My personal rules of investing

With the recession vs. soft-landing debate still lingering, I take a step back and look at my personal rules for what I think has made me a better investor

As I continue to watch, and participate, in the debate about the path forward for the economy and financial markets in 2023 and beyond, it seems right now few viewpoints are going to change.

Thus, I thought a little introspection might be more helpful. I want to tell you about the rules that I have found have been very beneficial for me. Perhaps, hopefully, they will also be beneficial for you. I will try to give examples of each.

Rule #1: Stay humble

This is the hardest thing to do. This is particularly hard to do when you have the right view and are being rewarded for it. However, the market has a way of humbling all of us. The longer you have been investing or trading, the more you have been humbled. The only market veterans that are boastful and overly confident are the ones that are trying to sell you something. Make sure you understand that. As we would say on the desk, everyone is talking their own book (portfolio). You just need to appreciate that and take it for what it is.

My three-part process is an attempt to stay humble. In that process I look at more than 60 different variables and time-series. Going through the process takes a lot of time and can seem arduous. However, it also reminds me that there is a lot of information and a lot of different approaches that people take to make money. I am only scratching the surface with the 60 variables I employ. There are hundreds more. There are different approaches - fundamental or technical, time horizons - day traders or investors, and markets - different asset classes, public or private. People can and do make money in all of these markets and approaches. We can learn something from all of them. We should.

I am fortunate enough to have spent meaningful time working in Asia, Europe and the US, investing via FX, EMFX, EM debt, equity long/short, global macro, tail-risk funds, and derivatives portfolios. I have learned something and adjusted my process with each.

From that, I try to stay humble and have perspective. This week, I wrote about perspective on Linked In:

“…when I see risks flaring on the horizon, I try to point them out. I try to help people anticipate what can go right or wrong, so they do not get caught up in the euphoria or the panic.

Right now, is one of those yellow warning signals. Last week we got the ISM data. Not only the headline data which sunk to 47.4, well below the 50 level of expansion or contraction, but also the new orders & inventories.

The ratio of new orders to inventories in blue leads the ISM itself, which is coincident with the SPX. Both lead the GDP & non-farm numbers. They tell us where we are going. Not where we have been. As you can see, it isn't good news.

In fact, the new orders to inventories suggest more downside in ISM to the 45 level. Every time we hit 45, we have a recession. Not a soft landing. A recession. Maybe this time will be different. I doubt it.

You can see the ISM also leads the percent of companies positively surprising on earnings. As the economy slows, earnings begin to slow more than anticipated. You can see this in orange. It has much further to go.

It also leads credit spreads. These investors don't care about growth as much as safety. However, when growth goes negative, safety is called into question. This process is only beginning. When spreads widen, it becomes self-reinforcing.

We are still early in this process. It does not mean it has to be a 2008 crash. However, it does mean it could be a 2000-2003 protracted downturn. Recessions & wringing out of excesses takes time. We are still early on.

Just be careful in how you are investing so you are not forced into bad choices later on. Investing is meant to provide financial freedom which means you don't think about money, you think about what matters.”

Rule #2: Learn from your losses

Education as always been a part of my perspective on financial markets. My first role during and after undergrad was with a firm named O’Connor & Associates. We like to say, it was Google before Google. OCA brought together the best and the brightest from across the country and around the world. The goal was to make money in the various nascent options markets that were developing.

A core philosophy of OCA was education. After all, it was hiring finance majors and engineers, geology majors and lawyers, market veterans and newbies. It needed to teach everyone a standardized firm approach, and firm culture, that would lead to success. Many other firms have tried to replicate this, but I know of few that have been as successful.

The education was not just in the classroom. The education also took place at the end of every day as we sat around and discussed what went right and what went wrong. As a rookie, I listened to the senior traders and portfolio managers talk. What I realized is that we all learned more from our losses than our gains. We learned more from our losses than our victories. We learned about our biases that prevent successful decision-making. We learned about being too rash.

