Risk vs. Reward

This is the primary theme that runs through all of my finance classes from investment research to portfolio management to derivatives to starting a new business. How does it stack up in the markets?

The theme of my LinkedIn posts this week was risk. I did this because I was starting a 5-week Pro Series Options Workshop for the CME Group on Wednesday (you can find last week’s video and sign up for the coming workshops at https://www.cmegroup.com/articles/videos/webinars/2023/cme-group-pro-workshop-series.html). In addition, I was appearing as a guest on Friday on the Options Insider Radio Network “Volatility Views” show. Finally, in my portfolio management class, we were speaking about derivatives and intermarket analysis. Thus, volatility and risk were top of mind.

As I went through the week on subsequent posts, I got the sense that risks were rising. We spoke a bit about this on the geopolitical front last week. We saw this from some of the early reporting on earnings as well, which I will cover next week. This week, I was focused on the market measures of risk and what the market thought was about to happen.

Conditions ripe for risk?

My two favorite analogies when it comes to assessing volatility and risk come from Sheldon Natenberg and Christopher Cole.

Shelly says that forecasting volatility is like forecasting the weather. There is serial correlation and mean reversion. The serial correlation means that our best guess for tomorrow or next week may be something that approximates what we are seeing now. For a long-term forecast, maybe next month or next quarter, we rely on mean reversion i.e. where are we vs. long term averages. Recently, volatility had been below average. Traders seemed to suggest this would continue. However, long-term, we were below the mean, thus we should expect a move higher. I think traders are starting to change their mind on that timing.

Why? I think this is where Chris’ analogy comes in. Chris, who is from California, says volatility is like a forest fire. We never know when a forest fire may start. We don’t know when a rogue camper or a gender-reveal party may literally spark a massive fire. However, what we do know is when the conditions are ripe for a fire. This may be seasonal or it may be because conditions are very dry. It may be because of poor forest management. Well, when it comes to volatility, what do we know? Seasonally, October has had its share of bad months through time. Yes, it is positive on average, but some of the most cataclysmic losses have come in October. Throw in illiquid conditions because of central bank removal of liquidity, the backup of bond yields and a higher dollar, and conditions may be ripe. Is there also poor risk management? Could 0 DTE options be creating a market structure ripe for a flash crash? This is Financial Conditions and the VIX.

Risks Rising?

Chart of the Day - risks rising? (I spoke on Tuesday on LinkedIn about rising risks)

I know I have spoken a bit about the rising macro risks in the world of late. I will still stand behind that even if stocks rallied yesterday on the hopes of things calming down (calm before the storm imho unfortunately)

I open my Bloomberg today to a story titled: VIX Is Primed to Surge Higher as Credit Cycle Turns: MacroScope

The opening paragraph sets the tone for the entire article: The rising wall of corporate loans and debt to be refinanced will increasingly stress company balance sheets, leading to a secular rise in equity volatility.

This is something we will be talking about in class soon enough. We will be analyzing the banks in the next month or so. Given we track the Russell 2k, these are all small regional banks. Loan losses (and deposit flight) will be an issue

This reminded me of a graph I have looked at several times through the years but have not done so recently. It compares the Treasury yield curve (inverted) to the VIX. The logic is simple, as the yield curve inverts, bad things happen. When bad things happen, the VIX reacts

There is a 2.5 year lead time because the yield curve has a great hit ratio but a variable lag. Sometimes it is 1 year, other times it is 3 years. On average the slowdown led by the inverting yield curve compressing bank margins & therefore slowing the flow of capital is a little over 2 yrs

We can see that based on this chart, the VIX could be headed for a much higher regime in the coming months. Again, capital not flowing to the economy will cause problems for companies & we will see this in the moves of the equity mkt

I can hear the pushback on two fronts. The first front is that the mkt only cares about 0 DTE options now and no longer looks at options beyond 1 week. Thus the VIX is no longer a valid way to ascertain risk

I would suggest that we have had expiring options for a long long time and there is no reason that this time is any different. Institutional funds hedging portfolios will not be looking at 0 DTE options. These are the flows I am trying to see, not the day trader flows

