Preparing for things to come

Whether you are getting ready for guests to join you for the holidays, or thinking of how to position your portfolio for the coming year, now is a time of preparation

As we approach the Fall Break at colleges and the Thanksgiving holiday, my wife and I have been busily preparing for kids coming home, a week of events with friends and a traditional get together with family. While the biggest celebration may happen on one day, it takes days if not weeks to get everything in order for it. It is useful at times to have this type of catalyst because projects finally get completed when there is a definitive target date to shoot for.

This is not uncommon in the financial markets. There have been many studies done about the behavioral aspects of investing especially when it comes to the year-end effects. However, perhaps less apparent to many investors is that there is preparation for this year-end long in advance. Mutual funds, which still make up about 55% of the market based on to whom you ask the question, prepare for the year-end distributions which typically happen in mid-December, by their actions at the end of October or early November. For a discussion, CNBC posted about this not too long ago here.

This means mutual funds have been selling winners and losers (mostly losers) in an attempt to reduce the capital gains taxes on those distributions. This leads to particular pressure in some parts of the market. Perhaps it is the relief from this selling pressure, combined with the obvious greed of fund managers and hedge funds to push stocks higher in order to maximize a bonus, that leads to the positive seasonality we observe in the markets. Of course, we do not always see this and in down years it is typically less present, however, there is still the expectation for this ‘Santa Claus Rally’ among many in the market.

More prudent investors are preparing for the year-end by anticipating what will happen in 2023 and preparing their portfolio accordingly. Most will tell you the markets are forward-looking and while I agree, I am sympathetic to the idea that as a higher % of the market has moved to passive funds, the number of days the market looks forward has certainly reduced some. That said, I think it is still fair to think that investors, whether tactical alpha traders or asset allocation real money, are anticipating what the cycle will bring in the coming 1-2 quarters which takes us into 2023.

As you know, that is part of my constant process to assess the Fundamentals, Behavioral and Catalyst aspects of the market. I did so last week and want to do so again this week by looking at a few different charts than I did last week.

FUNDAMENTALS

In my Applied Portfolio Management class, we build on the concept of the Investment Clock that was popularized by Bank America Merrill Lynch in the early 2000s. We assess the economy from a growth and inflation standpoint, and then observe both the empirical results of what that has meant over time, but the real-time results of what the market is pricing in right now.

If we observe the sector performance on a YTD basis, I would call that classic ‘stagflation’ behavior of the markets. When I say stagflation, most immediately think of the dreadful 70s, and that is correct. However, stagflation broadly speaking is when growth is falling but inflation is remaining firm and above trend. This is what we have seen this year. In those cases, the Investment Clock would recommend overweights in Energy and defensive value stocks as well as underweights in high growth tech because the market is going to struggle. This is exactly what we have seen.

Over the last week or so since the FOMC meeting, the market has shifted and begun pricing in more of what the Investment Clock calls deflation but which is typically seen as recession - growth still falling and inflation starting to fall as well. This is typically a negative time for the markets but of course we are already down a fair bit and there are strong seasonals to contend with. However, in this phases, we would expect Energy to give up its gains and for Staples, Utilities and Health Care to do well. That is exactly what we have seen the past week.