A great example from this firm was our losses in 1991 from the devaluation of the Finnish markha. I traded FX options at the time and we were about to go into the European Exchange Rate meltdown in 1992-1993, we just didn’t know it yet. However, the firm took a big loss one weekend on this devaluation, being short a lot of put options that ended up in the money. From this experience, we learned two things: 1. always cover your tail-risk - spending a tick to cover a wing is better than losing millions; 2. things were about to drastically change in Europe

OCA proceeded to learn more about and then bet against all of the weak currencies in Europe. This mindset permeated all aspects of the FX business. When it was all said and done, OCA was a huge winner from the breaking apart of the Exchange Rate Mechanism. However, in order to get to that point, it took a loss.

One of my most popular posts this year was called “I was wrong”. This wasn’t a mea culpa to make people feel sorry for me. This was an admission that being early is the same as being wrong. Sometimes we are more wrong than that.

I thought this year the market would focus on an economy that would slip into recession this year (I thought by summer, maybe it won’t be until later) which would drag down earnings. As multiples were already above average, the decline in earnings should lead to lower stocks.

Fast forward six weeks and markets are higher. I was wrong. As I wrote in a comment, I am glad I expressed my view by being in cash and being long puts and not by being short. However, the opportunity cost of missing out on high single digit or low double-digit gains in the market is very real. This is how FOMO kicks in.

When I am wrong, I always want to look at who is on the other side and who is right. These are the winning strategies this year:

Volatility, leverage and short-interest are near the top of the pack. Before this past week, they were at the top of the pack. Near the bottom are earnings revisions which means firms with positive earnings revisions are losing relative to those with negative earnings revisions.

I saw on CNBC I believe a story about how active managers are lagging the market. Do you think, do you want, an active manager that tells you: “I am going to invest in high volatility, high leverage, highly shorted stocks with negative earnings revisions.”

Of course not. However, that is what is winning. So, I am wrong, right now. I am losing some premium and some opportunity. I learn once again that sentiment and positioning matter the most in the near term. This is actually part of my process, and I wrote about it on Substack a few weeks ago. Fundamental investors are bearish, technical traders are bullish, something has to give. The hard part of investing is that even when you observe the bifurcation, knowing how it will play out is difficult. The reason I chose to spend some of my money market interest on premium, instead of fighting more aggressively, is knowing this technical bull call. At least I have learned that from my losses.

Rule #3: Stay in control with your emotions and dry powder

Sometimes the best position is no position. Sometimes it is better to be in cash and let the uncertainty play out. I learned this early from a mentor of mine. I was trying to convince him of an opportunity where we could make 50% but the risk was we could lose 20%. He asked me, what if we wait until the catalyst play out, how does that change the dynamic? I told him that assuming the asset would move on the news, we could still make 20-25% and once the news was out, our risk was probably limited to 3-5%. He told me - then we will wait. I said “what are you talking about? We are going to possibly miss 50%” to which he replied “yes, but after it is de-risked, I will be more comfortable to put 5x the amount of capital into the idea and the dollar amount of gain will be much higher”.

Having no position can feel meager. It can feel like you aren’t doing your job. However, if there are not favorable odds on your side, if you do not have a margin of safety, why take unnecessary risks? Why not wait for more clarity and go for it in bigger size?

I wrote about it this week on Linked In:

Chart of the Day - would you rather. "Would You Rather" is a fun ice-breaker game that you can play with anyone, anywhere. All you need is at least two players and a creative mind to come up with interesting scenarios and questions

Th goal is to try & ask a series of different types of questions to find out a lot about the other person or people. For instance, you can ask a question with two good options, or ask a question where there is a dilemma posed

That is the game that mkt participants play each & every day in the mkt. The mkt asks us as investors 'would you rather': buy or sell, choose asset A or B, choose stock A or B. Sometimes it asks the entire group, sometimes it ask just a certain portion of the group.

