The narratives that I see

Looking through some other Substack blogs as well as my own writings from this week yields some interesting insights

Agenda this week:

Recommend some other Substacks that I have found to be quite helpful;

Recap my posts from this week and the narrative I am following.

Before I do, if you like this Substack, please like, share and subscribe if you have not already. It really helps me understand what is resonating with and what is not resonating with people. I do these blogs to see how I can be helpful and where I can engage with others. If you have not subscribed, you can do so here:

Second, as I wrote in the last post, I am not doing this for any money. That is not my goal. However, there is a bit of work that goes into these. Many have pledged that they would, in fact, pay for a subscription. I am not going to ask for that. However, if you are so inclined, I would encourage you instead to donate to one of my favorite charities - The Evans Scholars Foundation. It is the largest privately funded scholarship in the USA, paying for tuition and room & board for deserving golf caddies. These high schoolers, who are in the top 20% of their class and whose families are in financial need in most cases would not be able to attend college without this. If you are inclined, please use this link and in the message box simply write Stay Vigilant. That way they can keep track and I can match the donations.

Now, on to the regularly scheduled program.

I wanted to highlight a few other Substack blog from people I follow that I think it may be worth it for you to as well. I appreciate that some are paid subscriptions, and this may not be appealing to you. However, what I find in Substack is that there is a large amount of high quality content being produced. There is much that I would have used when I was running institutional money, even if they were not prepared by ‘Wall Street’ analysts.

The first Substack I would recommend is Beachman’s Newsletter. I have recommended this before. Beachman has a very disciplined process for investing in growth stocks. With a background as a C-suite executive for a Fortune 100 company, he knows what metrics matter to management teams from technology companies. His process is much more than that but his perspective is well worth it. Interestingly, Beachman shorted the market this week, even though he has correctly called and ridden the market higher all year long.

The second is Investing in Financial History by Mark Higgins. I am relatively new to this blog as I was turned on by a friend. Mark does not write often but when he does, it is interesting. The views are being compiled into a book that will come out in February where Mark looks at the entire financial history of the US, from 1790 to the present, and shows us the lessons learned and how they apply to today. The blog I am sharing is a bit more than a month old but he is not looking at timely trades but long-term trends we should beware of. He has recently written about a concern for higher inflation than many are expecting, given the similarities of today to previous times in history. I know I am guilty of confirmation bias, but I have a lot of sympathy for his views here.

The third is a Substack called OpenTheBooks. This is one that anyone who watches political media may be aware of. In fact, a chart from this blog made it’s way into the recent DeSantis vs. Newsome debate. Adam tries to bring an objective view of the inefficient and wasteful spending that is going on in government. Given this spending is leading to a US debt problem, that may impact inflation, it is quite important to follow. In addition, as the government plays a bigger role via fiscal spending, it is important to know what ‘winners’ have already been chosen because of the tailwind of fiscal largesse. This particular post was about the money that has gone into the Middle East in the current administration, and may help us understand how the problems in the Middle East play out. After all, as we learned during Watergate, we need to ‘follow the money’.

Another new one to me is Dax Trading Ideas. I am interested in the unfolding recession in Europe, where we got more corroborating evidence that Germany may in fact be in a recession already. However, we also know there is a lot of potential value in European shares vis a vis US shares. Thus, I want to hear from people on the ground in Europe about what looks attractive and what does not, and why that is the case. Another one that costs money but if you are interested in Europe, could be worth your while.

Along the same lines is Brazil Stocks. With the dollar potentially set to seem some weakness in 2024, it is typically a time for emerging markets to being outperforming. Brazil could well be a big beneficiary of these flows. This blog is written by a Wall Street veteran and brings that approach to Substack. Another one where you can search for new ideas.

Finally, I will end the recommendations with the Weekly ChartStorm by Callum Thomas. I have recommended this one before and for those that may not use a lot of technical analysis in their approach but want a one-stop shop for what they need to be aware of, this is your place. Even for those who are good with technical analysis, you will see how others are viewing the landscape now. A quick read that can get you up to date on the markets.

