Plot twist

Post the FOMC meeting, and given the banking problems, we are moving from a rate tightening cycle to a credit tightening cycle

I hope you enjoyed the Macro Matters podcast for the CFA Society Chicago that I posted on Thursday. Monique, Tony and I wanted to cover the events of the day in real-time because we are at such a critical juncture for the economy.

Digging into the FOMC press conference a little more, I found these comments from Chairman Powell to be the most important in my opinion:

Source: Yahoo Finance

This is exactly the topic I was speaking to many friends in the market about on Thursday and Friday. The FOMC is passing the torch to the banks to do the heavy lifting on slowing the economy and bringing down inflation.

One interpretation, which many in the market took, is that the Fed is pausing and it is time to buy riskier assets again. I have to say that is not the interpretation that I would take. In fact, if you read my LinkedIn this week, you would see that I have highlighted dozens of reasons why I think a recession is starting sooner than later, and why this is important for riskier assets which typically sell-off as the recession starts.

One snippet came from an FOMC press conference from 12 months ago, when the Fed first started to hike rates:

"Frankly, there's good research by staff in the Federal Reserve system, that really says to look at the short - the first 18 months - of the yield curve. That's really what has 100% explanatory power of the yield curve. It makes sense. Because if it's inverted, that means that the Fed's going to cut, which means the economy is weak." - Fed Chair Powell, March 21, 2022

Looking at that indicator, which I call the JPOW Recession Indicator, you can see that it has down a pretty good job that last 40 years in predicting a recession. When the forward TBills are more than 50 basis points below the current 3-month TBill, a recession occurs. The loan ‘exception’, which was really a double dip, happened in 1997. This was a period when we had the Asian Financial Crisis beginning and the market anticipated the FOMC cutting rates. It did, because of uncertain effects from abroad, which served to boost the US economy and market again, leading to more severe hiking cycle that ultimately brought the economy and market lower in 2000.

(A hat tip to Garfield Reynolds from Bloomberg for the news story today that highlights this indicator and the quote from JayPo.)

You can see from the DOT plots of FOMC members and the Fed Funds Futures that the market is far more dovish than the FOMC. Fed members see rates going up one more time and then staying firm the rest of 2023 before cuts happen. The market sees 75 bps of cuts happening this year and another 150 bps of cuts happening next year. The market clearly sees something the Fed doesn’t or is at least unwilling to admit to.

I do think the Fed does see this possibility on the horizon but does not want to be accused of shouting ‘Fire!’ in a crowded theater by mentioning it. Thus, in true Fed-speak, we see the comment above: “The extent of these effects is uncertain” and “Such a tightening in financial conditions would work in the same direction as rate tightening”

The Fed knows banks are going to tighten standards. We discussed this last week. I think this is important enough that I want to highlight it again. In our fractionalized banking system, a bank’s loans + investments = deposits + bank capital. Typically for every $1 of deposit taken in, about $10 of loans are made. Right now, banks are struggling to retain deposits. That is the big problem right now. It is particularly acute for small banks. About half a trillion has already left big banks.

The first wave of money left banks for money market accounts in order to pick up about 4% of yield. I did this, and told all of my kids and family to do it as well. Why sit in a bank for 0% when you can get 4%+ in a money market. Don’t get me wrong, you keep 6 months of expenses in your bank account for the liquidity and security. Anything under 250k is guaranteed by the government. However, the money you do not need for expenses might as well sit in a money market.

Post the SVB fiasco, the next wave of move into money markets is an attempt to get out of banks. This from MarketWatch:

“Assets held by money-market mutual funds swelled to a record high $5.4 trillion last week as inflows hit the fastest pace since the start of the COVID-19 pandemic following the collapse of Silicon Valley Bank.”

No go back to the fractionalized banking equation. In order to make a loan, in fact $10 of loans, banks need $1 of deposits. However, deposits are going the other way. Do you think banks will be making more loans or fewer loans for the next several months?

