It's time for the vigilantes

You are all vigilantes. You wouldn't read this if you weren't. However, this week we step aside for the OGs of vigilantes

Courtesy of Creative Destruction Media

You know I love vigilantes. Anyone who is staying vigilant about any particular topic, is a certain kind of vigilante. In the past few weeks, we have seen the return of the bond market vigilantes.

The term bond market vigilante was coined in the 1980s by Ed Yardeni. He was describing the behavior of the bond traders who sold Treasuries in response to the policies of the Federal Reserve and their impact on the economy.

This fear of the bond market and its impact has existed ever since. There is a famous quote from James Carville, a Clinton political advisor. Per Wikipedia, this is the background and quote:

Intimidation to be sure. As I tell everyone of my classes, from Freshmen to 40 year olds, the 10-year Treasury yield is the one thing they need to focus on the most. It is the rate that underpins everything in finance - other US government bond rates, other sovereign bond rates in Europe and Asia, corporate bond rates, mortgage rates, commodity curves and equity valuation. Everything is driven by this rate as the anchor rate.

That is one reason why the ridiculous debt ceiling stand-offs that threaten to default on Treasuries are so dangerous. Most times the market brushes it off because rational people know that it would be a calamity for the global financial system. However, with people in charge these days, on both sides of the aisle, can we continue to rule this out?

It is also why the downgrade by Fitch is a much bigger issue than many let on. Sure, in and of itself, nothing is going to change. There are no investors - pension funds, insurance companies, bond funds etc. - that will sell their holdings as a result. However, it does mean we are one step closer to that potential calamity. We are not trending in the right direction. Seems we might want Bob Rubin back at the helm.

While it did not and will not cause meaningful portfolio change, it has meant that US Treasury yields are back to the highs of the last year:

There are a plethora of reasons and implications for this. I will try to cover some. I covered some others in the “Excell with Options” piece I write for CME Group. This past week I looked at the supply and demand for Treasury products given the higher issuance we will see in the coming year. You can read that here

This all comes at a time when bond investors seem to be strongly in favor with bonds. Whether it is the declining inflation or the expectation of a recession, institutional investors prefer bonds. This story on the topic just came out tonight on Bloomberg titled, “Bond Bulls at JPMorgan, Allianz Double Down on Bet Gone Bad”

https://blinks.bloomberg.com/news/stories/RZDZ40DWRGG1

The inimitable Mr. Risk at State Street had this chart in his publication this week, referencing the JP Morgan survey of bond investors. It shows investors on net love bonds.

However, faster money - leveraged accounts, hedge funds, CTAs - are taking the other side of this trade. If we look at the CFTC Commitment of Traders report that I get from the CME group website, we see that the leveraged money is at the biggest net short position we have seen since 2006 (probably longer but that is all the data had)

From a technical standpoint, the bond yields still look to be headed higher, which means the bond futures would be headed lower (thus one reason leveraged money may be short). You see in the first chart I showed above, that while we are at the highest in 1 year, the moving averages are turning higher which is a bullish (for rates) sign. Then, if I turn to the weekly chart, I see that the pullback in yields we saw this year held support and have inflected higher. The weekly MACD has crossed over and is moving higher and we are not yet overbought. This is a pretty strong signal to be short bonds and long rates.

Of course bond investors are long term holders, and don’t care about these short term charts if they are going to hold these investments for 10 years, right? Let’s look at that chart of yields on a quarterly basis going back 50 years. This is starting to look like we are breaking out of the 40 year bear market in yields/bull market in bonds. There may be a seismic shift taking place in the investment landscape. Bond investors who have spent their entire career in a bull market, may be anchored on ‘buying the dip’ in bonds. The same way these same investors criticize equity investors for buying the dip in equities.

Who are these investors? That may be changing a bit too. Global investors have preferred to hold Treasuries in a dollarized global economy because of the depth of the US markets. However, in China and Japan, two markets that are the biggest Treasury holders, their currencies are weakening and US bonds are not nearly as attractive. I wrote about that this week on Linked In:

Chart of the Day - FX

The last couple of days I have been discussing the problems in China that are percolating to the surface in real time. I didn't even mention the youth unemployment rate which is so bad it won't be published any more. I am sure I will get intel on that from my grad students next week

However, those problems are leading to a Chinese Yuan that is weakening to the weakest levels since last October, which themselves were the weakest since the Great Financial Crisis

I have also spoken about Japan & the BOJ, where even widening the yield curve control so rates could move up to 1% in the 10years is not enough to stop the Yen from weakening as well. It is also approaching last Fall levels, where the BOJ intervened as those were the weakest since the late 90s