The other is the changing landscape for loans. I listened to a podcast on Real Vision yesterday that talked about the mkt share gains of non-bank loans vis a vis bank loans given the lack of regulatory requirements

I have written about the bull mkt in private credit that I have seen first hand. The money flowing into this space may in fact overwhelm any loan losses especially in a mild downturn. I am open to the possibility

However, this is again saying 'this time is different. Whether one is a bank or non-bank entity, a slowing economy is not one into which people like to make loans. On the way out, sure, but not on the way in. So if there is no landing, perhaps the VIX doesn't rise. In all other scenarios? I take the over

This is a chart from the Macroscope column, which also suggests VIX may be rising

Other drivers?

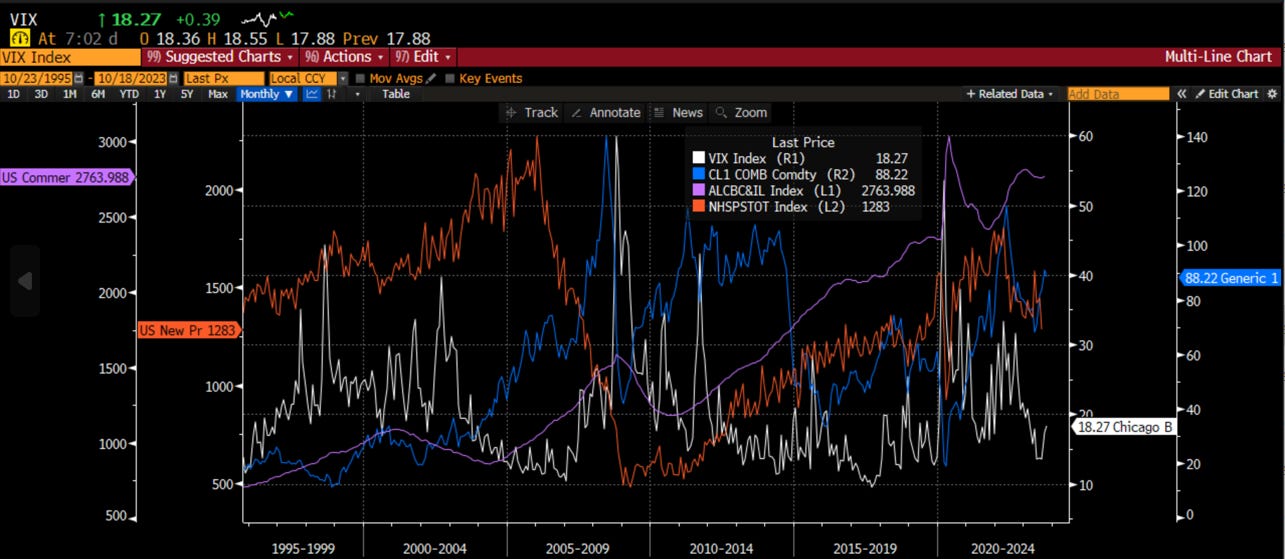

Chart of the Day - crowd-sourced (I spoke on Wednesday on LinkedIn about some other drivers)

Today's chart comes from an idea good friend Matty put in the comments of my post yesterday. Recall I looked at the yield curve vs. the VIX and referenced an article that mentioned credit spreads & VIX too. Both pointed to higher VIX

Before I get into this chart, I also saw a lot of crowd-sourcing and good dialogue today in the first of five options workshops I am doing for CME Group. If you have not signed up yet, I will put a link in the comments. We covered basic options strategies today & will build from there the next 5 wks

Onto the chart now, Matty asked for an overlay of the VIX vs. crude, housing starts and loan growth (I used commercial & industrial loans here). I had no idea what I would find when I put them together so let's look at it all together

The first thing that stands out is that spikes and collapses in the price of crude seem to somewhat coincide with rises and falls in the VIX. Crude is in blue and VIX is in white below

This makes sense to me because often the spikes in crude are about geopolitical risk or risks that the status quo is being upended. If you are expecting higher oil from here, should you also expect a move higher in VIX?