When trying to discern how to answer that mkt question, it is important to try & normalize the opportunity set. For instance, if the mkt asks - would you rather own Treasuries, corporate credit or stocks, how do you answer?

Sometimes it is clear that we are in troubled times & there is a preference for safety. Sometimes it is clear that risk-taking has a big tailwind & there is a quest for upside. However, the best would you rather questions come when it isn't clear.

Like now. Of course I say that knowing that half the mkt feels it is very clear that we should seek safety & the other half feels it is clear we should seek upside. When I speak to my various classes I can sense this even among my students.

How then do we look to normalize these opportunities? Classically, we would suggest that being lower on the capitalization stack means there is more risk. In order to take more risk, investors should be compensated. Are they?

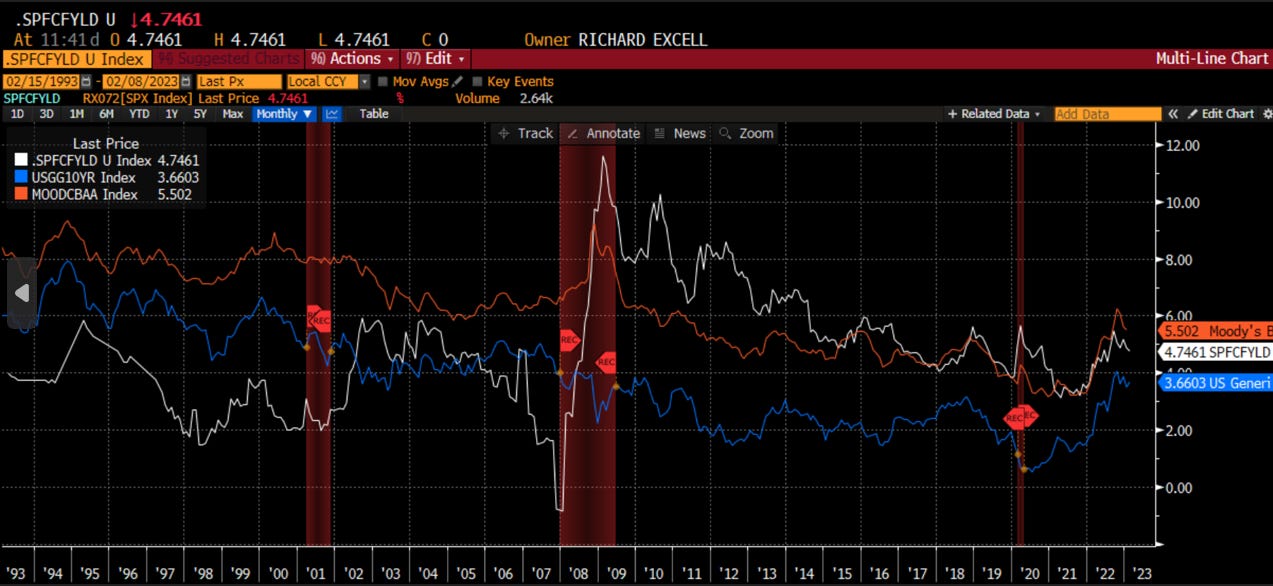

The chart today shows three lines: Treasury yields in blue, Baa yields in orange, and SPX fcf yields in white. I use fcf because the earnings yield can & is obfuscated by adjusted eps & stock-based comp.

We can see when the FCF yield is well below the other two, when not only are you not compensated for risk but you are effectively paying to take it, bad things happen. Think tech bubble & GFC.

When fcf yield gets to be too far of a spread above Treasuries, it is a good time to take risk. Look at the almost 10% difference in early 2009. This would be the margin of safety Ben Graham refers to.

A lot of other times it isn't that blatantly clear. One can look & see that when FCF yield moves below Baa yields, it is a better time to be in credit than stocks. Why shouldn't one get compensated to take more risk in stocks?