Continuing on, I want to look back at my LinkedIn posts for this week. Each day when I write my chart of the day, I do not sit down with any pre-ordained notion of what I will write about. I look through the news and headlines, I observe the price action from the day before and that morning, and determine what I think is percolating as the narrative in the market that day. However, when I look back over the week, I can often see that there was a theme to the posts I wrote that week. As such, I am going to share them all with you so you can see how this theme developed.

Monday — duaration

Chart of the Day - leadership

Another frustrating Saturday during the Fall for Illini fans this past weekend. In a must win game during rivalry week, to a team that started the year with an interim coach, we failed to show up. We failed to deliver. Thus, we will sit at home while just about everyone else in the Big 10 goes to a bowl game

It is hard to put your finger on one thing in a decade of futility. However, if I tried to, I think it would be a lack of leadership. In the past, that was at the top with poor head coaches. On Saturday, that came from the players as the seniors led a team with little emotion, little fight but lots of mental mistakes

Leadership should always be top of mind. I teach about leadership in my MBA 590 course. I rely on an excellent book by UofC professor Linda Ginzel. Many people conflate managing and leadership but she makes a clear distinction

Managing is the present – meetings, budgets, expectations, time

Leadership is a choice – a choice to create a different future, can be small or big

We had players & coaches who maybe managed the present leading up this week. We had no one step up to create a different future

Turning to the markets, at the end of October we had someone step up to create a different future. The Treasury announced how it would be funding the government in Q1. At this time, it announced it would be issuing far more Bills & fewer coupons than expected. I drew a vertical line at this date

On the surface, most people don't even notice. Some might wonder why the govt chooses to take on more refinancing risk by having to come back to the mkt more or why it wouldn't choose to issue at the lowest part of the curve (10 yrs) vs. at the very front which has the highest rates

The bond mkt noticed that this announcement meant there would not be as much duration hitting the mkt. Bonds, which had been on a relentless decline all year long (white) started to rally & haven't looked back

Other duration assets rallied too. Small caps (yellow) which are struggling for cash flow ripped higher. The equal weighted stock mkt (blue) moved much higher & continues now. Even crypto, which had already rallied on the ETF news, took another leg higher as the mkt sought duration

A mkt that was looking troubled at the end of October suddenly has gone into full Santa Rally mode with many suggesting new all-time highs are in sight. Primarily because someone stepped up to create a different future

I wish someone would step up to do the same on the Illinois football team

Tuesday - credit cycle

Chart of the Day - roll, re-roll, lid

In some banter on text today, some golfing friends and I were talking about some of the games that we play on the golf course. One of those games allows those who are down to 'roll' the wager which means to double the bet. The other team can re-roll & then there is a chance to put a lid on it

I had this in my head as I was reading some of the headlines, considering the podcast series I am doing and thinking about the stocks we are analyzing in the final presentations this week. Right now, it all comes down to the cost & availability of capital

The headlines start with Signa, the Austrian-German property firm that has seen some units declare insolvency while it is scrambling to find funding. There are loans that are coming due & Signa needs to roll these into new loans. As we know, a rolling loan gathers no loss

It isn't just Europe however. China is having its own credit events as Zhongzhi is in such difficulty the management team has been placed under arrest or whatever it is called in China. The govt is trying to sort this out as many wealthy Chinese are losing money in wealth mgmt products. This leads to unrest

It made me think of the Investment Exchange Forum podcast series on private credit I am doing for CFA Society Chicago right now. This space has seen a lot of money flood into it. Is there a risk of misallocation of capital as investors rush to take advantage of flows?