Next let's look at housing starts in orange compared to VIX. We can see the collapse in housing starts ahead of & leading to the fincl crisis. As housing began to recover, it showed a recovery in the economy which ultimately meant less variability in idiosyncratic risk.

If housing starts start to suffer now (they were lower today) because of the high cost of capital & the low availability of capital, could this signal that we are going to see a rise in the VIX? Flipping it around, to suggest we will see lower VIX, we should also see higher housing starts suggesting a stronger economy

The last is commercial & industrial loan growth in purple. Honestly, on this one, I don't see much of a connection at all. If anything, it seems as loan growth decelerates, the VIX is lower & as loan growth accelerates, the VIX rises. This is counter to what I might expect.

We also don't see a consistent pattern so I would suggest there may be no relationship here. Perhaps this is because we need to add in other types of loans (mortgages) or other players (private credit). I will look for a better measure

All in all, I think there are some relationships here. As someone who thinks crude can rise and housing starts could fall, both of which would suggest a higher VIX, it makes sense to me but I also may be at risk of confirmation bias. Then again, I didn't seek this out it was crowd-sourced (thanks again Matty)

Join me on those options workshops. Would love to have you and dialogue there

Risk across assets?

In my portfolio management class, we speak about intermarket analysis as well as derivatives. Even though we have an equity portfolio (where the client lets us use option strategies), I make the point that we can learn a lot from what the other markets are telling us.

When we look at risks across markets, it tends to move together because risks are a function of liquidity, and as one market or strategy is affected, asset allocators tend to pare back on risk in others. We can see that equity volatility (VIX), bond volatility (MOVE), credit spreads and FX volatility (JPM) move together over time. We can also see that recently, it is only really the bond market that is perceiving any risks to the market.

We know these will come back together at some point but we don’t know if that means the bond market recedes or equity volatility and credit spreads widen. If we look at the last two days last week, it started to look like idiosyncratic volatility in equity and credit is starting to suggest that this bond market volatility is for real.

That is something I covered on the Volatility Views podcast on Friday. In fact, if we look at the volatility of volatility, or the risk priced into the VIX options, where the index itself is a risk gauge, we can see the nervousness in VIX options is a leading indicator. In fact, some of the most popular options being trader are December, January and February 40-45 strike calls. That is a double from where we are now. Those are tails that people are buying incase risk really blows up.

Traders often use the shape of the VIX futures curve (1st vs. 4th future here) as well as put-call ratios to give a signal on near-term market risk. I have shown these before. We also spoke about the VIX curve on the podcast. It is nearing a flat level from its normal contango (upward sloping). If it goes into backwardation (downward sloping), it is a signal things are happening or are about to happen. If it gets very steep, it can be a contrarian signal but for now, it is a red flag. They asked my forecast for the VIX on this coming Friday. I was the high person at 27.72.