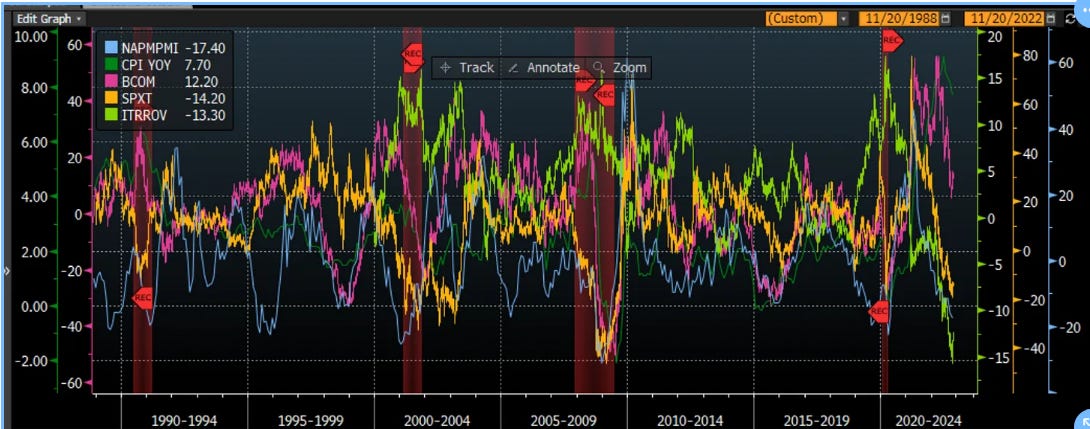

Looking at the set-up more broadly across markets, I look at stocks (SPX), commodities (BCOM) and bonds (ITRROV which is US Treasuries) overlaid vs. my measures of growth (PMI) and inflation (CPI). A few things stand out from this 35 year view. First is that commodities have tended to rally into a recession and then fall as the recession unfolds, suggesting that higher commodity prices are a cause but that the market anticipates the falling demand in the commodities themselves. We are seeing that now. Second, the stock market does appear to be forward looking and has begun selling off before the recessions begin (shaded red). Of course, these recessions are only identified after the fact by NBER but we can see that there is some leading nature of the market. Finally, we tend to see bonds rally at the beginning of a recession. This has NOT happened this time around because inflation has been higher than at any period in this sample, but perhaps this is where the opportunity lies at this point in the cycle, more so than even in being bearish equities which have already come down quite a bit. Thus, the markets are starting to anticipate a recession, but perhaps haven’t fully embraced it.

I am not sure if Mike Kantrowitz from Piper coined the acronym HOPE for the cycle, but he says he did, and I trust him. I have a good feeling the logic behind it came from when he worked with Francois Trahan in his early time in the market. Either way, I got the notion of watching housing from both of these strategists who have earned their stripes in the markets. The logic is housing, which has a large multiplier effect, leads the economy into and out of recessions. New orders follow housing, with profits and employment lagging indicators. This is what we are seeing now.

I am not going to belabor the slowdown in housing in the US because it has been discussed by many. I just wanted to show a few other charts I look at, that I don’t see others watch. The first is an index I create by calculating the number of existing homes sold by the average sale price of existing homes. This gives me an estimate of the dollar amount of home sales in the country. I look at existing home sales because they are 80-85% of total home sales. I look at the dollar value because this is what people are getting paid on: commissions for realtors, money in the pockets of generals and subs who fix things up, and the multiplier effect we discuss. You can see this measure in white that has been falling all year long, first as prices fell and then as activity fell. New orders eventually followed suit and have fallen. We have not seen employment affected yet, but this is a foregone conclusion. The jobs market has been the last pillar in the soft-landing story.

Another housing measure I watch puts a slightly different spin on housing and tells a slightly more positive story. Much is made of the mortgage rate which has double this year. However, my premise is that the mortgage rate is but one (of many) of two big determinants to the decision to buy a house. The other is whether one has a good, stable job. After all, if mortgage rates are zero, but you are unemployed, you aren’t going to buy a house. Similarly, mortgage rates can by 15% as we saw in the 70/80s, yet people still bought houses. So it isn’t just the rate piece. I created a simple geometric index that combines 30-year mortgage rates and the unemployment rate. This index is in white. The blue line is the oft-cited NAHB realtor index. The horizontal lines are the average of each series over the last 24 years (NAHB in white and mortgage*jobs in red). While the mortgage rate has gone up, the lower than usual unemployment shows the combined index has risen, but not extremely so. In fact, it is only at the average of the last 24 years. The realtor survey of activity has fallen and stands below the average of the last 24 years. We can also see that housing has led us into and out of recession each time over this period. This has typically been matched by a rise in the mortgage*jobs rate, but that has been when it is above average too. Fact is, this measure has been extremely supportive for housing for almost a decade.

If we dig into the mortgage rate itself, I like to do so by comparing it to the 10-year Treasury yield. Typically bankers would price mortgages as a spread to 10-year because that is the most liquid future they can use to hedge their convexity risk. As bankers get nervous, this spread to 10-year widens and capital becomes more scarce. This time around, it does not appear to be bankers getting nervous, but the Fed making a mess of things via QT and imposing this convexity risk back on the market. However, as we saw in the GFC and Covid, this spread does not typically stay this wide for too long and I would expect it to narrow back to the 2-2.5% range in the coming year. This is a positive influence on mortgage rates even if the 10-year itself stays in the 3.5-4% range. It implied mortgages around 6% in the coming year. The question will then turn to whether people have jobs that even allow them to afford this rate.

For the most wholistic view on the housing market, I would refer you to the Odd Lots podcast that was done with Jim Egan from MS: https://omny.fm/shows/odd-lots/this-is-what-7-mortgages-will-do-to-the-housing-ma

Jim makes a great point that we should consider. Perhaps we should consider that housing prices do not have to collapse with rates where they are because while demand has surely fallen, so will supply. Builders won’t be able to affordably build but importantly, people in existing homes (80-85% of the market) won’t want to sell to trade up or move to warmer climes because they are locked into a low rate mortgage. Perhaps activity just slows to a halt. This is good news for house prices perhaps, but still bad news for the economy.