As I mentioned last week, before the second wave even started, when we were first seeing money move to chase higher yields, banks were already tightening standards:

For loans to small businesses, it is even harder to get a loan than for large businesses. This hurts the outlook and optimism for small businesses. I have inverted the small business optimism index, or NFIB Outlook here, and compared to the percent of banks tightening standards. You can see there is a really good fit to this data with the immediate post GFC period the only period when loans were available but businesses weren’t optimistic. However, as standards will get tighter, we should expect optimism to fall.

If businesses are not optimistic, do you think they will hire more people? There has been a disconnect between the outlook and employment this year. I expect these two series will recouple with employment falling. We already see that in the tech sector.

Small businesses are the engine of the economy. If small businesses are expected to ratchet lower, I would expect ISM and GDP to do so as well.

I will show you again my favorite ISM chart courtesy of Credit Suisse (RIP). It plots four regimes: ISM above or below 50 and rising or falling. The ONLY period in which SPX returns are negative on average are when the ISM is below 50 and falling. Right now the ISM is 47.7 and is expected to fall further. You tell me what to expect in the SPX.

However, it isn’t the deposit flight that is the only problem. You see, right now this banking ‘crisis’ is not that big of a problem. Well, yes, it is existential potentially for some small and mid-sized banks. However, as customers move money to either bigger banks or money markets, the money is not lost. It can still circulate in the economy. Banks are losing deposits and facing a liquidity crisis. Banks have not yet started to lose any money on loans. In fact, the average bank has less than 1% of their loans market as non-performing right now.

That may be set to change. Investors are increasingly getting concerned with the risks in commercial real estate. CRE is a vast sector that includes everything from office buildings to healthcare facilities, multi-family buildings, hotels, data centers and even distribution centers. There is no meaningful concern yet in most of this sector with the exception of office buildings.

Here I show the charts of SL Green and Vornado, two major players in the office building space, compared to the full REIT Index. You can see REITs broadly are pretty flat since the start of 2020, however, the office building players are at only 20% of their equity value from the beginning of that year.

I read about the risks of CRE in the Wall Street this weekend. This may be the next shoe to drop for banks.

From the Wall Street Journal:

You can see we have a negative combination of vacancy rates rising to the highest levels in more than a decade at the same time a large amount of newly built office space is coming on line.

This is only part of the problem for these players. You can also see the previous growth of office space happened from 2013-2018. CRE loans are typically about 10 years. This means that starting this year and for the next 5 years, CRE loans are coming due. You know who holds most of those loans? Especially for small and mid-sized players? You guessed it, banks. You know who doesn’t want to rollover or make new loans right now? You guessed it, banks.

Per US News & World Report:

“For banks with assets between $1 billion to $10 billion, CRE loans comprised about 33% of the total held on their books, according to estimates by ratings agency Fitch. At the end of last year, CRE only made up about 6% of loans held by larger banks that had total assets of more than $250 billion, it said.

Goldman Sachs economists estimate the combined share of small and mid-sized banks, including lenders with less than $250 billion in assets, is 80% of the overall stock of commercial mortgage loans, it said in a note.

Both Goldman and Fitch did not specify which small lenders were most vulnerable.

Julie Solar, a credit officer at Fitch Ratings, said the office sector faces asset quality deterioration, putting smaller banks at risk due their relatively larger exposure as a percentage of their assets.

"Banks will be primarily exposed to CRE through bank loans on the balance sheet," she said. The total exposure of the U.S. banking system to CRE loans was $2.5 trillion at the end of December, Fitch said.”

About $500 million of these loans come due each year for the next 5 years. Of this $500 million in CRE loans coming due each year, at least 30% is thought to be office buildings.

More from the same USN&WR article:

“More cautious underwriting will probably lead to a further slowdown in real estate markets, Wells Fargo & Co analysts wrote, citing Federal Reserve data that showed tightening lending standards for CRE in the first quarter.

