K.I.S.S.

Not trying to overthink right now

With everything going on in the past week, I have been reading a ton of perspectives and listening to many webinars. I thought this point, raised by Tony P. of Goldman in his note to clients, was maybe the most humble but also the most important:

Very, very few people really know anything.

I couldn’t have said it better myself. Right now there are a lot of “experts”. Even worse, if you spend all day on X.com trying to sort through things, you are being hit with 3x the amount of propaganda as usual. You have likely the China/Russia bloc saying how Iran is winning the war and the US is running out of ammo, and the MAGA crowd saying that this will be over in days. How do we know what to do?

For me, I try to keep it simple. What is the simplest thing to think? Oil prices are higher. Oil prices are likely to stay a bit higher than normal for now. You want to be long the oil winners (energy stocks, petro currencies) and be short or sell the oil losers (Asia, cyclicals).

This is difficult because the oil losers had been ripping higher. However, as John Maynard Keynes says, “when the facts change, I change my mind. What do you do, sir?”

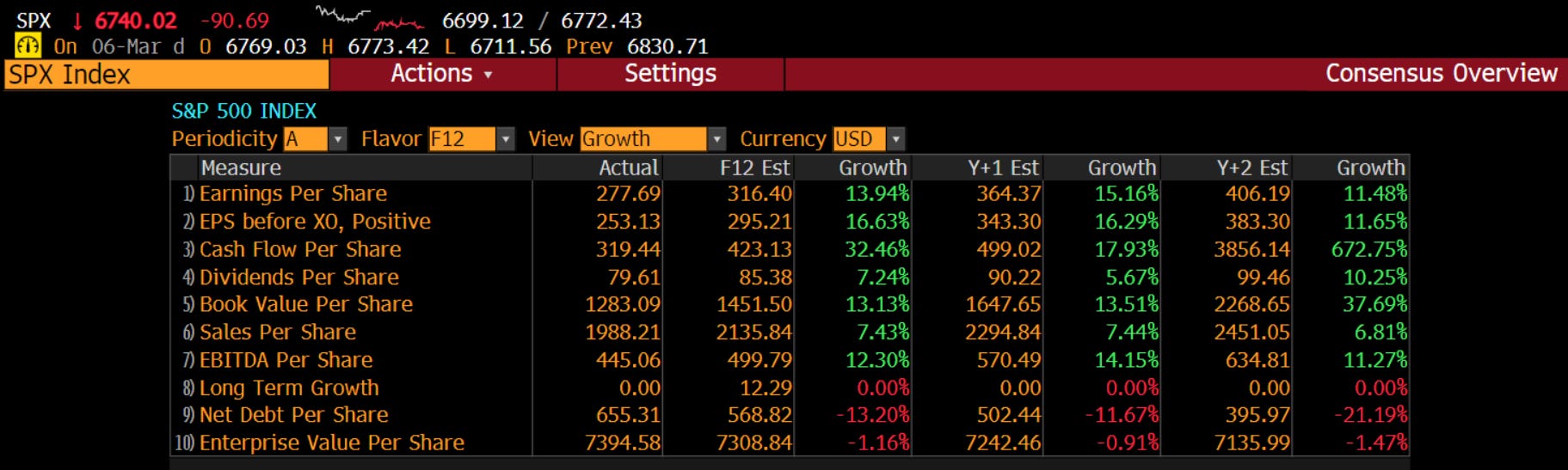

Oil prices have an impact on more than just the oil importers. There is a link between oil prices and the multiples we pay on stocks through the inflation channel. The current move higher in medium term (3-month futures) suggests the SPX forward P/E is heading lower:

In addition, for those that follow commodities, you know that futures that go into backwardation predict higher futures prices. This is the 2-month vs. 9-month curve vs. futures prices. Higher oil prices are predicted.

Layer in the problems we already had in the credit market, which also predicts forward P/E through the liquidity and investor sentiment channel, and forward P/E looks set to fall to the 19.5-20x area pretty soon.

If we put 19.5-20x on the expected eps the next 12 months of 316, we get an SPX of 6150-6300. Now, what if earnings come down to only 290-300, still growth just not the 14% growth as expected? We are quickly into the 5900-6000 area.

What is the catalyst? Volatility itself. As I discussed with students this week, risk parity strategies use volatility targeting. This is the way they measure how much leverage to take and therefore how much to own of each asset class. When implied volatility rises, the amount risk parity invests in equities comes down mechanically. What causes volatility to go higher? Tighter liquidity as seen in credit spreads. This is the same measure of credit spreads vs. implied volatility, pointing to higher vols:

This is the measure of implied volatility (inverted) overlaid with the equity exposure of risk parity, which has yet to fall very much. This is very real (hundreds of billions) of selling pressure.

Technically, the SPX looks like it is breaking through the ichimoku cloud. With this selling pressure, the lagging span will fall. The target range on the Fibonacci retracement of the move from the April low to the October high is 5900-6200, the same area we can get to by looking at P/E and eps.

This suggests to me that risk management needs to take precedence to being the hero.

As Tony P said, no one knows very much about what will happen. I am not trying to predict what will happen. I am just trying to look at the ramifications of what has already happened.

K.I.S.S.

Stay Vigilant

Short, simple and to the point. Another great analysis in this interesting times.

Oil has stabilised, vol is lower so your risk parity guys have come into buy equities today - great note Rich