I bring these to FX rates up because there is a correlation between the weakest of these currencies & the US 10 year Treasury yield. Correlation is not causation but you can see from the chart today, there is a pattern here that may not be perfect but is informative

You see, China and Japan are 35% of all foreign holdings of US debt which amounts to 14% of the total holdings of US debt. Weaker currencies mean these holders will demand a higher yield in order to compensate

Which is the chicken and which is the egg is really not that important as there is an interlinkage between the weakness of the FX rates & the yields. This impacts all of us whether we know it or not

The 10 year yield is the rate that underpins the pricing of all other assets in the market. We see yields on other government bonds widen as the US yield widens to levels also not seen since last October

We see the rate required on corporate bonds also widen when the benchmark rate widens. This means the cost of funds for any companies investing for growth - whether that by software capex or reshoring - are more expensive

It means our mortgage rates for houses are going to be more expensive. The average 30 yr mortgage rate moved above 7.5%, the highest since 2000. Higher 10yr & wider spreads mean housing is even more unaffordable

Higher yields mean commodity curves move up as the carry cost for these products is more expensive. This will impact inflation

Higher yields mean that PEs for equities must come lower too. This is the impact we are seeing on the most expensive tech stocks in particular in the past week or so

If you got in late to the trades, you might want to consider some stop/losses. If you are sitting on cash, you may be given an opportunity if you are patient. Either way you should speak to your financial advisor for guidance

Most importantly, you should Stay Vigilant

This is the chart of higher yields and the forward P/E for both SPX and NDX. These markets have been ignoring the move until the last 2 weeks. Can this continue? I am not so sure it can. This does not mean stocks have to go a lot lower. Earnings can carry the day. This past earnings season was once again better than expected. As we get past Labor Day, we will have a number of industry conferences where companies can tell us about the last quarter of the year and next year. Investors are pre-disposed to want to buy stocks (we have talked about that behavioral bias post Labor Day before). However valuation is going to have to suffer.

While corporate credit spreads have narrowed, higher US 10-year yields mean higher corporate borrowing costs in absolute terms. Growth capital is getting more and more expensive:

