry us through 2025, you might want to wait for confirmation.

Earnings start this week. We also get CPI. Then Yom Kippur ends and we see how, not if, Israel retaliates and what it means. There is a LOT going on. For me, it is still time to …

Stay Vigilant