The last of the three body problem - catalysts

The last of the three bodies in the three body problem is Catalysts.

As we build the view, it is important to know what the trend of the economy, and therefore the trend of the market is. It is important to know what is driving this trend at home and abroad, and how this impacts different parts of the market. In addition, one must ascertain the behavioral tendencies of the market, to determine where the supply & demand is. Price is the intersection of supply and demand, so discerning what is affecting either of these, is vitally important. However, in both of these cases, Newton's First Law the law of inertia, will hold. An object in motion will stay in motion unless acted upon by another force. This other force comes from catalysts.

There may be many catalysts that an investor should consider, but I have simplified this into three specific catalysts. Since last week's blog was so long, I wanted to give you a break. The three catalysts I will discuss are economic surprises, earnings surprises, and geopolitical risk.

First, economic surprises. Our friends at Citi have comprised economic surprise indices for more than 2 decades. These measures do not tell us about the trend of the economy and what is driving that. It does not tell us which economy is stronger than the other. However, importantly, it tells us how the economic data that arrives every day and every week of the year, is coming in relative to expectations. Markets move at the margin. Markets will, to some extent, price in the news that the consensus agrees upon. Thus is is only when the news comes in better or worse than expectations that prices will adjust. High absolute growth is good, but if it is not quite as good as everyone hoped, there will be a negative reaction. The fundamental category will capture the high absolute level, the catalysts catch the latter.

As I look around the world, I simplify into four areas: US, China, EU and EM. How are data relative to expectations? We can see two clear trends in my opinion. The first is that even in the midst of a strong economy in 2021, all of the regions consistently saw data come in lower than expectations throughout the year, perhaps presaging the slowdown the market is anticipating right now. I am probably giving people too much credit, howevre if the data is consistently good but not as good as hoped, it wears you down. On the one level, you ultimately lower your expectations. On this front, expectations have certainly been lowered and that is the other trend. All year long, in spite of negative headlines, the economic data has been better than expected. This has particularly been the case in China and you can see in blue, it has even spiked higher of late. Of the four regions, the US is doing the worst on a relative basis, and perhaps this is because expectations haven’t come down as much. However, from an ecomomic surprise standpoint, the markets are in a good place:

The next area is earnings surprises. With a hiking cycle starting it is reasonable to assume that mutiples for stocks will continue to compress from the extremely high levels seen at the end of 2020. This has been the trend and in the SPX, we have seen the forward P/E fall from over 21 to mid 17s. Arguably still high, but I think it is safe to say optimism has waned. Is this waning optimism justified?

A falling multiple doesn't spell doom for the overall market, however, it does mean that companies will need to continue to deliver on sales & earnings growth in order for their stocks to move higher. Not only growth but growth that is better than expected. Recall from above that markets move at the margin. In order for a stock to move higher not only must growth be high in absolute terms but also must be high relative to expectations.

The first chart shows how sales and earnings have come in relative to expectations. The numbers are all largely positive for the overall market and for each sector. In fact, the industrials sector is the only one that has seen a negative earnings surprise. I would draw your attention to the bottom of the picture. On the left is the level of surprise, sales and earnings, for each of the last several quarters. The trend is clear that there are diminishing marginal returns. We surprise, yes, but are doing so at a much slower rate. This rate is better than pre-Covid, and you recall we were about to go into recession even before Covid, but it is not nearly as good as it has been. On the bottom right of the chart is the stock reaction to the news. You can see here that it is very much a mixed bag. Even for the biggest earnings surprises, the one day change in the stocks is negative. Overall it is quite mixed, and so investors are not rushing to buy in. These are not positive developments.