Sorting through all of this, from a Fundamental standpoint, I still see that we are going to be moving into a recession in the coming quarters and that the market is only now really starting to price that in.

BEHAVIORAL

I am just going to touch on a few charts here. I believe it came up on my podcast with Barry Knapp where he referred to watching more what people do than what people say. I typically look at both, but today I will focus more on what people are doing, because almost all I hear people say is negative.

John Hussman (uber bear admittedly) shared on Twitter a graph of the 250 day EMA of the SKEW Index vis a vis the SPX. I have always looked at the SKEW and CSFB Indices in this section but had not looked at the long run moving average. The logic as I see it could be that as people get more bearish, they stop purchasing the OTM insurance and simply give in and sell their stocks. They have lost some sense of hope. Perhaps that is not entirely accurate, however, in my 30 years in the market, I can tell you I have gotten to that point, and I know many others have as well. If I look at the 200-day moving average of SKEW (which measures the price of the OTM options vs. the ATM), and advance it by 4 months, I can see that big drops in the SKEW moving average have coincided with big drops in the market. There is some noise in here for sure, as no indicator is perfect; however, it may suggest that there could be more downside in the market from here.

I like to focus more on the shorter-term activity in options. Options are an instant gratification vehicle. If you structurally buy options, you will structurally lose money and have a drag on performance. However, if you use them tactically, and do it well, you can substantially improve your Sharpe Ratio. I look at both the CBOE put-call ratio as well as the total US composite put-call. I smooth each out by considering the 20-day moving average. When this measure rises, it is bad news for stocks as hedging is picking up. When it falls, it is good news for stocks as hedges are being unwound. It has worked very well this year. Right now, the CBOE measure has hooked higher, but this is not corroborated by the US composite. As they move together, i expect it also moves higher. This should be bad news for stocks in the near-term.

I also like to look at the technical charts to get a sense of where the pain points are and how investors will behaviorally respond. We can see from the daily SPY, the market had broken out above the range (in blue) where buyers and sellers had accumulated positions. The bulls were in control. However, the market ran into resistance, and we can see the lagging span (in red) run into this resistance. Now the MACD is starting to roll over. That 389-390 ish level that was support then resistance and now support will be the level the bulls need to see hold in the coming days.

I mentioned earlier that perhaps the opportunity lies in the bond markets. After all, if we are going to see a recession, we have already seen stocks sell-off and now are seeing commodities lower too. We would normally see bonds higher, but this has not happened because inflation has been too higher. There is no strong signal on the daily chart for TLT (long duration bonds) but on the weekly chart we can see that the MACD is turning higher suggesting a change in momentum at the same time we are coming off a meaningful oversold RSI that is also turning up. The first resistance I see is the previous support that comes in around 113 in TLT, about 13% higher. This might be the better recession trade than short stocks here.

I also look at Commodities on a weekly chart. The daily chart confirms that recession is being priced in as it is quite weak. However, the commodity bull story is one of secular under-investment and a potential secular bull market as supply has been permanently taken offline in many markets. On a weekly basis, that secular bull is being tested here, as we are at support levels on the Ichimoku cloud and the weekly MACD is starting to turn higher. While the daily prices can press a little lower, the secular bulls will need to assert themselves to maintain control of this market. With cross-currents, I am watching this asset from afar right now.

A positive story for risk right now is possibly the dollar having topped. As the dollar wrecking ball (hat top Michael Kao) thesis played out, risky assets globally struggled under the weight of a strong dollar. The weekly chart - price, MACD, RSI - all suggests a top is in and we should move amount 5-7% lower in the coming weeks. This should be positive for risk.

I wrote about the potentially weakening dollar on Linked In this week:

“Chart of the Day - end of the line. We are approaching the end of the semester & it is becoming pretty stark it is the end of the line. We have Fall Break next week & when we return, there is just one & a half weeks of classes before finals. We are discussing the final presentations for clients in many of many meetings. For many students, it will also be the end of their Masters program & graduation is close. It really feels like the end of the line.

It may also be the end of the line for the Fed. Some at the Fed, led by Brainard, are talking up that idea. Others, led by JayPo, are saying 'not so fast'. The mkt certainly is starting to think so as the terminal Fed Funds were 5.1% right after the Nov FOMC & are now 4.9%.