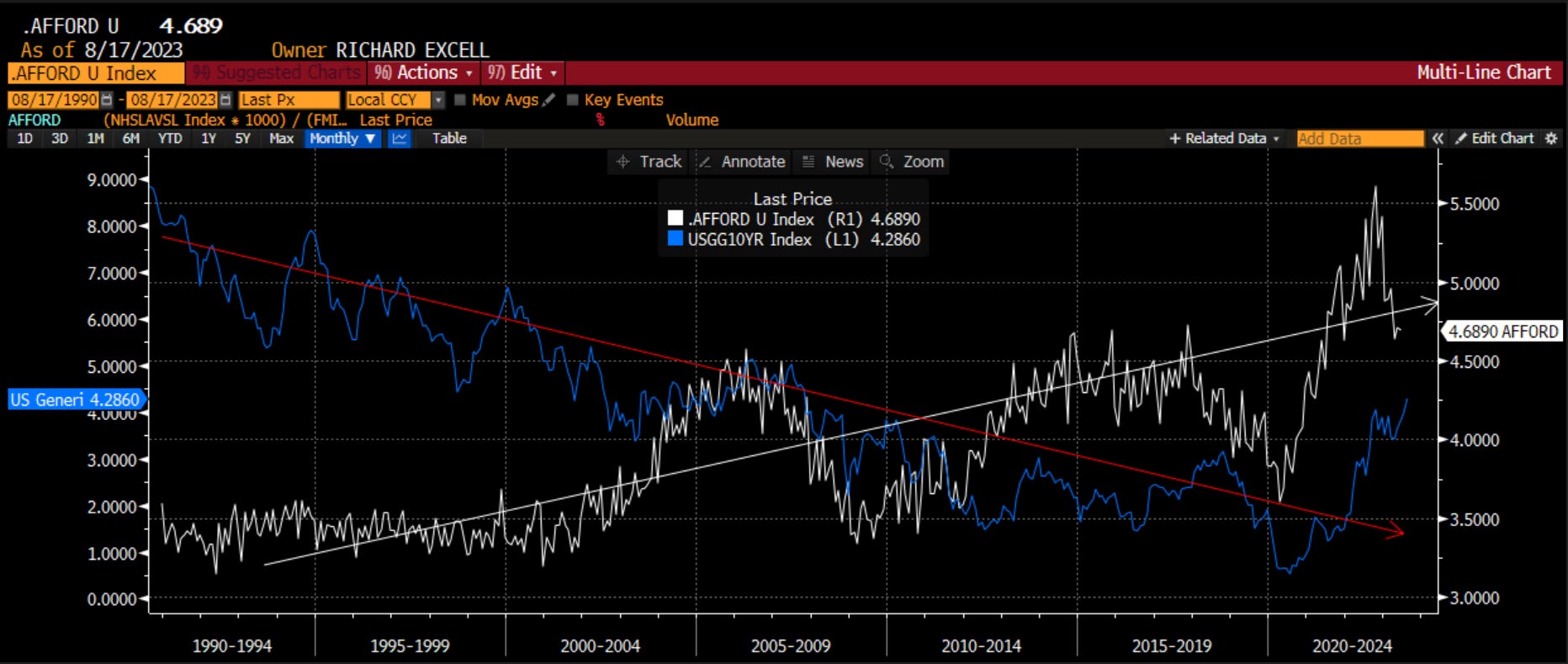

Most importantly, it continues to impact the cost of a mortgage. I wrote about this in two different LinkedIn post this week on affordability. The first looks at the long term trend in US interest rates and what this has meant for the multiple of one’s income they would be willing to spend on a house:

Chart of the Day - affordability

Yesterday we looked at US 10yr yields & showed how the weakness in FX like Yuan & Yen may be pointing to higher yields. Today, global govt bond yields reached their highest since 2008 as global data continue to be better, suggesting central banks aren't finished

Today I wanted to focus a bit more on housing because it is so central to the economy & so important to most people, who either have most of their net worth tied up in a house or aspire to one day

The chart today shows two things - US 10 yr ylds in orange & a housing affordability measure in white. I have added two arrows to show the long-term path of each

We all know that we have been in a 40 yr bull mkt for bonds leading to lower yields over time. There is a big cohort that feel that due to too much debt, retiring Boomers & technology like AI, this trend will continue toward lower ylds for years to come

I am personally more in the camp that we have seen the low in yields & they will stay higher for longer. Reshoring or near-shoring is happening. The energy transition is happening. Wage gains are happening. All of these point to higher prices/inflation/yields imho

The white line is the median sales price of a home in the US divided by the median income in the US. It is a measure of what multiple of one's income you need to spend on a house

When I was first buying a house in the early 90s, the rule of thumb was about 3-4x your income you spend on a house. This was already higher than the 3x my parents used to gauge what to spend

You can see that the median sale price to income stayed around this 3.5x thru the early 2000s. Then it embarked on a journey higher. Much higher. Coincident with the trend of lower & lower ylds

This number peaked at 5.5x in 2022 at the height of the house-buying frenzy post Covid. Money was still essentially free & every Millenial decided they needed a house in the suburbs, which meant every Boomer had a chance to move somewhere warm

However, this 5.5x, even 5x, is unsustainable particularly if we are in for higher yields ahead. One can hope to refi lower if one believes we will see lower ylds in the future, but will we? 5% govt bond rates & a 7% mortgage rate are not high, they are normalized

So how does this affordability measure continue to drop from 4.7x now back to the avg of 4x (or even 3.5x) it used to be at? Either prices fall or wages go up

Can prices fall more? There is still a shortage of housing in most major geographies in the US. Inventory of existing homes is sparse. There is still demand from Millenials who are in the midst of household formation

That means wages need to go up. How much? If this measure were to go back to 4x, wages need to go up by 20-25%. In my wages post last week, I showed how the many unions are asking for & receiving gains more than that

This is going to be an interesting dynamic to watch play out. Views may need to reset

The second takes into account the mortgage cost and looks at another measure of affordability, that is collapsing and signaling much more difficult times ahead for the housing market.

Chart of the Day - affordability part two

Yesterday I took a look at the move in 10 year yields & showed how the multi-decade trend lower in yields might be changing. That has the potentially to ratchet lower the ratio of sales price to income back toward longer term averages

Today I want to look at a different measure of affordability, this time one put out by the Natl Assoc of Realtors. That composite index is in white and adds to the measure I used yesterday by including a mortgage component.