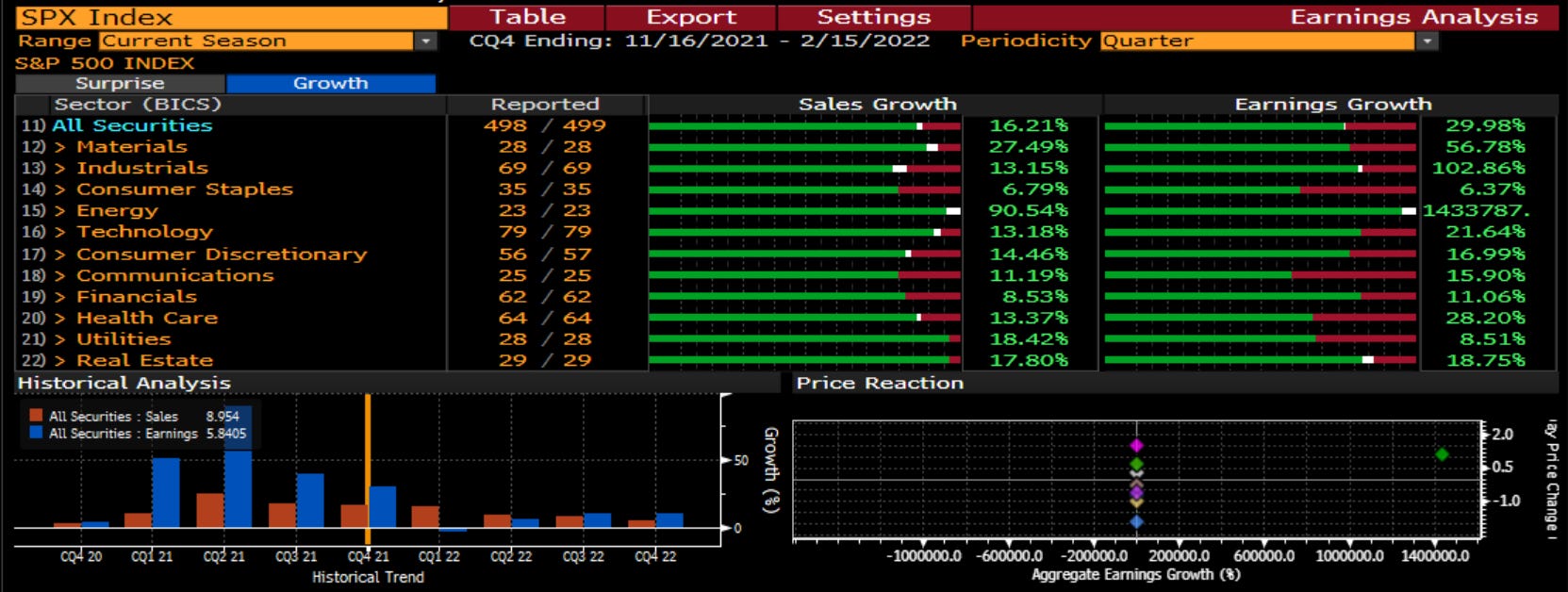

The second chart shows the absolute level of sales and earnings growth. You can see that with only a few exceptions, the sales and earnings growth were both double digit. Comparing this to the top chart, we can assess that the absolute level of news was pretty impressive, however, investors had already worked to price this in. Also, the highest growth was in the cyclical sectors such as Energy, Materials and Industrials. This is a very inflationary type of environment and not the stagflationary mindset that has become consensus. Stocks can do well in inflation, when prices are going higher but growth is still good. Especially stocks with high fixed costs that have a lot of operating leverage, such as Energy, Materials and Industrials.