You see it the most is in the US Dollar. Dollar strength has caused a bit of damage in countries & companies around the world that are short $ because they borrow in $ against their export revenues but end up short when those revenues decline. After almost a 20% move higher this year, the $ has pulled back 7% from the highs. That is not a small move on its own.

When I see the $ move like this, my first instinct is to ask what is driving it. Is it relative interest rate differentials? The obvious place to look is US vs. Japan given relative policy decisions. At the peak, the spread between bonds and JGBs hit 4%. It is now down to 3.4% suggesting a top is in.

It may also be due to my preferred forecasting tool of FX which is relative growth rates. In the past couple of weeks, the idea of a US recession has really crept it. This has been echoed by retailers like TGT & KSS this week which are telling you US consumers are slowing a lot. The US PMI is finally catching up (down) to the PMIs in the EU, China, Japan, Korea etc.

My second instinct on big dollar moves is to look at the relative performance of EM to the US. This is very sensitive to the Dollar as EMFX & EM stocks/bonds are very highly correlated. Weak FX means weak stock & bond mkts as capital flows out. The converse is true. EEM should start to do better vis a vis SPY if the Dollar has indeed begun to top.

One problem with EEM (in blue), though, is the heavy exposure to China. With Xi Jingping's Common Prosperity & crackdowns on the successful, it is not clear at all that shareholders (esp. US shareholders) will be allowed to be rewarded over Chinese workers & consumers. As a result, I also looked at an index I created with just Mexico & India. In my podcast on Substack I spoke about India, the tremendous demographics & tailwinds to the economy. Mexico is benefitting again from USMCA & the reshoring/near-shoring of businesses to North America. If you look at this index in white, it has always tracked the EEM very closely. This year there has been a decoupling. In fact, Mexico & India combined are up on the year.

Even in bear mkts there are things to invest in.

Stay Vigilant

#markets #investing #emergingmarkets #dollar”

The last measure of Behavioral sentiment I wanted to discuss was crypto, which has been the story of the last couple of weeks. I am not going to do the forensics of the FTX story as you can get that from many other places. However, I put my two cents on the broader crypto story on Linked In this week:

“Chart of the Day - voyeur (n): a person who enjoys seeing the pain or distress of others. I watched Thursday night football not because I am a fan of either team. I am a Bears fan. I watched to see the Packers suffer & lose. I was a voyeur. I came away quite happy.

I see a lot of voyeurs on LinkedIn & Twitter when it comes to crypto. I'd guess few have any direct interest. They aren't short any of the coins blowing up. They are enjoying the pain of others. They are not direct fans. They are voyeurs.

I get it. Terra/Luna, Celsius, 3AC & FTX show that there were flaws/fraud in the system. This validates some bearish arguments. This has set back the industry by yrs. It has cost institutional investors billions of dollars that may never come back into the space. It doesn't mean it all goes away.

Today I show Bitcoin & Ether. Combined they are 53.7% of the $873bb mkt cap of crypto. There are 000s of other coins that make up the balance. Most people think only of crypto as the coins & not the technology disruption behind the coins. The coins are just the funding vehicle for the project, like SAFE notes in angel/seed/VC. Many of the VC deals fail, like 90%. Many coins will fail. That does not mean the technology disruption won't occur.

Bitcoin isnt going away. It may not go to 1mm either. US investors don't understand the use case of Bitcoin. They don't need to as the $ is quite strong & accepted everywhere. However, Bitcoin makes a lot of sense for people subject to fiat ccy that has or will massively devalue. This is no small part of the world. US consumers also do not have a large amount of remittances abroad. Other countries rely on this. Philippines has 10% of its GDP in remittances. Saving fees on this amount of money makes a massive difference. Bitcoin may not be for US investors, but it isn't going away.

Ether is also not going away. The Ethereum network is home to DeFi & smart contracts. I did an entire podcast series on DeFi (link in comments) showing the use case for DeFi. FTX is NOT DeFi. FTX is CeFi. It was an unregulated copy of the TradFi world with exchanges, traders & brokers. It was inferior to the traditional world. DeFi is rebuilding that infrastructure. The industries most likely to be disrupted are those where the customer experience is a pain point. Has anyone had any pain points with their bank or broker? Do people love their fincl services?

NFTs are also not going away. I am not speaking of Bored Apes. I am speaking of the ability of content creators like artists, musicians & writers to connect directly with their fans. I am talking about fans being able to get more value via unique experiences or equity ownership in projects. The content industry needs to be disrupted & it is.