Stocks do best when the entry level fcf yield is above both Baa & Treasuries. The returns are much less certain when it is between. When it is below both watch out.

Right now it is below Baa & above Treasuries but the spread to Treasuries is the tightest since 2005. This makes the would you rather game almost seem more like truth or dare.

So I ask you - would you rather?”

I would add to this post something I took from a friend of mine, EJ at Cantor. He was also speaking about a margin of safety or lack thereof. He was showing how the spread between the yield on cash and the yield on stocks is the lowest since the GFC. Are you being compensated to take risk? Maybe it is better to keep your powder dry.

Rule #4: Maintain an intellectual curiosity and stay thirsty for knowledge

I will often have people message me and ask me which degree they should get or which certification they should pursue in order to understand markets better. This is a very difficult question to answer. After all, it depends on your interests and your skills. It depends on where you focus and depends on your experience.

However, in spite of all of this, I do answer that one should focus on lifelong learning. I told you about the education I got from my first job. I told you about what I have learned in different jobs and cultures. I have also then pursued a CFA charter, MBA degree, CMT charter and ESG certification. I am now working on more programming and big data analytics skills. I just think one should always try to keep learning. Why? For one, it improves your skills and makes you more employable if not successful. For another, it is rewarding. Maybe most importantly is that everyone else in the market is trying to get better, so if you don’t, you will fall behind.

No one degree or certification has informed a majority of my process. I take parts of all of it in each piece. I think this is a competitive advantage personally. Along those lines, I wrote a bit on Linked In this week about what we can learn from other markets as well:

“Chart of the Day - gimme some credit. I am sure there are a lot of people feeling that have gotten a lot wrong in the early part of the year. To not have participated in a 15% rally in the NDX can doom one's year if not their career.

They probably would love to get some credit for something, for some of their calls. We all need that positive reinforcement after all.

When I think of credit, I think of credit markets. I have always learned/known that credit leads equities. Those focused on the return OF capital vs. the return ON capital are going to be more critical.

In his podcast with me, Barry C. Knapp mentioned to me that credit does lead equities except at major inflection points. This is when we can see the lower quality equity names outperform earlier.

In fact, we have seen leverage, short interest & volatility as the top performing factors this year. This might seem to imply credit will then follow along.

In my Substack this week I pointed out how the Moody's Corp Baa credit index has disconnected from the ISM readings suggesting that we have perhaps seen the low.

However, I am not so sure we are out of the woods yet. The chart today shows the relationship between High Yield vs Inv Grade and compares to Energy vs. SPX as well as oil.

What we might infer from the chart is that the outperformance of the lower quality credit all of last year, which was seen as a sign of strength, might actually be do simply because of energy.

As we can see, the outperformance of HY to IG coincides extremely nicely to the outperformance of Energy to SPX. Leading them both? The price of oil which was lower into the depths of Covid but then has run quite nicely.

Energy companies to their credit (pun intended) have shown a considerable amount of capital discipline which should make both bond holders & equity holders quite pleased. This has shown up in performance.

The times may be a-changin' tho. Oil price is back to where it was in late 2021 & we are now realizing that Russian supply is still getting to mkt. Biden seems to be playing chicken with the SPR creating even more uncertainty.

Oil has broken lower on the daily charts & is headed to support on the weekly. If prices break down, how long can energy companies show the discipline. Will credit & equity investors get impatient?

The cost of goods & the cost of capital underpin all of what we do in forecasting the economy. At least one of these may not be so favorable going forward.”

Rule #5: Help others

I remember working with some Aussies back in Singapore. We were talking about a particular customer who took great pride in ‘running us over’. He would ask several banks for an options quote in large size, and then trade with one who would then have no chance to cover any of the risk because everyone knew the trade and where it was done. You may ask why we bothered, but it was the decision of people higher up the food chain than us. Anyone, one of the Aussies said “don’t worry, karma is a boomerang.”

