Thanksgiving

Regardless of how your year has gone in the markets, there is something to give thanks for

We are going into a holiday-shortened week in the US, as we celebrate the Thanksgiving holiday. If you ask many Americans, this is perhaps their favorite holiday. It is all about family and friends, food and football. It is about relaxing and recharging ahead of the year-end rush.

We celebrate the history of the US. In 1621, the Plymouth colonists from England and the Wampanoag people shared an autumn harvest feast that is acknowledged as one of the first Thanksgiving celebrations in the colonies. This was a time when people could have been driven apart, but they found the reason to come together and share in a bountiful harvest.

The official holiday began during the US Civil War, a time when people were very much driven apart. President Abraham Lincoln made what had been an unofficial day of gathering to give thanks, an official national holiday. The goal was to bring people together to be thankful for what they had, even if times were tremendously difficult.

2023 is another year where people could be driven apart. In fact, many are. However, I think this time of year is one where we need to find the way to come together and give thanks for the blessings we have.

The message today at church was about sharing in the gift we have been given and if we do, we will be blessed with even more gifts, so that we can share those as well. As I heard that message, I thought of my two-year journey in Stay Vigilant. It actually began before that in my LinkedIn posts, and the goal in both was to share in what I had the good fortune to learn throughout my 30+ year career, across several continents and every asset class. My hope was to demystify finance or demystifinance.

True to the message at church, the more I have given of these thoughts and ideas, the more opportunities I have been given to participate in webinars, podcasts, workshops and live events. In each and every one, I have had the same goal: share what I have learned with the hopes of helping others. I get enough feedback and encouragement that I will continue to do so.

I don’t do it looking for thanks. The thanks come from being invited back. It comes from the readers of my posts and the comments I receive. That is how I know I am not wasting my time. However, like I said last week, I do not ask for any money. Some have pledged. Others know we are approaching Giving Tuesday. Either way, if you are inspired, my charity of choice is the Evans Scholars Foundation. You can donate at this link: WGA Evans Scholars donation. I just ask that in the message box you write “Stay Vigilant”. I can then find out what the readers have given and match it myself.

Given the holiday in the US this week, I will not be writing next weekend so this missive will serve for two weeks. As a result, I revert back to my format of looking at the Fundamental trend, the Behavioral flows and actions, and the Catalysts that will change people’s minds. I hope you enjoy.

FUNDAMENTAL

My theme this week on LinkedIn focused on the fundamental trend. There were a few posts and I started to see what I thought was a pattern emerging.