CRE borrowers are grappling with higher costs for refinancing and hedging at a time where it's also getting more expensive to pay back their debts, said Viswanathan at Goldman.

Declining occupancy rates will probably force office landlords to cut rents for tenants who are also seeking less space as they negotiate new leases, he said.

Morgan Stanley expressed a more bleak outlook for CRE lenders this week.

"Don't roll the riskiest loans when they come due," Morgan Stanley analysts led by Betsy Graseck wrote in a note. "Banks should tread carefully as they can be left with the keys" of properties they don't want.

Big cities will bear the brunt of the CRE woes.”

Back to the WSJ:

We don’t need a canary in the coal mine. We already have one. Brookfield and Blackstone’s BREIT have already had problems and suspended withdrawals from some of their funds. Presumably it was due to the illiquidity of these funds that the firms needed to slow the outflow. However, I think investors in them know the risks.

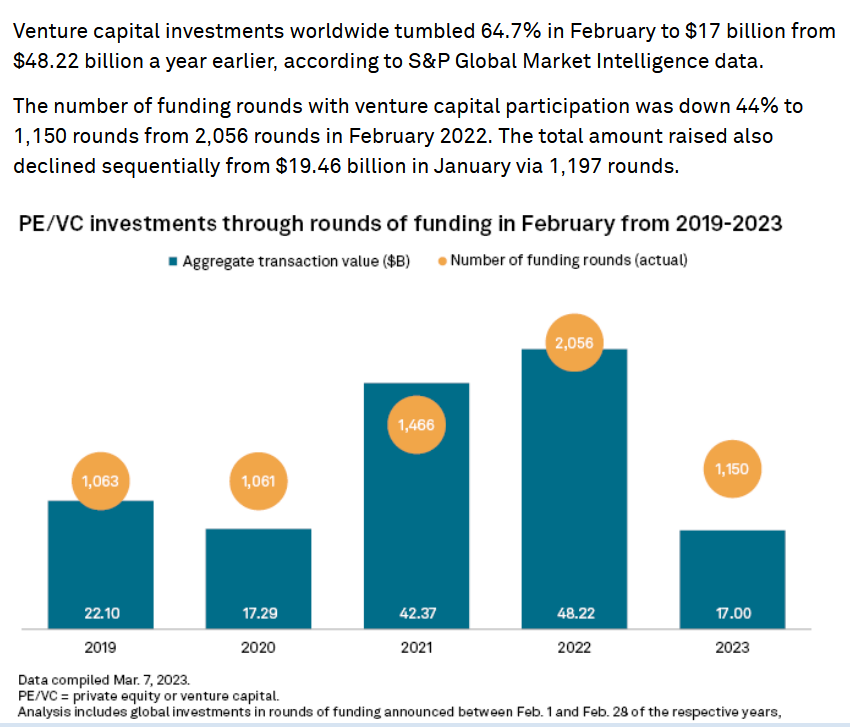

You think that is all? Au contraire, mon frer. Let’s go back to Silicon Valley Bank. Why do you think it was the largest, most successful and most well-known bank in the Valley? A major reason is that 50% of SVB loans were loans on capital calls for venture firms. What does this mean?

You see VC firms are measured based on the internal rate of return of the money they draw down from investors. When a VC raises money from pensions etc, they do not ask for it all up front. Otherwise, it sits in cash for a while and hurts returns. This makes them look bad. Instead, they tell the endowment or pension, we will tell you, with some months’ notice, when we need the money. You keep it for now. This improves the IRR because it doesn’t have the cash drag. You think mutual funds might like this arrangement?

Then SVB came in and said, we can do it one better. Not only do you not need to draw it until you need it, but we will loan you money against this commitment, and you can delay the draw even more. This will really help your IRR and help you attract more assets. You can see why SVB was so popular and critical.

