Tasting notes

A quick look through some interesting charts in between stops at wineries

I am celebrating a birthday and Father’s Day this long weekend in Napa Valley. I don’t have the time to organize my thoughts as per usual, but given I wake up earlier than the rest of the family, I always have some time to go through charts of what has been happening in the past week. This is my stream of consciousness thoughts on what I am seeing. I hope it isn’t too distracting. Enjoy!

For me the single best short-term indicator of risk taking is the moving average of the put-call ratio. You can see the plot here between the inverse of the put-call and the SPX. Until the put-call turns, the risk-taking appetite will still be on. This is the number one thing I am watching right now.

The single best economic indicator for me is jobless claims. It comes out weekly. It is not subject to the adjustments (birth-death ratio anyone) or revisions (three months worth!) of the non-farm payroll. It has been very strong for over a year. The risk per most economists is if it ticks above 250k. It has for the past two weeks. I show it here vs. the relative performance of bonds to stocks. With jobs getting worse, bonds should begin to outperform stocks.

I show the same thing here over a longer period of time. Covid messes up the series but you can see there is a really good fit to this. Worth paying attention to.

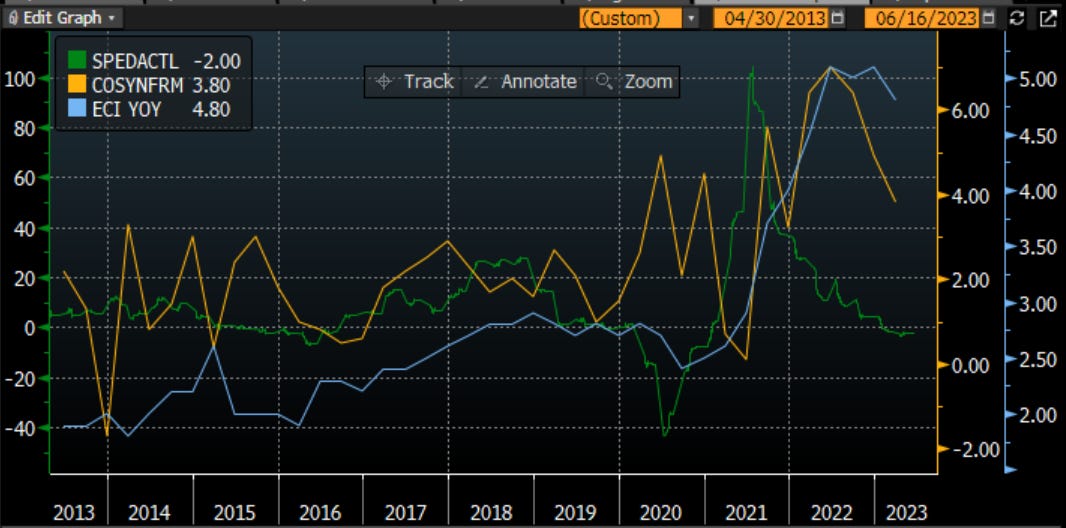

It makes some sense that as companies begin to earn less, they will want to pay less. I plot the actual S&P earnings vs. two different measures of wages. Wages have started to slow with earnings falling. We still see the unions pushing for higher wages. This can only hurt company profits.

H.O.P.E I have told you about housing → orders → profits → employment before. We haven’t yet seen employment weaken. Now some are pointing to housing getting stronger. I think this is a false start personally. New home sales are doing well. Existing home sales which are usually 85% of sales are dying. People are stuck in their mortgage. I wouldn’t read this positively as some are.

Another great global economic indicator is the ratio of copper to gold. It is signaling to us that there is a global slowdown occurring. We should expect bond yields to move lower. They are not now perhaps on fears of Treasury issuance. This is a big disconnect that should come together here at some point (see bond vs. stock performance)

Another thing holding the yields on 10 year higher is the move in USD vs JPY. The Fed is still hawkish but the BOJ is still dovish. Thus the dollar is strengthening vs. the yen.

Looking at the relative rotation graph, we can see that some early risk-taking leaders such as crypto, have moved into the weakening bucket. However, things like QQQ are still strong. We have seen the short-interest basket move solidly into improving suggesting that may be driving the moves right now. I think the health of the market is weakening

QT has started again albeit quietly. SPX and Fed balance sheet have moved together whether we want to admit it or not.

In fact, global stocks have moved with the Big 4 central bank balance sheets which are also rolling over.

Money supply at the big 4 locations (US, EU, Japan, China) has plummeted. Stocks have ignored.

If we break down who is doing what, the Chinese central bank is the only one trying to grow its balance sheet. This signals to me that it is not seeing its economy take off after Covid.

The stimulus we are getting from D.C. right now is all on the fiscal side which we can see in blue. Will Biden keep his foot to the gas through the election? Can we issue that much debt?

Risk across assets moves together. I said 6 months ago that this would get back together. We see Bonds and FX reducing their risk profile to match equities and credit. This is powerful for risk

Looking at the chart I highlighted before to say the NDX should roll over has proven to be a bad signal. I admit I was wrong on this one. Of course, we are now even more overbought so I think there is danger still. However, the relentless move higher in tech is beyond impressive.

We are now very overbought in SPX too. We can stay overbought in new bull markets. I just don’t think we are at the start of a new bull market.

Within stocks, what is working? Basically just growth. Traders prefer growth when growth is scarce. This is being driven by the mega cap names that are stealing growth from the smaller firms. Look how badly low volatility names are doing, or quality names, or dividend yield. The market does not want high quality. It wants to few names that are winning and nothing else. It is a long Magnificent 7 and short S&P futures type of market.

You can tell as I go through this that I am still leaning negatively. I recognize the technical drivers of risk-taking. I don’t want to take the other side as long as I see put-call moving and as long as I see the rotation into the same sources of risk driving the bus. It is a market that some are enjoying and most are lagging. However, it is also a market where you can earn 5% annually to sit and watch. I am still taking that boat but I recognize that causes the loss of some credibility at some time. I will worry about that another time. For now, I am going to another wine-tasting and enjoying my weekend.

Stay Vigilant

This could be the week in which bears claw back the narrative. Of course, that is highly uncertain, but at least the set-up position seems to favour the bears. One thing on the economy is a greater appreciation for the notion that the support from fiscal policy as heretofore been underestimated if one simply looks at the federal balance sheet. The ex-Dallas Fed dude, Kaplan was saying that a lot of the fiscal firepower is largely unspent, rests at the state level, but these states face a use or lose it by end of 2023 or 2024. Along with no obvious center for chaotic unwind of leverage positions that would trigger systemic risk, there is a degree of confidence that hiccups would be small. I would not be complacent on this or think this. I do not see where the leverage is but it does tend to make itself known after the party stops. Anyway, I am on board for a sharp sell-off to begin this week (I hope) and a more positive outlook for bonds---I almost feel as if I am channelling David Rosenberg...