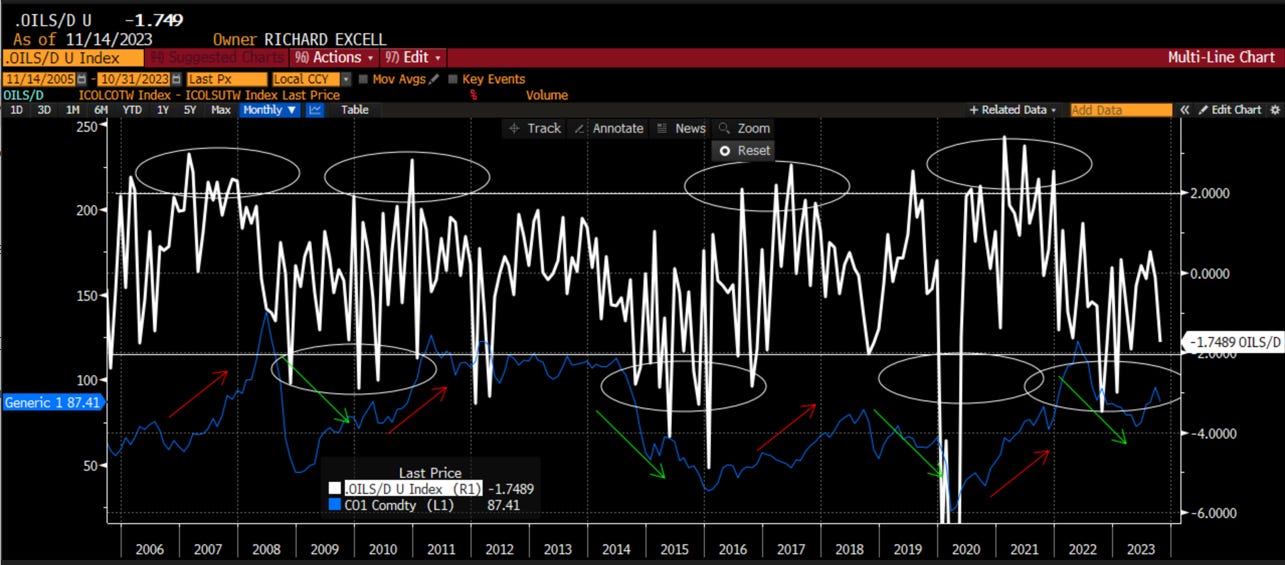

Chart of the Day - oil supply & demand

One market that I have found quite interesting of late is the oil market. There was quite a bit of discussion about the cutback in supply & what that could mean for prices & inflation. The inflation print today may suggest that this is no longer a concern

The argument given is that collapsing demand is forecasting a recession. One doesn't necessarily see that in the headline stock indices that continue to march back to the highs. You might if you looked at small cap stocks still languishing though

Is demand really falling ahead of a recession? The good thing is the IEA gives us the global supply & demand numbers so we can sort through what is happening. I have found whenever one exceeds the other by 2%, price is indeed affected

When demand is +2% as you see in the circles, prices move higher. Conversely, when demand is -2% as you see in the lower circles, prices fall. Currently we aren't quite at -2% but are getting close enough. There is something to this falling demand story

What might it look like going forward though? This is where I think it gets more interesting. Of course, this demand could continue to fall if a global recession happens. That may be what the mkt is currently suggesting

However, we have seen a number of other developments that may foreshadow more demand for oil than we previously thought

For those not paying attention, all of the major offshore wind providers - Vestas, Orsted & Siemens - have struggled mightily this year as projects are stopped do to cost overruns. Siemens even had to ask the German govt for support. If we aren't getting this energy from offshore wind, where will it come from?

Recently we have seen Plug Power, once a Wall St darling & the biggest mkt cap in the clean energy etf, collapse in price. This firm that generates power from hydrogen, cant do so in an economical way & now it may no longer be a going concern

More concerning for me was NuScale which makes small module reactor nukes. I am a big believer in nuclear power &, while not long SMR, was very keen to see it succeed. However, it also is facing cost overruns & can't deliver power cheaply

Another victim of higher cost of capital making projects too expensive to deliver cheaper energy is Solar Edge. It is also falling considerably down 75% this year

If offshore wind, hydrogen, solar & nuclear can't deliver power cheaply, what source of energy possibly can do so? Maybe there will be latent demand for energy after all

Perhaps this is why the Biden Administration has started to re-fill the SPR in the past weeks. Maybe it realizes it can't hold out any longer

Another interpretation would be that demand for energy is falling that precipitously across all forms of energy that we are already in a recession. If that is the case, why are stocks moving back to the all-time highs?

Many cross currents in the mkt now. Best to ...

Stay Vigilant

Chart of the Day - trucking

On my drive home from Champaign last night, I got to the final stretch, the final highway & traffic ground to a halt. It ended up there was a rolled semi up ahead. My thoughts go out to the driver & their family as it didn't look good. Everyone shut their engine off & we sat for 90 minutes

This same thing happened to me 2 weeks ago on the way home on the other highway. That time, another rolled semi & we sat on the highway for 2 hrs with the engines off

The 1st things that come to mind: 1. there are a ton of trucks on the highways 2. many people drive like idiots around trucks & most assume these massive vehicles have the same handling & stopping power, which they don't, thus these bad accidents