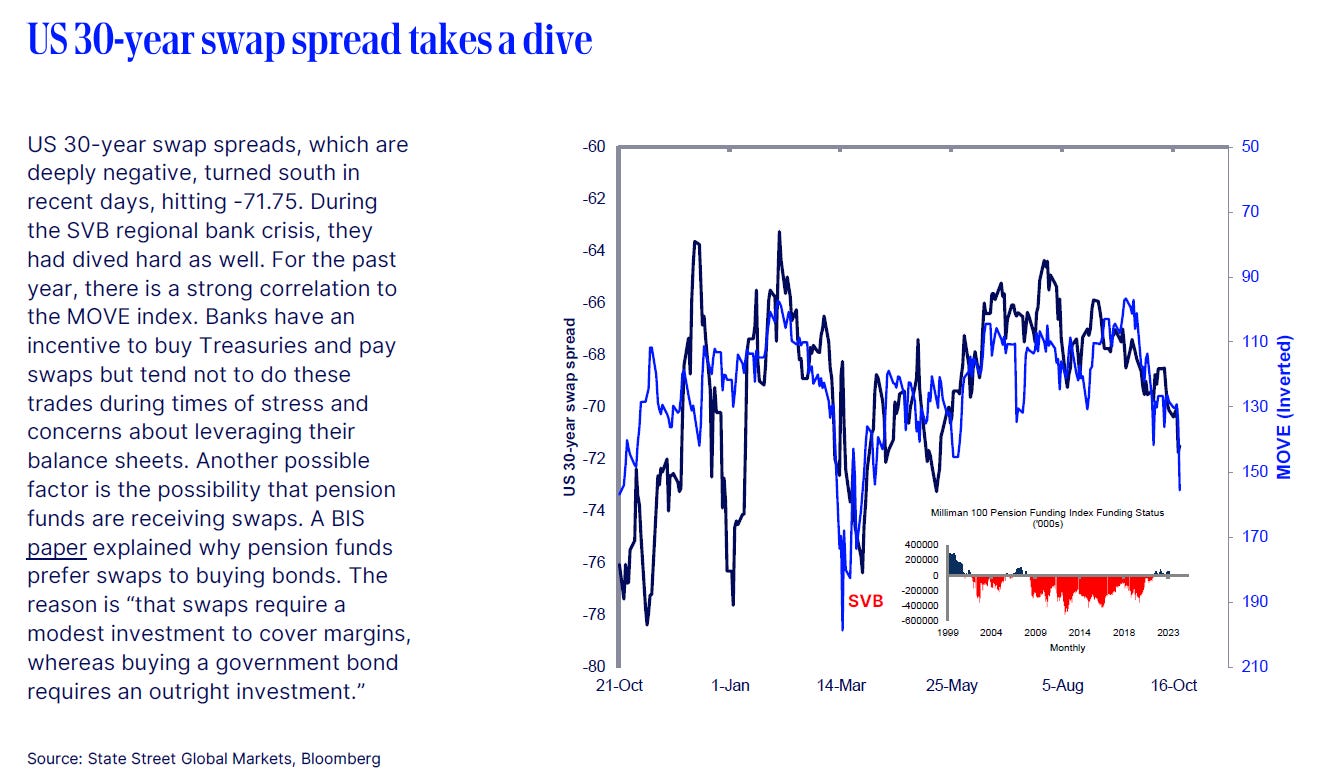

Swap spreads and bond risk

Friend of the program Mr. Risk puts out some great charts every week. Always thought-provoking. He had this chart this week that really made me think that the risk we see in the bond market may not be going away any time soon. The information in here is also being corroborated by some banks, but we really want to hear more form the regional banks still to come.

10-year risk

Chart of the Day - magic (I spoke about the US Treasury move on its own in a LinkedIn post on Friday)

This week is Homecoming. Lots of events for the students & alumni to attend in the lead up to a very critical game against our rivals to the north. Illinois vs. Wisconsin is a proxy war for Bears vs. Packers

One of those events was a comedy/magic show by Derek Hughes who was a finalist on America's Got Talent. He was terrific weaving in comedy while doing tricks from disappearing/reappearing items to mind-reading.

It makes one think about what tricks the magician is using to confuse, entertain, trick, freak out & otherwise generate a wide range of emotions. Those wide range of emotions seem to also come from any discussion of the 10 year US Treasury yield, the benchmark price for every asset class. I thought of four

Misdirection - this could be of time or attention where the magician diverts the audience from the secret acts they are performing. I am guessing there was a lot of this going on

For the 10 yr yield, I think the growth narrative has been a big part of the misdirection that is used in the market. While I really don't think better than expected growth expectations are the driver here, it tricks us into thinking this back up in yields is a positive

Sleight of hand - Magicians often manipulate objects using quick & skillful hand movements. I think Derek used this a lot but I still don't know how a card got in the kids shoe

For the 10 yr Treasury mkt, I would suggest that sleight of hand is related to who is selling (or not buying) the bonds that are issued. The Fed did some when it allowed banks to get par for bonds marked down. Other sleight of hand are the Chinese or Japanese Treasury bond holdings. Whether they are going down a lot or a little, they aren't buying as they did before

Implying false assumptions - Magicians can subtly influence the audience to make choices that appear free but are actually predetermined by the magician. I think Derek used this quite a bit

On this front, I would suggest this might be akin to the inflation expectations discussion. We can look at mkt based measures which look tempered. We can hear the economists & Fed discuss how inflation is falling while consumers know more of their money is still going to food & energy