The bullish argument would be that these investment vehicles are relying on an old principle of banking - all underwriting is personal. By having deep relationships, these lenders can work with companies thru problems that the heavily regulated banks can't

The bearish argument is that even with the money into the space, given Basel IV & more regulations on regional banks, there is a vast shortage of capital available to companies in need. US Treasury issuance only crowds it out more

In class this week, we are analyzing financial stocks. Of course we need to understand the balance sheet risks, how much mgmt has reserved for loan loss, what mgmt experience is in navigating a cycle, and where these loans have been made

One thing is for sure, in the era of low if not negative rates as we saw in Europe, there was capital misallocated. The cycle will find out where it was. Look at the chart today. Signa bonds just 2 years ago were trading at par. Now, after rates have gone up 4.5% in 18 months, these same bonds are trading at 11

This is not the only place we will see a problem. Credit events naturally follow cycles where there was too much money at the wrong price. With capital now more scarce & at a much higher price, where will the problems rise

This is a time when the person who is down may look at you and say 'Roll' and the response shouldn't be 'Re-roll' but rather 'No thanks'

Wednesday - interest rate scenarios

Chart of the Day - scenario analysis

I talk about mkts everyday with a friend. Yesterday in the a.m. he said "Equities higher & bond ylds lower as Ackman says the Fed will cut in 1q of 2024 due to a weakening economy & a real risk of a hard landing"

I joked that this is saying equities are higher because Ackman fears a hard landing. The thing is, I think he was right in capturing the mkt views but I fear it shows how the mkt may be set up for risks ahead

In all of my classes I speak about scenario analyses. I want to make sure the students understand that a model that captures one possible outcome is far from complete. A single DCF can't capture the intrinsic value

But if we work through a base, bull & bear case we are now onto something. We get a picture of what could happen in our most likely view, but also if we are wrong by either being too optimistic or too pessimistic. We can go further by doing Monte Carlo simulations too

The point is forecasts are often wrong & we need to understand this, but we should also anticipate where we could be wrong & what that means for potential outcomes

Let's take the above situation about rate cuts & the economy. The mkt is pricing in 3-4 rate cuts next year. In addition, it is now consensus that the mkt expects a soft landing. This is the base case

Why would the Fed cut rates if we have a soft landing? The argument goes that every time the Fed pauses 6-9 months later it begins cutting rates

This leads to the Peak Fed mindset & the Santa rally. After all, if the cost of capital comes lower while earnings hold up fine, who doesn't want to buy stocks. The question I have is how likely is that? It's happened 3 times in 14 Fed rate hike cycles

Another scenario may be the one Ackman is referring to. This is the other 11 times in rate hike cycles. This is the one where the Fed cuts rates, 6-9 months after a pause because we are clearly going into a recession or a hard landing

In this case, perhaps rate cuts will support multiples (P/E) where it is, but earnings are going to come down sharply. Let's say earnings fall from 216 by 15% (it is usually more on avg) to 184. Put the same 21x P/E & SPX is 3850

Maybe you think this is too bearish. So what of we do in fact have a soft landing. We are getting sizable fiscal stimulus & in an election year this may continue to carry the day. This may be the Jay Powell scenario who keeps telling us that rates will be higher for longer

This is the one where we have a soft landing but where rates stay at 5.25%. This is one where P/E are going to revert to more normal levels of 18-19x even if earnings stay where they are at 216 because of a soft landing. This gets us to 4100 or so

I am open to the notion there are other scenarios. Please put your favorite scenarios in the comments. Right now, I think the mkts base case scenario looks more like my bull case & my base & bear cases see lower mkts in 2024

Thursday - fiscal and capex spending

Chart (more of a collage) of the Day - renewables infrastructure

I have been talking to my daughter Lauren Excell a lot about her work lately. She is fortunate to be presenting her work/paper at IC2UHI2023 (https://lnkd.in/gbTvvtNg) in Melbourne, Australia in the coming days

Her work focuses on "Multi-scale retrofit pathways for improving building performance and energy equity across cities". It is above my paygrade but it fits squarely in the work people at a conference on countermeasures to urban heat islands will care about

As I was sitting down to digest the paper, I noticed there were a few emails that came in & were speaking much to the same topic. The first came from Cap IQ which discussed that top wind & solar developers plan to add 110 GW of capacity in the US by 2027

In spite of near-term cyclical demand issues, these companies are looking at projects focused on the long-term secular trends, much like the decision when retrofitting urban landscapes

After all, there are still state mandated targets for percentage of renewables that still need to be met. So even with a higher cost of capital, these projects get done since state regulators are likely to approve rate increases to pay for it

This leads me to a chart in the lower left from Rob West at Thunder Said Energy. He is a great follow if you care about energy mix. The chart is from the UK but he sent one for California as well

It shows that as more renewables are added to the mix, one of the big winners is nat gas. Why? Because while renewables have come down in price & have low CO2 intensity, they are still intermittent.