As I sat, I thought to myself that I hadn't looked at the trucking data lately. There are a lot of trucks on the roads but how does this compare to expectations. My post yesterday was looking at oil demand & I would be remiss to think about that without thinking of the big user of diesel

In today's chart I bring up in blue the truck utilization index put out by FTR. They also put out a trucking conditions index forecast in white. I plot both vs the ISM data in orange. As I mentioned yesterday, the energy mkts are pricing in a recession & slowing demand globally

If that is the case in the US, it better happen soon. You can see the trucking utilization has fallen rapidly this year consistent with the fall in the ISM. The trucking conditions index is also falling

Most interesting to me is the forecast on the trucking conditions index, which you can see on the tail on the white line. It is looking at the next 2 yrs from where we are & sees much brighter times ahead. This would be consistent with the soft landing many are forecasting right now.

I don't know if the forecasts are accurate but FTR Associates is a reliable source for transport info. Their index tracks the deviation from trend in 15 different metrics that represent 5 major conditions in the U.S. truck mkt. They see good things ahead

The major conditions are: volumes, active capacity utilization, fuel, cost of capital, bankruptcies. The index tracks level, rate of change & expectations for each major condition.

The 15 individual metrics are combined into a single weighted average index that tracks the market conditions that influence fleet behavior. A positive score represents good, optimistic conditions; a negative score represents bad, pessimistic conditions.

This index is suggesting the equity mkt is correct & we see a soft landing ahead. What does that mean for the path of rates then? What does that mean for energy demand? Will the rest of the world slow that much to offset a better US?

There are disconnects in the pricing of mkts & it is our job to figure out how to sort thru those & determine what the best trade is

Chart of the Day - regulation

I was at an alumni event where we celebrated the success of our students from Gies College of Business - University of Illinois Urbana-Champaign -UIUC Investment Management Academy & Investment Banking Academy. These are the best of the best & they showed it last night

In speaking about the amazing careers & early success they have had, a common theme seemed to come up - private equity & private credit. This is definitely the place for the top talent in the country to be heading right now

It was interesting to me, then, on my ride down to see 2 podcasts at the top of the stack, both of which were focused on private equity. The 1st was Freakonomics asking if private equity is ruining the US & the 2nd was OddLots speaking with Lina Khan about private equity

Freakonomics focused on a book called "Plunder" written by Brendan Ballou who is Special Counsel at the Dept of Justice. While the views are his own, I think the book's title belies his view of the effects of private equity in the US

The interview with Lina Khan, the Chairwoman of the FTC, was equally interesting. She spoke about the suits the FTC has filed against many private equity firms, with a particular emphasis on the roll-ups being done & looking at it more from a big picture, than deal by deal basis

Both podcasts seemed particularly focused on the healthcare industry - assisted living, hospitals, doctors practices, PBMs, anesthesiology etc. Both presented the actions of private equity & implications for consumers & employees in a negative light

This made me think that as we enter an election year, with healthcare a particular interest to the large voting bloc of retired Boomers, that this could be something to pay attention to

Then in my email I came across two articles from S&P Cap IQ - the 1st was about the sentiment of private equity's Big 4 sinking to the lowest in over 5 quarters & the 2nd that short sellers have boosted their bets against the healthcare industry

You ever have one of those days where you seem to come across a lot of information that is directing your attention to the same thing? You ever wonder what to do with it? That is the last 12 hours for me

The chart today is from George Washington Univ looking at executive actions that are considered economically significant i.e. will have an impact on the economy of $100mm or more

We can see that other than the dip in 2017-2018, these have all trended higher over the last 40 years. If you had to guess, will that number be higher or lower next year? What will the impact on the stocks affected be?