His point was essentially what goes around, comes around. If we treat others well, people will treat us well, if we don’t treat people well, it will eventually catch up to us. I have no idea what ever happened to that customer, so I don’t know if that negative karma boomeranged. However, I do know that in trying to prepare not to get run over, I got a lot better in my investment process and it has helped me through the years. So, at least the positive side of the karma boomeranged.

That is one of the many reasons I try to put out the content I do. I want to “demystifinance” and make the markets more approachable. I am just looking for more of that good karma to boomerang.

I would encourage you to do the same. Most importantly, I would encourage you to not engage in the Twitter bashing etc. that occurs. Rise above it.

I tried to rise above this week as I was disagreeing with someone on what will happen to multiples in this cycle. He was adamant multiples will rise as earnings fall. I took the other side and he seemed to get offended. He said, make your point and if you argue I will block you. Again, I am not trying to argue. I am trying to share the information I have. I am a believer in the Socratic debate method - if we have a debate, and I feel I won, I should have more confidence going forward. If I lose, I know I need to go back and do more work. This can’t happen unless we are trying to help others though.

Anyway, this was the offensive Tweet:

“There is a lot of talk of eps ranges and P/Es in the cycle. On the left is the consensus expectation for eps at $223. I have seen forecasts as low as 140 but I will put 180 as the low. On the right you see the range of P/E this century. We can say the 1 s.d. range is 14.5-20.5 but we can also see the high P/Es are achieved when rates are falling and not rising. If we take the extremes we get 20.5*220 or 4500 on the upside or 14.5*180 or 2600 on the downside. If we narrow the P/E range on the same range of eps we are looking at a 3200-4200 range for this year. To get a breakout from here you need BOTH eps to not fall (consensus sees flat) AND multiples to expand from above average levels even in a rising rate environment. I think Benjamin Graham used to ask about the margin of safety. I will leave you to draw conclusions.”

Rule #6: Stay unbiased

There are many biases that can affect an investment process. They are categorized as either cognitive errors or emotional biases. The former are basically mistakes in calculating the real probability of something occurring. These are relatively easily fixed. The latter group are emotional problems. Money is emotional. That is human nature. The more we can try and stay objective, the more successful we will be. I have tried to incorporate many things into my process to take these various biases out of the process. I will list them here for you. I would encourage you to do the same. I highlighted the ones I have seen the most.

Cognitive errors:

•Conservatism – revise views too little when given new evidence

•Confirmation – look for or pay attention only to information that supports your view

•Representativeness – similarity of events informs the odds of an outcome

•Illusion of control – overestimate one’s ability to manage outcomes

•Hindsight – people perceive past events as having been more predictable

•Anchoring – decision is influenced by a reference point

•Mental accounting – investors categorize outcomes

•Framing – manner in which data is presented can affect decision-making

•Availability – mental shortcut that relies on easiest info to find

Emotional biases:

•Loss-aversion – people hate losses more than enjoy gains

•Overconfidence – subjective confidence > objective ability

•Self-control – people do no act in their long-term best interests

•Status quo – a preference for the current state of affairs

•Endowment – prefer to retain an object owned than acquire at same price

•Regret-aversion – decision is affected by desire to avoid regret

Rule #7: Try to understand both sides of a debate

I remember a lot of things from my time on an exchange floor. It was like the investment version of that book “All I need to know I learned in kindergarten”. I say that with fondness in my heart for the combination of juvenile fun but also intellectual power that I saw on display every day.

One thing that has stuck with me is: Bulls make money, bears make money, but pigs get slaughtered. It sounds a little simplistic, but there is a lot of truth in this. Whether the market is trending up or down, there will be opportunities for both bulls and bears to make money. Those traders or investors who are greedy and overstay their welcome, are most likely to end up losing the most.

In my quest to understand both sides of the debate right now, the recession vs. soft-landing, the Fed will be higher for longer vs. the Fed will cut, I wrote this on Linked In this week:

“Chart of the Day - when doves cry.