Even as the % of the grid moves higher for renewables there needs to be a baseload power that can fill in when needed. The empirical data in UK (which is now 28% wind) & while solar has climbed to 20% of the grid in California overall, 40% of the time it is 0%. Thus nat gas has grown as well

In the lower right we see the nat gas futures curve. Nat gas has had a tough year. After a booming 2022, it collapsed this year. Over the summer it tried to breakout but is falling yet again

However, when we look at where it is priced longer term, we can see (absent the seasonal spikes & drops) the trend is moving higher. Others may agree that nat gas is a winner in grids that are consistently moving more toward renewables

Back to Lauren's paper. As I told her, I think there is a lot of work to do on retro-fitting urban buildings in the coming yrs. 1st, there are going to be many buildings that fail to secure new funding, so the new owner (the lender) will look to retrofit to attract new tenants in some way

2nd, the biggest cities are all moving toward renewables & therefore buildings need to be updated for this world. For those that think this is only a California thing, note that Texas now produces both more wind & solar than California. Nat gas may need to play a part in all

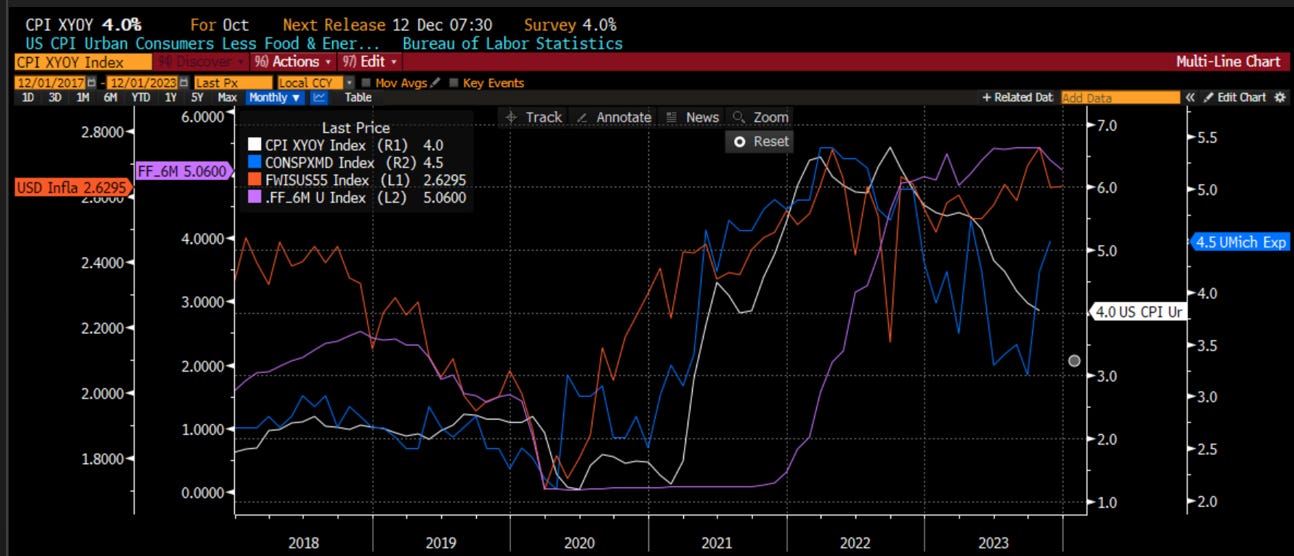

Friday - inflation

Chart of the Day - inflation

Bear with me because this may seem like a bit of a rant on inflation. The narrative taking over the mkt is clearly one that inflation will continue to gently drift back to, or below, the Fed 2% target. Thus, we now have 125 bps of cuts priced into 2024