Don't count me among the haters of private mkts. I think they provide not only great returns to investors, but a useful purpose in keeping the crown jewel of the US - our fincl mkts - efficient & lubricated with capital

However, in any mkt we can find flaws or problems. Seems like this may be under the microscope for now

Chart of the Day - HOPE

There has been a lot of economic data this week. The highlight for many was probably the CPI data on Tuesday where the 0% month over month print had all mkts excited. All Fed hikes are priced out now & the cuts priced in get bigger w/ almost a full cut by May and more than one cut by June

This has led to a large rally in duration assets with 10yr yields down to 4.4% & the high yield mkt moving to levels not seen since the summer. The junkiest of equity names with no profits or cash flow have led a massive move higher in stocks this week as a result too

Of course, this all feeds into the Santa rally narrative & with a shortened holiday week next week combined with a desire for portfolio managers to increase their bonus, the pressure for a move higher into the Dec 13 FOMC mtg is palpable

Leaving aside that core CPI year over year is still 4% which is double what Jay Powell wants, there may have been other news this week that should give traders & investors some pause as they re-assess positions into early December

The data I think was most important was the NAHB Housing Market Index data which came out yesterday. It plummeted to 34 which is Covid era lows. You can see this in white in the chart today & I think we should all take note

I have discussed before how housing leads the economy out of & into recessions. In fact, it was the very strong NAHB in December of last year that set the tone for the soft landing discussion & strong mkt this year. You can see it led the other data

The other data is the ISM New Orders in green, the S&P quarterly profits in pink & the household survey jobs data (yoy) in blue. The household survey data is better than Non-farms payroll or unemployment because it leads at inflection points

You can see early this year after housing bounced sharply, new orders picked up & then profits began to improve & the labor mkt got a bounce. It is the last to move so it is still holding strong. This Housing (H), new orders (O), profits (P) & employment (E) flow indicated the economy would be better

I didn't pay enough attention early this year even though I should know better. It is important we learn from our mistakes & I am taking notice now

It is not surprising to see NAHB number drop because also out was the housing affordability index which fell to 93.40, the lowest point I can find going back to 1986 when the data on Bloomberg start. That is, housing has never been less affordable

The mkt hope is that the Fed is cutting rates which will boost things like the housing mkt. However, with 4% core yoy CPI perhaps the Dec 13 FOMC could disappoint the mkt if it hears higher for longer & hawkish pause

The real HOPE is that housing is falling & we should expect new orders, profits & employment to follow suit. Maybe this is the demand slowdown we are seeing across the different forms of energy that I spoke about earlier this week

Looking at this in aggregate, I come away downbeat on the economy as we go into the new year. Sure, the trucking outlook looks pretty good. We should not dismiss this. That said, the HOPE paradigm I find extremely important. The housing data was very poor this week and we KNOW that leads us into and out of inflection points in the economy. If we layer on top of this the heightened regulation that we are seeing across the economy, as well as the falling demand in the energy markets - whether oil, nuclear, solar or wind - and I can do nothing but be a little cautious as I look out for the next 2-3 quarters for the economy.

BEHAVIORAL

For the better part of 2023, even when the fundamentals of the economy, of central banks, of the banking system, looked negative, it was the behavioral or technical parts of the market that held everything together. Thus, I would be remiss not to consider this. In fact, in a project I am working on with students, the results of which I will reveal toward the end of the year, it is the behavioral aspects of the market, and not the fundamentals, that matter in the short-term. This is not surprising, as for one we know that things like valuation have no significant impact on investment performance in the short-run, but are the most important in the long-run.

I will therefore look through a few behavioral patterns to try and assess where the supply & demand tendencies of the market may lie.

The seasonal tendencies for the market are very real:

October and November tend to be very strong months for risk-taking in spite of some historically bad Octobers. While this past October continued the stumbles of August and September, the price action in November has wiped it all out and we are back near the highs for risk-taking. Portfolio managers will try to ride this higher in order to maximize bonuses this year. As Bully Ray Valentine would say in “Trading Places”, they want the G.I. Joe with the kung-fu grip.