"How could you just leave me standing Alone in a world so cold?

Maybe I'm just too demanding Maybe I'm just like my father, too bold Maybe you're just like my mother She's never satisfied

Why do we scream at each other? This is what it sounds like

When doves cry" - Prince

This song popped into my head yesterday when I saw the market reaction to Jay Powell comments.. Much like the FOMC press conference, I did not hear the dovishness that many others heard.

In fact, what I heard actually makes me more nervous as the chart today will show you. I heard JayPo say there will definitely be 25 bps in May. I heard higher for longer as well.

The mkt heard that inflation was expected to soften. The mkt is still pricing in rate cuts to begin later this year and continue into 2024. I still don't see it.

As I commented on another's LI post yesterday "when the Fed feared deflation, it stayed lower for longer than anyone though possible. Now it fears a reacceleration of inflation. I think it will stay higher for longer than any of us think is possible"

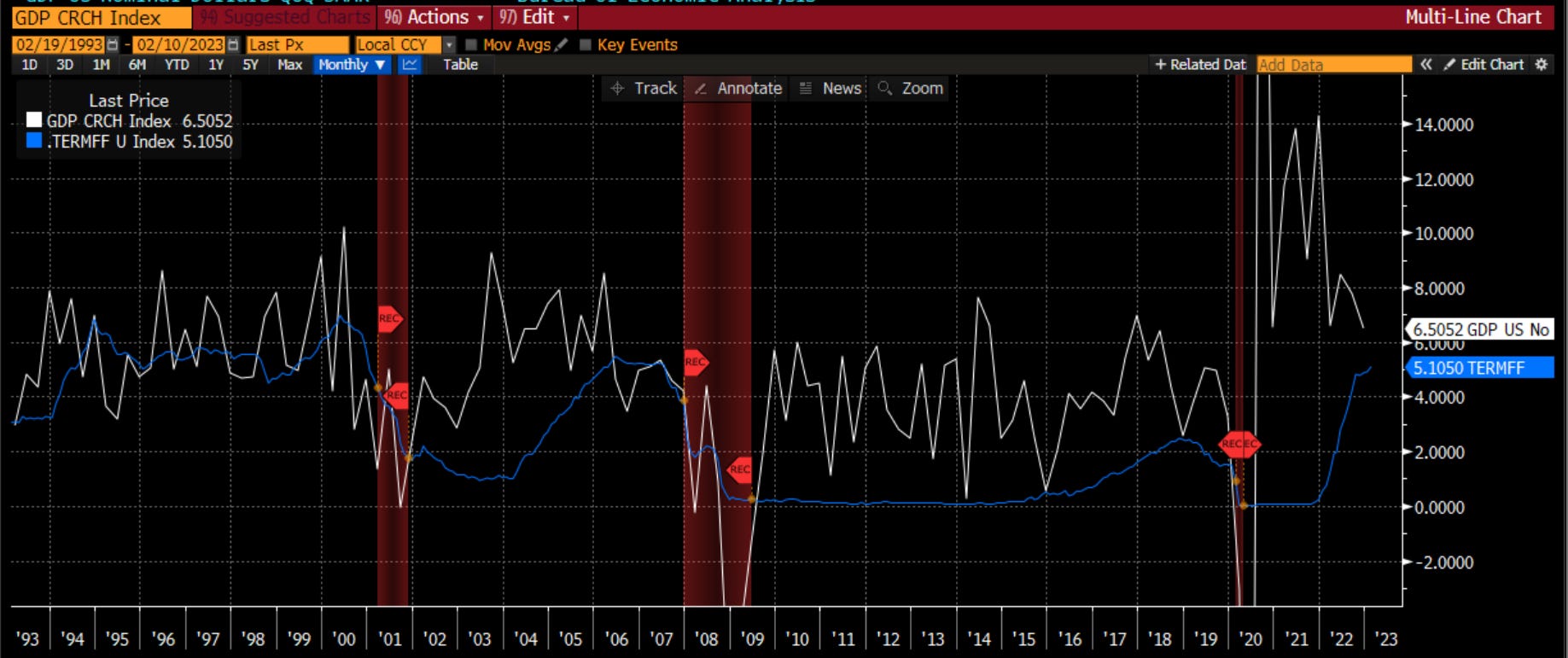

Let's just look at today's chart. It shows the terminal Fed Funds future - where the mkt expects the Fed to peak - versus nominal GDP.

Perhaps you see the same pattern as I. Whenever Fed funds moves above nominal GDP, we have a recession (in red). Yes, there was that period in the mid 90s where we didn't so it isn't perfect, however, its been pretty clear otherwise.

Let's say the FOMC stops at 5.25% where he says now. Let's say we get the soft landing that JayPo forecasts per his presser - real GDP around 1% but not negative and inflation falling to 3%, still above the 2% target.

That sounds like a 5.25% Fed Funds vs a 4% nominal GDP. That sounds like most people's base case forecast right now. That sounds like we are on the brink of recession if history is any guide.

Again, perhaps this is the mid 90s. That was a period where strength in Asian economies was leading to a global savings glut that supported US assets and helped us avoid a recession. It also led to a bubble.

Another period not shown on here is 1967. In that period there was no recession but the Fed stopped, inflation reaccelerated, the Fed restarted and we got the recession in 1969.

But like Prince asks us 'why do we scream at each other?" Can bulls & bears alike look at the same information and come to a different conclusion? Is any of the info I said today debatable?

The bulls see the Fed finished & a new bull mkt. The Fed has finished before & it hasn't been a new bull mkt. The bears see a recession, earnings decline & lower stocks. With a record number forecasting recession, perhaps it is priced in.