It’s a great idea. Until …

Per S&P Capital IQ:

Investments were tumbling and VC firms needed the cash. In fact they needed the cash and went to SVB which didn’t have the liquidity as it was tied up in Treasuries. So SVB borrowed the money from the Federal Home Loan Bank of San Francisco. You think regulators shouldn’t have seen a yellow flag at this point? From the WSJ:

So now VC firms will still have those capital commitments but will be hesitant to draw too early for fear of hurting returns. However, if they do not draw, those endowments and pensions may get leery and want to back out. The companies VS firms have invested in will begin to struggle and need more cash too. This does not spell a particularly bullish story for Silicon Valley near term. What sectors are most likely to be affected? Again, per S&P Cap IQ:

We have already seen the lay-offs at the mega tech firms. Many of the smaller firms had absorbed this talent. However, those firms will more and more be starved of capital going forward. I look for more risk in TMT, both private and public.

This all takes me to a favorite of mine from grad school. I have used this in my career and my colleagues always roll their eyes as they think ‘how can this old thing work?’ I use it in my portfolio management class in helping the students how to build a model to forecast the economy. The logic and intuition are still robust.

The quantity theory of money holds that the price of goods and services is directly linked to an economy's money supply. The Renaissance astronomer and mathematician Nicolaus Copernicus formulated the idea in the 1500s. American economists Milton Friedman and Anna Schwartz revitalized it in the mid-20th century. Milton was at U of C where I went to grad school. You don’t have to be a monetarist to use it.

The equation is: M*V = P*Y

Where M is money supply, V is the velocity of money or propensity to use or consume money. P is the prices of goods in the economy and Y is the output or amount of goods.

All of these are observable in hindsight. Money supply leads the others, though, given it takes time for it to work through the system. Money supply grows not when the Fed grows its balance sheet. That is only creating bank reserves for the most part. Money supply grows when banks create credit and make loans. This is the big driver of money supply. It is why M2 did not grow that rapidly after the GFC.

For velocity, we can only try to anticipate what the demand for and ability to get loans looks like. We spoke about housing last week. It will continue to be difficult as mortgage rates will remain high. There will be even less demand if employment starts to suffer. Do you think small businesses will want loans if the outlooks is bleak? Will they even be able to get loans if banks are tightening standards? What about CRE loans? What about venture capital firms?

I think it is fair to posit that velocity will continue to fall. This at a time when M2 growth is negative for the first time in history that I can find. Negative money growth and falling velocity. What does that mean for output and prices? On the plus side, this means inflation could fall. However, economic growth is going with it. This is why JayPo knows that the next phase of the cycle is the credit tightening slowing the economy and slowing inflation. This is why the Fed can pause. However, this is NOT a bullish pause.

Finally, I want to touch on a topic I have heard several times in regards to a possible ‘solution’ going forward: Central Bank Digital Currencies. The argument goes, that in a time of crisis, the biggest concern is the uninsured deposits because the other deposits under $250k are already insured by the government and funded by banks paying an insurance premium for this privilege. Who has uninsured deposits? Businesses that want the liquidity of a bank account to conduct transactions - payroll, rent, paying suppliers etc. If the government is going to guarantee uninsured deposits anyway, it may as well control these transaction accounts, pay 0% rate, and conduct this business using Central Bank Digital Currencies. Why backstop banks to do this and let banks make a spread? Aren’t we just subsidizing the banks? If customers want a yield, they can go to banks, but then it is at their own risk and they have to do diligence.

It sounds so appealing and simple. However, do you realize the control that would be voluntarily given over to the central government if this were to happen? The government is already trying to get visibility on transactions over $600 in every bank account. If every transaction (read: checking) account that used to be at a bank was now at the Federal Reserve, the Fed would know every transaction that is occurring and have a record of it on an immutable ledger.

I am neither a conspiracy theorist nor anarchist. Far from it. However, this level of control and oversight, of all transactions occurring in the economy scares me far more than any recession we are going to see in 2023. We need to be very aware of the central government usurping power during times of trouble.

As Chicago native Rahm Emmanuel, Barack Obama’s Chief of Staff, once said: "You never want a serious crisis to go to waste."

Stay Vigilant