When the index is 100, a family earning the media income can afford a media sale price house using conventional fixed financing. You can see the index is not only below 100 now but at the lowest levels this century

You can also see that a decline in affordability led the other housing measures we use lower into the Great Fincl Crisis. A massive improvement in affordability led the housing measures in the decade after the housing crisis

Right now it is headed sharply lower yet not all of the other housing measures are following suit. One measure that is going lower is the existing home sales in purple. I spoke about the homeowners there that are 'trapped' with a low mortgage rate

Let's not feel sorry for them because while they can't move, they are locked into long term money at century low levels. They are non-plussed by this move higher in rates. Expect these families to be the ones doing lots of things to fix up their old houses in the next decade

New home sales have held up better as homebuilders are offering all kinds of incentives to make things more affordable. Communities are further out. Houses are smaller to bring down the avg price even if sales per sq ft is still high. Builders also offer shorter term teaser rates on mortgages

With strong demand due to Millenial household formation, this houses are selling. New home builders have a unique oppty in this mkt which is why Warren Buffet has bought stock in them even if their prices still near all-time highs

This demand is perhaps why the biggest data outlier still holds up. The blue line is the Natl Assc Realtor diffusion index. A reading above 50 means more builders view conditions as good than poor. Below is the opposite.

The latest reading came in right at 50 and is not shown here as the data only goes thru June which when the other measures go up to. With 30 year mortgages hitting the highest levels since 2000, we can expect the white line to keep moving lower

This will continue to weigh on housing which will weigh on the economy as well. This doesn't appear to be a 2005-2008 problem because that was an oversupply issue. This is a high demand but no affordability issue. Things slowing & prices needing to fall for different reasons

It is still something to keep your eye on because it will effect not just the broader mkt but each of your local communities as well

The one thing I believe that is holding the realtor survey of the housing market in place is the jobs market. I made this point repeatedly last year when the spike in mortgages was predicting a collapse in housing. My point is that it isn’t just the cost of a monthly payment that matters. It is also the ability to make that monthly payment given your job. If mortgage rates are zero, but you don’t have a job, you won’t buy a house. If mortgage rates are high, but you have a really good job, you can buy a house. I created a simple geometric average of mortgage rates and unemployment rate that I call Mort*Job. It is in blue and does a better job of tracking the NAHB housing market survey than mortgage rates alone. This move is not great for housing at all. But a still healthy job market insulates that … for now.

Lots of moving parts. There are many that want the Fed to give it the green light to buy the dip - in stocks or in bonds, depending on your market. The Fed is meeting with all global central bankers this week at Jackson Hole for the annual getaway. Recall last year, a very short speech by Jay Powell, telling the market the Fed had a lot more to do, caused a 17% sell-off:

There are no expectations of that type of move. However, I fear there are a lot of expectations that this will be the typical ‘non-event’. Benson at PiperSandler made that exact point as he analyzed history:

“The lauded symposium just doesn’t move markets, on average, as compared to run-of-the-mill FOMC meetings and, non-farm payrolls or ISM do. Still, the Chair could say something interesting. A few Jackson Hole speeches were of course very big deals. Bernanke made much of the venue in 2010 and 2012 ahead of QE2 and Operation Twist respectively. In fact, only two of 21 chair speeches coincided with daily changes in the ten-year US Treasury yield that exceeded a couple standard errors, given all trading days since August 24, 2000. Similarly, only twice have S&P 500 returns been outsized to the same degree, but last year happened to be one of those times.”

I also fear many others think central banks will be dovish. The theme this year is “Structural Shifts in the Global Economy”. There are parts of the global economy that are struggling. I have looked at Chinese economic data quite a bit of late. Emerging market central banks are rapidly reducing rates as inflation is no longer a fear, slowing economies are. Argentina is slowing so much it is about to devalue, collapse or both. As people say, when the US coughs, the rest of the world catches a cold. Could this lead to a dovish outcome? Perhaps. My sense is central bankers understand, as I do, that inflation is a mindset and not a number. One needs to get people to change their mind about what will happen going forward. Workers ask for higher wages not because last year had a high CPI, but there is a fear this will continue for the next 5 years. How do central bankers measure this anchoring? Inflation expectations. I include 4 measures here - that from the US Treasury Inflation Protected bond market (white), from the US swaps market measuring 5 year inflation 5 years forward (blue), the Fed’s preferred measure, the St. Louis Fed 5 year expectations in orange and the University of Michigan consumer inflation expectation in purple. Only the TIPS market is lower from a year ago. All are higher than pre-Covid. Collectively this may be reason Jay Powell might not be as dovish or as much of a non-event as the market thinks.

The US bond market is the most important market in the world. It has been in a bit of a state of chaos of late. Will this continue? My sense is the bond market vigilantes think so. I like the way vigilantes think typically. I am watching their lead. We are all trying to …

Stay Vigilant