Broadly speaking, web3 is not going away. It is the next iteration of the internet which needs to be disrupted.

Be careful seeking advice from voyeurs. They don't have skin in the game.

Stay Vigilant

#markets #investing #cryptocurrencies”

A very mixed bag on the behavioral front. There are plenty of headwinds to risk-taking if I look at the options market and SKEW or put-call ratios. In equities, the bulls have a critical level to defend this week to enforce the positive seasonality in stocks. The falling dollar might be a signal that the bulls can control stocks from here given its correlation to risk. However, a more positive technical picture in bonds suggests that tactical asset allocators may see more possible upside in bonds than stocks, especially given the fundamental picture, and could prefer that market. In EM, there might be some positive news but in crypto, another risky asset, we know the near-term news is quite poor. Too many mixed signals to get a strong sense of whether the supply/demand of the financial markets leans pro or anti-risk from here.

CATALYST

Finally, what catalysts are left in the market that may get investors to change their minds. We are past earnings and discussed those last week. We have another Fed meeting coming up and it appears the Fed might be slowing getting out of the way, but that is likely because they have already done their damage. From here, the biggest catalyst will probably be the economy - whether we can have a soft-landing or if we have a recession, how long and deep will it be.

A measure I always look at but haven’t shown in a while is the Citi Economic Surprise Index. It looks not at the data in absolute terms, but whether it is better or worse than expectations. Frankly, right now, I am not even sure what the market is rooting for. When we were in stagflation, good economic data meant more Fed. Bad data meant less Fed but also falling earnings. Now that we might be starting to go into recession, bad data probably confirms that and takes away the soft-landing. Good data might lead investors to believe the soft-landing. I think this pivot will happen more so after the December FOMC meeting. Either way, analysts adapt to the data and if it is consistently better or worse, adjust their expectations. It has been worse for some time. Lately it is about as expected.

Comparing the US data to the rest of the world, you can see the US and Europe have been better than China and EM for most of the latter part of 2022. In the last month, though, the relative surprise in China and EM looks a bit more positive. This is coinciding with a declining dollar as well. It might be that the marginal dollar of risk-taking begins to look to Asia and EM and not the US or Europe.

Narrowing down the focus to inflation, we can see when the market expects the Fed to start to back off. I use three different measures of inflation expectations - that from the TIPS market in white, that from the swaps market in blue, and that from the Citi inflation surprise index in orange. All are starting to weaken and suggest we have seen the end of the inflation story for the time being. If true, this could take the Fed out of play in the early part of 2023 and shift the focus of investors.

Finally, one must always consider geopolitics when assessing the possible catalysts to the market. The Ukraine fiasco has proven that to us again. However, now that we are potentially in a new multi-polar world as many of my podcast guests posit, it is ever more important to ascertain where the risks in the world can pop up. For this, I will point you to the Alpha Exchange podcast where my friend Dean Curnutt interviews Rob Dannenberg, another friend and former CIA agent. Rob gives a great overview of what investors need to worry about.

https://www.stitcher.com/show/alpha-exchange/episode/robert-dannenberg-former-chief-of-central-eurasia-division-cia-208578920

Right now, there are no major catalysts to get investors to change their minds meaningfully yet. The behavioral supply and demand are very mixed, with some positive signals and seasonality, but also some headwinds. The fundamental trend of risk is lower as we are headed more urgently into a recession led by housing. The market is finally sensing this and pricing this into risk markets. Even in a recession and bear market there will be opportunities, and perhaps this is now in bonds, or potentially in certain emerging markets like Mexico or India. As we look ahead and prepare for next year, it is time to consider how you want to set your portfolio up for 2023.

It is also a time to Stay Vigilant

Excellent. I especially appreciated your fair treatment of crypto. Just a few hours ago I Tweeted something to the effect of, "Yes I understand how horrible things are in crypto land right now, but the technology has not actually failed." Bitcoin and Ethereum remain unchanged, still producing blocks.

As I was reading your article another thought occurred to me. We all make jokes about retail investors buying the highs and being so bad at timing markets. We laugh as they (I am part of the "they") buy the rips that the so called sophisticated investors are selling. Yet when prices are attractive, as they are in crypto now, there is so much pressure on Twitter and in the media to get the hell out! Never touch this awful stuff! You would be insane to buy crypto!

Market commentators make it difficult to buy at/near the lows. Does that make sense? I'm just hashing out ideas here, maybe my thinking is not coherent.

Buy low, sell high, yet when prices are low it can feel like the entire world will call you a fool for buying that most hated of things.