That's a wrap ... or is it a taco?

Heading home after a great trip in Europe

This week we ended our two-week trip through Europe, visiting companies and seeing sights. We also introduced students to, perhaps, different ways of thinking about the investing industry, different priorities in investment products and different investing attitudes. Finally, we got to experience new cultures and gain a greater perspective of what is really happening in Europe, and what Europeans really think about the US.

As they say in show business, that’s a wrap.

One major takeaway for me is how ultra-focused everyone, I mean everyone, is on the Trump tariffs. Whether they will work or not work, whether they are illegal or not illegal, the apple cart has already been upset. Companies want to reduce exposure to the US, even though it can’t go to zero with the US such a large weight in indexes. Consumers are less inclined to travel to the US. Students are less inclined to study abroad in the US. On the last point, because students aren’t, or can’t, study in the US, that means fewer US students will go to Europe given the exchange requirements. All of this is a net negative in my opinion. Less interaction only creates more problems and more enemies.

Thus, it was interesting to see all of the headlines of tariffs being pushed out and of one panel of judges saying they were illegal. It seemed these tariffs were always destined for the Supreme Court anyway, now it may be fast-tracked.

It was even more interesting when the students were talking about the WSJ reporting asking Trump about the ‘taco Trump’ meme. You know, the one that says “Trump Always Chickens Out”. So, maybe instead of a wrap, we have a taco after this week in Europe.

From an investing standpoint, I think the taco Trump meme only creates more uncertainty and not less. He is likely to be more stubborn, less willing to extend, and more demanding in his terms because his ego has been bruised. The US market didn’t seem to agree with me. Sure, NVDA earnings were good, as were the market’s overall, however, the macro could have mattered. it didn’t really.

I feel aligned with the views of Reva Gujon, someone I have interviewed in a Stay Vigilant podcast before. This is what Reva said about tariffs:

More whiplash today from Trump tariff rulings after the Court of International Trade ruled that Trump's IEEPA-based reciprocal tariffs and fentanyl/border security tariffs are out of bounds. The Court of Appeals for the Federal Circuit then swiftly issued a temporary stay on those tariffs while the Trump admin's appeal is under review. Hand-wringing and sighs of relief on all sides of this tariff debate. What comes next?

Delay tactics: Even as the IEEPA tariffs remain in place for now, questions over their staying power and the credibility of the July 9 deadline for deal-making will slow negotiating momentum. Much harder now for Trump to fire off midnight tariffs on Truth Social with his most potent tariff tool in legal limbo.

Rolling with the punches: The Trump admin will take the 'nothing to see here' approach in pushing ahead with negotiations as if nothing has happened. But if it's worried about the appeal outcome, it could also explore additional tools in trying to maintain leverage with trading partners. Section 232s are still stacking up. There are active 301 cases on China and on countries that impose DSTs. Section 122 of the Trade Act of 1974 could be used to impose across-board tariffs up to 15% but would expire after 150 days without Congressional approval (opening the door potentially to Congress reasserting oversight powers on tariff policy.) Section 338 of the Tariff Act of 1930 is untested but is more in scope with trade reciprocity arguments and could impose up to 50% across-board tariffs over trade discrimination.

Mixed results for trading partners. Japan has a decent shot at a grand bargain in this window of vulnerability for the Trump admin. EU still facing a rocky road ahead over sectoral tariffs and non-tariff barriers. MX and CAN get to breathe a bit easier while trying to shift attention to USMCA-level negotiations.

And if the admin loses the appeal... watch out. In addition to the trade toolkit, the Trump admin can hunt for leverage in other places. Besides 301s over DSTs, Section 891 and the proposed Section 899 of Internal Revenue Code in the 1BBB could lead the US to weaponize the tax code and impose tax penalties on companies based in countries that impose "unfair foreign taxes". This would be a very ugly scenario leading to tit-for-tat tax retaliation that would stifle investment and undermine the admin's big onshoring goals. The admin can also apply long-arm leverage in export control enforcement to pressure partners.

Escalation ahead for China. The admin could also take a more constructive path of leveraging US market access to assert supply chain security standards (excluding Chinese participation in critical areas) and driving more partner convergence through trade deals. This is what Beijing will be most concerned about. The US is already ramping up tech controls. Beijing has its hand on the CRM trigger. And the Trump admin has more room to raise 301 tariffs on China...

