Reader Q&A

This week I am answering questions that readers sent in

Thank you to those who sent me questions. I love to hear the questions and comments from folks because it helps me see where other people’s heads are, what they are focused on, and where sentiment may be. I will keep all of these anonymous in case people don’t want their names used.

Here we go

The first question was about my comment on a market of stocks vs. a stock market. How do I determine where we are? Is it just the seasonality of earnings of is there something else?

For this, I like to look at implied correlation:

We get this measure from the options market. It uses the stocks in an index and the index itself. We look at the implied volatilities of the single stock and index options. It is a good measure to help us see what the market is expecting on a forward-looking basis for the movement of stocks and the market. If traders expect the stocks to move as one, implied correlation is higher. If it expects more divergence between stocks, it is lower. You can see back in the Financial Crisis, implied correlation got over 80%. The current reading is 16% or the lowest since we have this data on Bloomberg. This is a market where it foresees very little problem on the horizon. It is a market of stocks.

I got a number of questions regarding the recession view. Most along the lines of ‘isn’t it time to throw in the towel on the recession view?’ A couple of things on this front. First, I didn’t think we would have a recession last year. I thought the housing and travel industries would keep us afloat and a recession would start late Q1 or Q2 this year. I also thought this would be what I called a ‘jobful recession’. I thought we would see the exact opposite of what we saw after the Financial Crisis when we had a jobless recovery. At that time, the top 10% did very well but the bottom 90% struggled more. This time around, I think the bottom 90% will do fine and the top 10% will struggle. The bottom 90% seem to be doing very well as they are still working and they are seeing wages move higher. The layoffs are in tech and financial services, largely the top 10%. I know GDP is still strong. It is backward looking though. The Leading Indicators are negative. Every time they have gone negative we have had a recession. Perhaps it is different this time but it still seems like later this year a recession will hit, but I would still expect the jobs data to stay pretty good.

Another few questions were on the momentum of the market. If you look at every index, we are breaking out to new highs and it looks like the all-time highs could be in site. Adding to that is the clear psychology of investors. Active managers, long only and hedge fund, can’t take it anymore. They have to throw in the towel. This will only accelerate when they get back from Summer vacation post Labor Day.

With hedge funds, the last 6 weeks we have started to see the most shorted names outperform the broad index. The first thing a lot of hedge fund managers will do is to reduce short exposure and lean net long (if they can) before going all in and grabbing beta. We are starting to see that.

We are also seeing the Zombie stocks perform well. Zombies are those whose earnings before interest and taxes are less than their interest expense. These are essentially dead companies that could survive when rates were zero. Can they survive with rates over 5%? These stocks on average (15% of the Russell 2k index) are up 26% vs. the index up 8%. This are very low quality companies yet they are performing well because shorts are being covered.

Finally Q4 seasonality is strong for the markets. Portfolio managers know this and if they are lagging the benchmark, there will be a chase I think.

Even small caps, which have lagged all year, are starting to look strong on the charts:

My biggest fear is that we get a move higher that brings people in just as we start to get really bad data on the economy, with a Fed that is still in play. I don’t think we get a crash, but this set up is what happened in 1987. Just at that time, the market structure was broken which exacerbated the move. I think we could get a more muted version of this possibly.

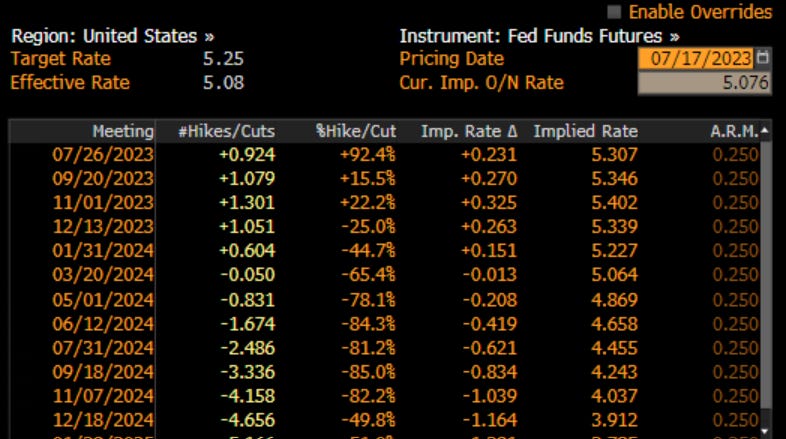

The final question was about my views on the FOMC. When will it stop? Have we seen the last move in the cycle? When will it start to cut?

The market still sees 1 more move higher but it sees many cuts next year. The cuts have been pushed out (recall the cuts were priced in starting this summer at one point) but even while pushed out, they are aggressive in the number.

Even the FOMS itself has cuts priced in for next year and beyond

Goods inflation is falling rapidly. However, wages are still going higher which is why sticky inflation stays so high. This is why I think rates will not move lower even if we get bad data. The FOMC has wanted to normalize policy for some time and we are finally getting there. While the FOMC was hiking a lot early last year, policy was still easy because real rates (I look at TIPS market) were still negative. We are only now getting into sufficiently restrictive real rates.

I would keep an eye on real rates. I don’t think the FOMC wants to see these go back into negative territory again if it can avoid it. It took them there when deflation was the threat. Right now it still sees inflation as the threat. I know the demographic, technology and debt arguments for lower rates longer term. However, I think that will take a very long time and for the foreseeable investment horizon, we should be thinking of policy rates in the 5%+ territory.

Higher real rates tell me that multiples on stocks should go lower, which means earnings have to drive the market.

We shall see. For now, thank you again for the questions. Remember to …

Stay Vigilant

My working theory is that we have been in a sector specific recession since mid 2022. A recession that is impacting certain sectors at a time. Software and tech was the first to get hit, then manufacturing, then housing, recently energy. Who’s next? Likely autos and travel. This time is different and this recession is also likely different. The COVID shock to the economy was strong and now that pendulum is swinging back and forth as it tries to find its new equilibrium.