Maybe the reality will be that we are both wrong & the mkt just goes nowhere. After all, markets can go sideways. Markets tend to find the way to hurt the most people.”

Rule #8: You will be rewarded (eventually) if you are beat up for your ideas by consensus

I leave you with the last rule. This is particularly true if you engage on social media. There will be times when people will beat you up, where you will get Twitter-bashed, maybe even blocked. Not because of how you are reacting, but simply for your views. As Abe Lincoln told us “You can please some of the people all of the time, all of the people some of the time, but not all of the people all of the time.”

It is still healthy to engage, tactfully, and try to understand both sides. The best positions, the highest rewards, can come when you realize that you are onto an idea, and the overwhelming consensus is on the other side of the debate. It will be painful to take a beating on social media, but it can be worth it to your bottom line.

Where might this be the case right now? The soft-landing view which I think is epitomized by the pricing of Fed policy at the end of 2023 and 2024. The market still is strongly of the view that the Fed will cut rates after pausing. It is not because of a recession, though, because otherwise the Fed Funds rate would go below neutral. It is based on a soft-landing view. My hunch is the FOMC is going to actively get these rate cuts out of the curve in the coming weeks. What does that mean for real yields? What does that mean for equity multiples? What does that mean for commodity futures curves? This is all up for debate, but understand where consensus is:

I hope you enjoyed my rules for investing. Have a good week in the markets and …

Stay Vigilant

Great investing life lessons in this post. Thanks for sharing them. #4 and #6 hit home the most for me...staying curious, continuously seeking knowledge and information and considering all POVs on an idea/thesis.

Unfortunately, in today's social media driven investment world, many investors forget these timeless values.

Perhaps I can suggest one more lesson to add to your list:

We are competing with ourselves when we invest.

Really enjoyed the embedding of your early career. And some events specifically that weren't so clear how they were going to play out when they did. A lot of information we get is a "history favors the victors" kinda thing.

Like seeing how you think about different environments. I wrote down each of the biases for future reference. And how you apply your investment framework to different case studies of present and past.