Stooges or Assistants - Sometimes, magicians use assistants who are in on the secret & play a role in the trick. Derek only called up students from the audience so I don't think this was going on

For this we have Congress. I don't think anyone disagrees Congress is full of stooges. Well, these stooges might take us to the brink of a debt crisis that could be real this time because there is no leadership to come up with a deal

It isn't all trickery that is moving the 10yr to where it is. However, I think it elicits the same wide range of emotions for investors that Derek got from the audience. By the way, if you have a chance, see his show

(Editor’s note, if this were a stock, we would all trip over ourselves to buy it. Look at that chart!)

Margin of safety

A friend on LinkedIn said to me “You seem to still be pretty bearish.” My response “I don't know if I am bearish as much as I would say 1. there are a lot of risks in the world 2. there is no margin of safety in the stock mkt to compensate for these risks.”

I have spoken about the risks above. Wha about the margin of safety in investments. For this I am going back to a chart I have shown many times this year. It compares 3-month money market yields with the earnings yield on the SPX and NDX (the inverse of P/E). We can see that the earnings yields are below the money market yields right now. For the SPX, this is the first time since the Tech Bubble in 99. For the NDX, it is the second times since the tech bubble with the other being 2006-7. Neither of those times ended well. Of course, as we know, this can persist for some period of time. However, it is clear there is very little margin of safety. If risks are rising, is there any reward to holding stocks? Or is cash at 5%+ a ‘no-brainer’ as they say?

Finally, I want to leave you with one last post from LinkedIn, where I looked at the Japanese market. Always looking for places that can 1. give me information about my own market 2. provide me a diversifying investment.

Risk or Reward?

Chart of the Day - Japan House

It was a beautiful fall day yesterday so my wife and I decided to take a long walk thru the Arboretum on campus. It was the perfect day to capture the changing colors of the autumn

As we strolled thru, we came upon the Japan House in the Arboretum. The House goes back to the 1960s when Shozo Sato began to show a series of art & culture from Japan as a way to bridge the gap between the two countries.

In 1998 it moved to its current location under the direction of Kimiko Gunji who was one of my professors.

Bringing back these memories of Japan (I started my love of Japan in high school when I visited & stayed with a family), I started to think about the investment landscape & how the story may be changing there for the first time in my professional career

When I first went there in the mid 80s, it was the peak of the Japanese bubble. The mkt was roaring & Tokyo was the center of everything happening from corporate strategy to culture to food. The dollar went a long way in Japan

Then came the Plaza Accords in 1985 when the G7 decided to have a currency adjustment, which largely meant strengthen the Yen against the developed West as it thought the only advantage Japan had was a weak ccy allowing it to take market share in exports. This was an advantage but far from the only advantage, yet the top of the mkt came in 1989.

The chart today shows some of this dynamic. The orange line is the USD/JPY and blue line is Topix, the stock index with Toyota, Honda & Sony but also the big banks & insurance companies

In my view there are 2 things that have driven the index. Currency for sure given the major exporters that are in the index. But also interest rates and the impact on the financials. From 1990 until 2012 the currency was strengthening & interest rates moving lower hurting both sectors

Prime Minister Abe's Three Arrows reform was a catalyst in 2014 which helped give stocks a boost, but it was the weakening of the Yen that also aided exporters. With rates low, the fincls couldn't help out & the index lagged global peers

Then came the inflation post 2021 which other central banks have fought. Japan has welcomed this inflation as a way to break the consumer of the deflationary impulse. The white line has had fits & starts but seems to be on a trend now

Higher inflation has meant higher rates which has helped fincls. Higher inflation has meant a weaker ccy as there are fears the govt is losing control of inflation (see my posts on debt monetization). For now, both are serving to help stocks which are at 30 yr highs, but still not back to 1985

Japan is the poster child for western govts that have too much debt. If Japan can find a way to navigate out, it gives a roadmap for the others. QE started here after all. So did balance sheet recessions. If it can't, it will be the road map for what other countries are facing. We should root for Japan

Stay Vigilant