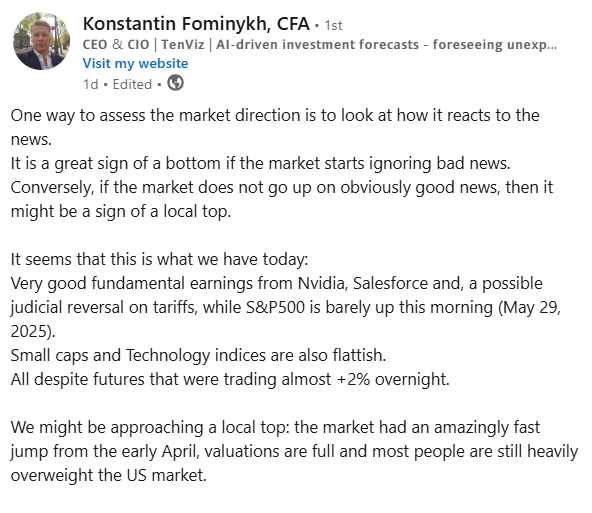

Whether the US market cares about this or not, may be the question. Are we back to pure idiosyncratic markets? Another former interviewee, had some thoughts on LinkedIn:

Konstantin sees the move this week a bit differently. He always has a different take as he was an early user of AI in trying to interpret the positioning and flows of the market. I find it interesting that he says people are still overweight the US market. It is not surprising given the magnitude of the positioning before, but in speaking with many savvy investors in Paris, Zurich and Vienna, I definitely get the sense they are looking for a reason to rebalance. Again, there are index constraints, but with valuations and catalysts as they are, this seems like an opportune time.

In fact after an amazing run from the lows in April, with the market basically unchanged for the year, you would be forgiven for thinking it was all a bad dream and you should still be involved. However, technically speaking, I would highlight a couple things on this chart that might give one pause near term. The first is the MACD crossing and starting to head lower. This suggests a change in trend may be afoot. Sure, we could go sideways instead of lower, but it might suggest the move straight up has stalled. The second is the RSI. As prices headed higher on the NVDA/tariff news, the RSI did not set a new high as well. This is called a negative divergence and is also a negative sign.

Maybe a better sign is the stalling in risk appetite. We had a couple interesting meetings that talked about crypto. In Zurich, we met with Bitcoin Suisse, one of the largest trading/custody/research firms on crypto. Swiss investors are interested in crypto and access the market through these guys. They were quite positive on crypto as you might think, however, I took a poll of the students after, and the company was not able to convince any of the students who weren’t already believers. Maybe those who own will HODL, but are there more to join?

A different meeting with a multi-asset team in Vienna talked about the lack of an equity culture, the lack of risk appetite, generally in Europe. Where we have 60-40, they have 40-60. Investors, corporate and individual, don’t feel the need to be active in equities. However, the ‘younger generation’ does like to trade crypto on their phone. So, perhaps, this balances out my students cold take, with a Millennial and Gen Z European crowd that is more keen. As I told my students, you can’t think of crypto through a US-centric perspective. You probably wouldn’t buy it.

However, Bitcoin itself is rolling over and as I have pointed out before, it can be a pretty good leading indicator of risk appetite in markets. This could also point to some downside in the NDX as we see above. I am more inclined, and not less inclined, to think of Bitcoin as a risk barometer after my meetings this week.

It isn’t just for NDX either. I compare Bitcoin to the stock vs. bond allocation ratio. This compares US stock and bond total returns. Bitcoin does a pretty good job of leading this index too.

Speaking of Bitcoin, X was on fire with Bitcoin content given the conference that went on this week. Lyn Alden spoke at the conference and there were various clips of her speech. It is worth going through and listening to them. It may seem a bit like more of the same, but the argument is that nothing is going to slow the fiscal spending train, which means governments are going to be expansive, inflation will head higher, fiat will be de-based and you want to own hard assets. She picked Bitcoin. When speaking to Bitcoin Suisse, they made similar points and in reality it is not just the US government, but UK and many EU governments as well. This definitely gets one bullish Bitcoin, but also gold and real estate.