Somehow a 0% m-o-m CPI print or a 2.3% PCE that is 0.1% below consensus feeds this 'immaculate disinflation' narrative. However, it decries logic to me especially when we look at other data around it

The GDP Price Index was higher than expected at 3.6% & the PCE core deflator was at 3.5%. Seems well above target. You know what else is well above target? The y-o-y core CPI at 4%, double the Fed target

I ask all of you this: what do you think of your own cost of living index? Is it 0%, 4% or even higher? I can tell you the Social Security Administration sees it staying higher. The cost of living increase for 2024 is 3.2% after 8.7% in 2023 & 5.9% in 2022.

Lately I have had the experience of reviewing many projects involving trades, on a large scale school renovation & given some home emergencies. I can tell you that comparing to quotes from 2021, costs of materials & labor are up 70-100%. Are they flat m-o-m? Who cares? Salaries are not up 100% in 2 yrs

Make no mistake, there are secular drivers of inflation: supply chain rationalization, energy transition, & too much debt. All pols will tell us we can grow out of the debt but the reality is no one has the courage to restructure, we won't default, so inflating our way out is the easiest option

In January 2021, Pres Biden made the statement inflation didn't matter as long as wages kept up. So now the path is twofold: 1. to stand on the picket line with workers urging higher wages 2. to gaslight us that inflation isn't higher

Consumers aren't stupid. Look at the blue line which is the 1 yr inflation expectation. It's spiked of late after coming lower earlier in the yr. Look at mkt expectations in orange These stay at the highest levels in yrs. The purple is Fed Funds in 6m. I think it will stay here or higher

Jay Powell doesn't want to be Arthur Burns. He cares about his legacy. Much like Ben Bernanke, he knows price levels are a mindset more than a number. Ben was very worried about a deflationary mindset taking hold & went to extreme measures to ensure it did not

Jay knows that inflation is a mindset that may be taking hold. I think he will also go to similar extreme measures to ensure it does not. In my mind that means higher for longer. In my mind that means letting the economy have a hard landing. Maybe another hike if the data stay strong

The notion of the immaculate disinflation driving both stocks & bonds higher, w/the Fed normalizing policy & the economy chugging along is a possible scenario. What are the odds?

Any deviation from this will be bad for markets. We get a week & a half of data before the next FOMC. There are many catalysts ahead

As you see, the theme all week is about how dovish the market is when it comes to rates and credit. However, there are many risk factors and scenarios that I don’t think the market is considering. Many of these risks are identified in the blogs by people like Beachman, Mark Higgins and Adam Andrzejewski.

I hope you enjoy the various resources and the ideas that percolated this week. As always …

Stay Vigilant

Very humbled and grateful for your recommendation, Richard. Thank you.

Here is what I wrote to my subscribers this afternoon....

As I wrote last week, I am getting a bit more cautious about the market. FOMO, froth, rocket emojis and diamond hands are showing up again in the financial media, fin twit and online forums. We have seen this movie play out multiple times over the past three years. We all know what tends to happen next. It amazes me how investors do not learn lessons even though they are so recent and should be fresh in our memories.

My long time readers know that I am not a perma-bear. If you read my posts from last year, arguably one of the worst for investor portfolios in recent times, you will see how I was mostly positive about markets, the economy, consumers etc. And I continue to believe that stocks are some of the best places to put money to work.

I am not advocating a crash…I want to be clear about that. I am just being cautious right now. I think we will have some sort of pull back leading up to Dec 15th that will then be followed by markets rising back into the new year. I was expecting these conditions in late Dec. However, everything seems to be sped up by 2-3 weeks. Mr. Market loves to keep us on our toes. (I could be proven completely wrong.)

My stock wish list is ready. My buy points have been identified. Game on!

Possible improving credit conditions improve outlook for capex and re-financing nullifying Ackman scenario. Ultimately though inverted yield curve proves too much, a recession pushed out to late 2024/25...? Anyone’s guess