If we layer onto this seasonal tendency, the price action from this week, we can see that there were quite a few technical drivers for performance. It was clear that traders and levered funds were short both stocks and bonds into the CPI number. The 0.0% month over month number caused a scramble in de-risking this week, ahead of a holiday-shortened week coming up. We see the sharp move higher in the Goldman Sach most-short index in blue, up over 8% this week. The Russell 20000 small cap stocks in orange were up over 5%. These are the most risky names that have lagged massively this year. The white line is the managed futures fund which was short both stocks and bonds ahead of CPI and we can see the negative performance. Finally, the QYLD and RYLD buywrite etfs and to buy the market through Thursday and then turned around and sold calls on Friday to re-establish the position. All of these drove risk higher this week.

My favorite short-term indicator is the 20 day moving average of put volume vs. call volume. When it heads lower, it means investors are not seeking insurance but seeking upside exposure. This is positive for risk. This is what we see right now.

Looking out to the medium term, however, I assess the ratio of copper to gold as this is the commodity market measure of economic growth relative to the safe-haven commodity asset. It has a tendency to lead the growth of the economy. This metric is telling us to be wary of a good-sized slowdown in the economy. This is consistent with the negative view we see from the energy complex.

Another potential source of risk is occurring in Japan, a country that is a capital exporter to the rest of the globe. As the Yen weakens (USD vs. JPY move higher on this graph), the tendency for Japanese investors will be to re-patriate savings. This will start to starve the rest of the world of necessary capital. No place may feel this more than the US, which plans to issue billions of dollars of Treasuries in the first quarter. Will we see much higher yields in Q1 in spite of a potentially slowing economy? This is my fear. This is the return to the 1970s.

I will end on a more upbeat note. The broader US stock market broke above the trendline and is set to move back to the highs, if not higher, in the coming days and weeks. While there may be trouble as we look into Q1, much of the short-term signs point to higher prices for now.

CATALYST

The final category I always consider is the catalyst section. What can happen that will get traders to change their minds. At this point I can only think of two things: more and more negative geopolitical headlines and the December Federal Reserve meeting.

On the former, I know that the lack of escalation across the Middle East since the October 7 has many people feeling more comfortable. I sense that this may be the calm before the storm. The US has been stepping up its attack of Iranian proxy targets across the region in the past two weeks. This coming week there are several countries going to China to discuss the Israel/Hamas war. While many feel this is a chance for a peace deal, this may be overly optimistic. I will leave it to the experts that show us that geopolitical risk is breaking back higher and heading to the highs we saw when Russia attacked the Ukraine.

On the plus side, the APEC summit in San Francisco appeared to put the US and China back on track to more productive conversations, after several years of more difficult discourse. While this is surely a positive, the actual hot wars occurring in the world still have me a bit more worried than the usual person.

Finally, the next big negative potential catalyst for me is the December FOMC meeting. We can see from the chart below that the market expects no more hikes and cuts to start next year. After all, the Fed usually cuts 6-9 months after it pauses, or so the narrative goes. However, history shows us that the fed cuts 6-9 months after it pauses because we are in a recession. This has happened every time except the mid 1990s. The only reason that was different was because we had the Asian Financial Crisis which caused the Fed to cut. My concern for this meeting is that traders will be leaning very long because of the positive seasonals and technicals, fully expecting nothing out of the Fed. Any hint that the Fed could still consider hiking, or any further mention of higher for longer i.e. no cuts, could get some people caught leaning the wrong way. Something to beware of in a few weeks.

In summary, I believe the fundamentals are still negative, the behavioral aspect is positive for the next month or so, but the catalysts, if anything, shade negative. I feel like this is still a time to be cautious but try to participate in the positive tendency for moves higher. If we look at the price of insurance in the equity market, as measured by the VIX market, it is heading back to the lows of the year. Thus, one can express long risky asset views with optionality, which embeds the protection that one needs for any surprises in the coming weeks.

I will check back in with you in early December. Until then …

Stay Vigilant