However, this tweet and others like it point to a big bear story in crypto that used to be discussed and isn’t as much anymore. Quantum computing will be able to crack the encryption of crypto, putting everyone’s blockchain and net worth at risk. Quantum has been on the come for a long time, but appears to be close to a point of maybe breaking out. I know my own university is very active in this and the internal headlines suggest major advancements in quantum. Chicago and Illinois aim to be the center for quantum computing in the US, so maybe I am a bit biased, but this is something to watch if you are long crypto. For now, it is only a possible tail risk down the road.

Back to the fiscal expansion idea. This is a retweet of something Elon put out this week. The DOGE, the person tasked once with cutting fiscal spending, is getting on board with the growth of government trade. The ‘grow your way out of it’ is what politicians, especially the GOP, always resort to when they can’t cut spending or raise taxes. Scott Bessent has suggested it as well. Shouldn’t we care more about this changing mindset? If so, I agree with Andreas that shorting bonds is the right idea. What does that mean for stocks though?

For that, I point out an interesting post I read from Jurien Timmer, head of macro strategy at Fidelity:

At 88 bps, the term premium is well above the financial repression era lows of the past decade, but it remains well below levels that we might consider normal over the past 5 decades. My guess is that the term premium is on its way to 150 bps or so, which depending on what happens to inflation expectations could push the 10-year well above 5%. The stock market will not like that, and neither will the dollar.

Why does this matter? For two reasons. One, as the stocks/ bonds correlation chart shows below, the higher yields go the more correlated bonds tend to become to equities. The purple dots show the correlation of long-term Treasuries to the S&P 500 (going back to the 1930’s) and the black circles highlight the period since 2020. The Great Moderation Era of the 2000’s and 2010’s is likely over, and we are back to the more traditional era of the 1960’s-1990’s.

Two, the more correlated bonds are to equities, and the more competitive bond yields become to equity yields, the more impact those rising yields have in forcing equity valuations to correct. That’s at the heart of the Fed model, favored by the Maestro Alan Greenspan during the 1980’s. The model only works when rates are not being suppressed by central banks through zero interest rate policy (ZIRP) and Quantitative Easing (QE).

The bond vs equity valuations chart and the DCF grid both indicate that a return to 5% for the risk-free rate could force the equity P/E-multiple to drop 3-4 points from here. That would be a 15-20% haircut to price, before adjusting for the offset from earnings growth. That’s consistent with the trading range thesis.

Term premium matters as we discussed with the Greg Ip post last week. Rising term premium means rising yields. Rising yields mean lower equity valuations. While this does not mean the bottom has to drop out of stocks, it does mean that US stocks look challenging here. If US bonds are a short, are US stocks a safe place to be? Maybe those European investors will see this and want to move out of US stocks and into European stocks.

If we are talking about an expansionary government as a driver, it may be worth considering the relative growth of central bank balance sheets too. Remember when we used to care about that? Well, comparing the ECB balance sheet growth to the Fed balance sheet growth has been a decent indicator for relative US vs. EU equity performance. Is this another reason for a rotation out of the US and into EU?

Rising EU PMI’s are making the case for cyclical upside in Europe relative to the defensives. Can this continue? If so, the market there could continue its strong run despite the lack of an equity culture.