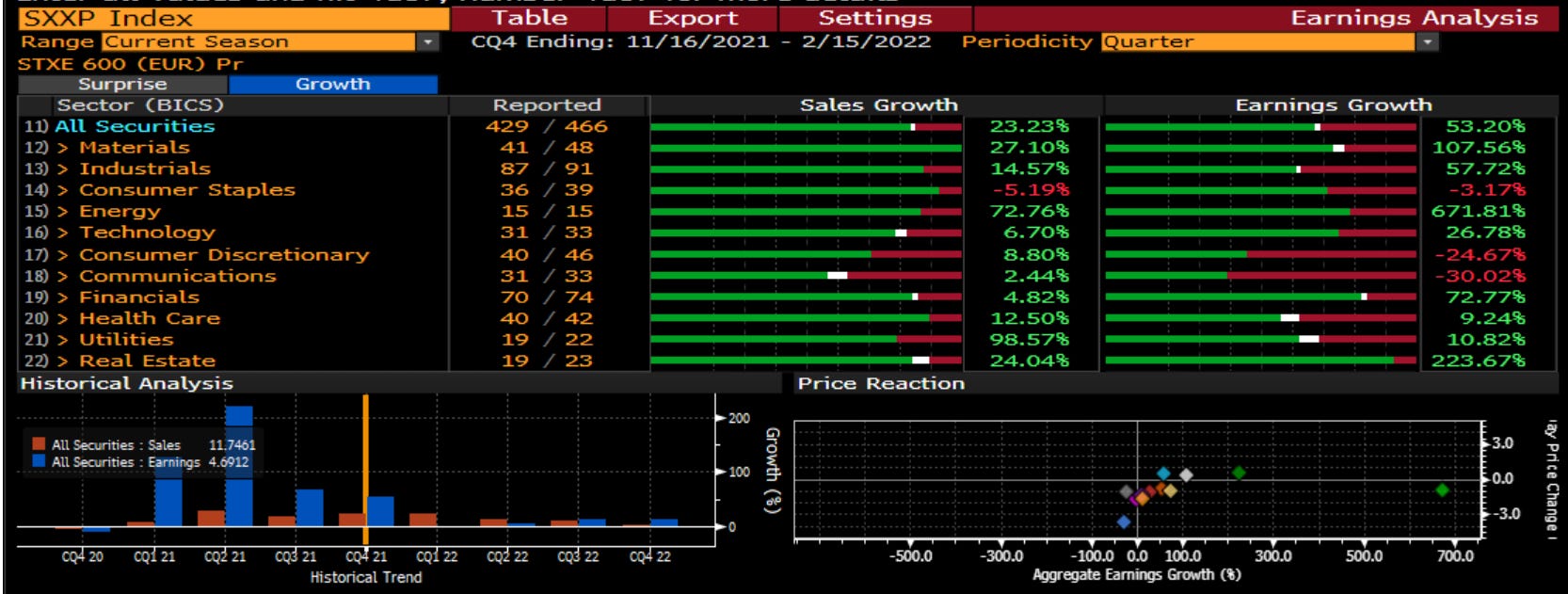

One last chart and that is the same analysis for Europe. Since the invasion of Ukraine, things have changed pretty materially so I do not want to draw too much into this. However, you can see a similar picture of very rapid sales and earnings growth, but where the surprises are coming in more and more in line and where the stocks are not reacting. So even before the bad news came into the market, the good news was already priced in.

Finally, I consider geopolitical risks. There is no way one can consider the current geopolitical risks in the market and not come out negative. Admittedly, this particular category is always either a negative or a neutral and never a positive for markets, outside of a period such as win the Wall came down and there was a multi-year peace dividend to the market. Right now, though, we are probably witnessing the exact opposite of the Wall coming down. We are witnessing not just an unprovoked attack on an innocent nation, but we are witnessing the beginning of a Second Cold War, and this will be one in which it is not just bi-polar between the Soviets and the West. This is one that will be multi-polar as China looks to assert its sphere of influence, Iran does the same, and Russia has already started. Will Turkey follow suit? What about in South America? The peace dividend that drove rates lower, multiples higher, margins stronger, and wealth to historic levels for the last 30 years looks like it is ending. This has major implications for all markets.

How do we pull it together? The economic data has been surprising on the upside across the world. While the trends in economies are worse, this means that so far countries have been able to hold on better than consensus thought. This is a mild positive. The earnings data suggests that any good news is being priced into stocks. This look was based on data from earlier this year, before the invasion as well. What will it look like in the next quarter? As we said, multiples will not be expanding, so can sales and earnings hold on and drive stocks higher? This could be difficult but we shall see beginning in April. Finally, the geopolitical risks are about as bad as I have seen in my 30+ years in the market. I am not one who is prone to hyperbole but this is a historic moment and a negative hsitoric moment at that. We might be looking at permanently lower margins, permanently lower mutliples, and therefore permanently lower returns going forward.

Stay Vigilant

Great analysis, gives one 3 things to think about in the overall picture.

great summary, thanks rich. i might suggest another weapon to put in your "earnings surprise" arsenal. CGERGLOB Index = Citi global earnings revision breadth (+/-) which can be a good indicator on the direction of earnings and earnings surprise momentum...long before companies actually report the news. similar to the citi economic surprise indices.

i would post the chart here...but substack hasn't figured that part out yet. -Mr B