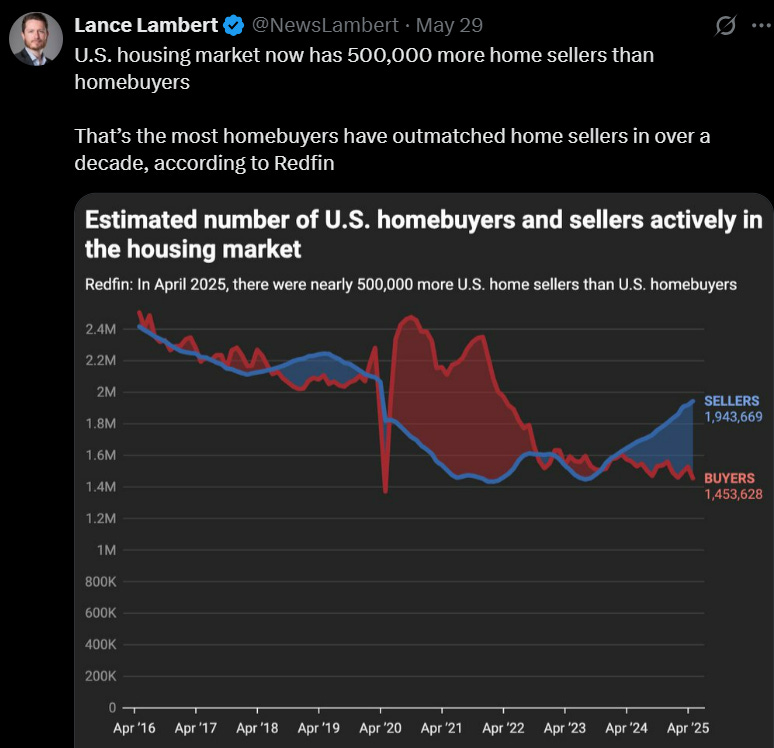

I talked about real assets before and for many that means housing. However, is the housing market looking strong? How is it doing? We are starting to get some unsettling news from the housing market, always an important leading indicator. The chart above from renowned macro strategist Francois Trahan shows the number of home sales per household has collapsed to levels that are worse than even during the Great Financial Crisis. This at a time when all we hear from DC is how great the economy is.

What is driving this slowdown? This chart above suggests that higher yields (which we may be seeing more of) is slowing down the number of buyers, and those who bought post Covid, perhaps for an investment purpose or for a second home, are turning net sellers. This paints a more downbeat view of the US housing market which is a big driver of equities.

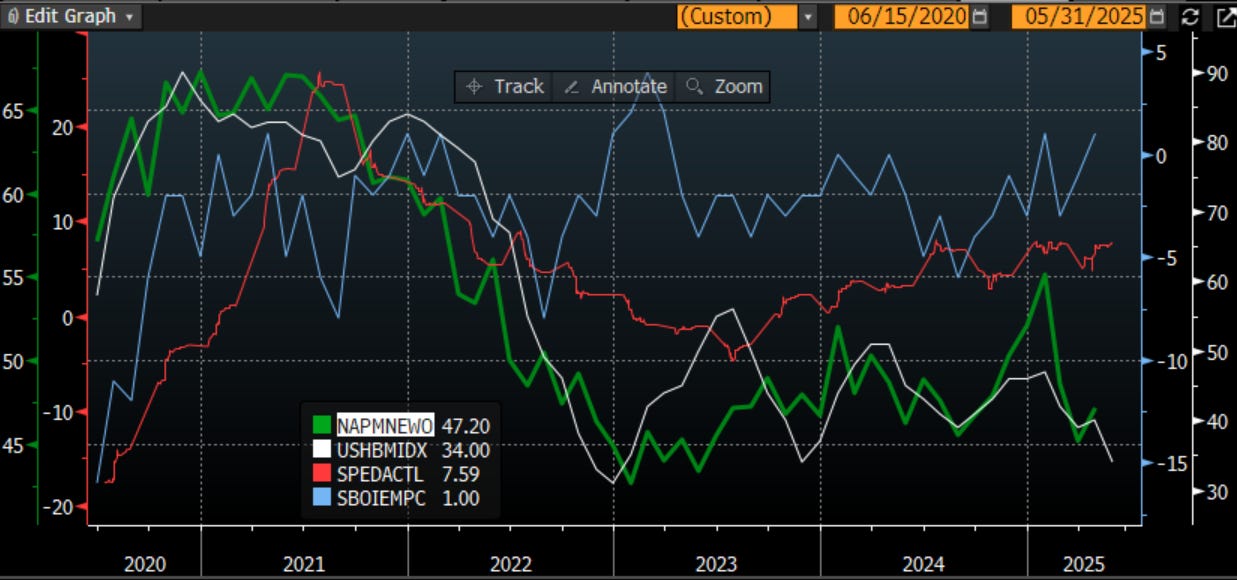

I have discussed H.O.P.E many times before. Housing leads the economy into and out of recession. If the housing market is looking weak, that is not a good sign. As you see above, the falling NAHB Real Estate index in white should lead new orders lower. These are the first two places we would see move. Only after that will we see earnings (in red) fall and then finally employment. The early indicators of H.O.P.E also point to downside in the economy and in stocks.

If new orders are heading lower, that likely means the new orders to inventory ratio is heading lower. It is a leading indicator of the US PMI, which itself is coincident with the stock market. However, in the last 9 months, stocks have outperformed what the economy would suggest. Here I look at the S&P 1500 and not just the Mag 7 biased SPX. This is a bad sign for the overall stock market. As much as people saying these ISM like indicators no longer matter, for the overall stock market, they sure do. Maybe for a handful of names, for now, they don’t. But for many investor portfolios they will. They certainly have for the small cap fund we run for the university.

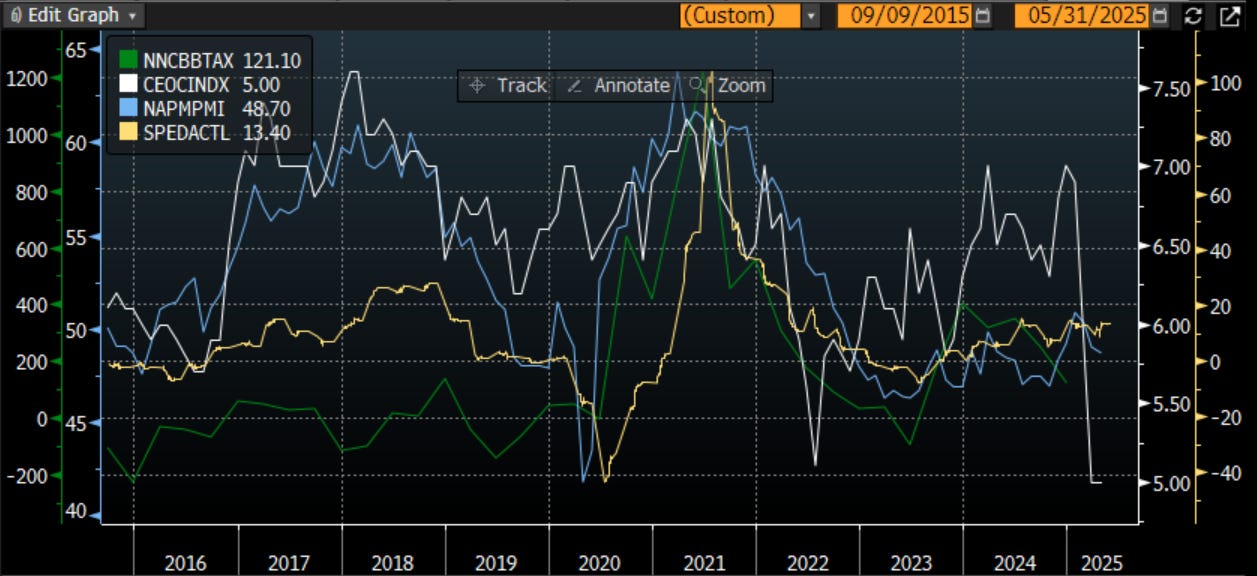

Maybe it is no wonder PMI’s will fall in the US because CEO confidence has plummeted. The other lines here are earnings, those reported to the government and those reported to the market. CEO confidence leads both. This is another yellow warning sign.

Coming back to the US after a two week trip, where I wasn’t watching every headline, every tweet, every move of the market, can be refreshing. It lends a new perspective. As I try to re-gain my market footing, the signs to me look cautious. There is reason to think that the bullish parts of the Trump program - DOGE, tax cuts and cuts to regulation - are being replaced with the negative parts of the Trump program - tariffs and strong pushback from the Establishment. It is also the case that the European buyer for US stocks may be leaning the other way, selling into the bid right now. If we add some possible weakness in bonds, it makes one wonder where they can turn. It may in fact be Bitcoin and gold as the only safe places to be right now. Maybe the US investor needs to develop that EU attitude of taking their risk exposure in crypto instead of stocks. That is a major cultural change for many.

For now, it is time to unpack, do some laundry and catch up on sleep. For now, that’s a wrap (or is it a taco?).

Stay Vigilant

Excellent commentary and analysis as usual!