Trick? or Treat?

Is the move in the markets over the last 2 weeks just another head fake or is there something more to this?

Before I get started, I just wanted to put in a quick note. I have been writing this blog for 10 months now. My goal is to demystify finance, to help as many people as I can. I do this when I teach and I do this with family and friends. I want to help as many people as I can. If you like what you read, please like and subscribe but also please share. The more people I can reach the better for us all.

Now, on to the show …

We are through the month of October now. It has a horrible reputation as the month of crashes. In fairness, that reputation is well-earned as there were major crashes in 1929, 1987 and 2008. However, in aggregate (as you will see below), September is on average the worst month of the year.

We knew this month would be important. We are still in the throes of a hyper-aggressive Fed. We also were treated to Q3 earnings by the majority of firms in the last several weeks. As we wrote a month ago, this month would dictate the course of 2022 but would it, could it, also dictate what happens in 2023? Let’s take a look.

The price action in the SPY has been pretty positive the past 2 weeks from the October 12 lows. Those lows took us below the June and September levels and there was reason to believe this was the big one. However, the last two weeks have been quite positive. It all started on October 13 when we received the latest CPI report. It came in higher than expected and stocks opened down and went a fair bit lower. Then it all turned around and stocks ended closing up almost 3% that day. Was this the capitulation that everyone had been calling for? The bears would tell you certainly not because the market bottomed well above the levels called for by many. However, the price action was indicative of at least a near term low. As you can see in the daily chart, we have now rallied 12% up to the 390 level, which used to be support and it now resistance. The Ichimoku cloud also comes in here. That is fancy language for this being the level where the majority of people either bought or sold most recently. It is an inflection. The bears had been in control but the bulls are mounting a comeback.

We had spoken about it before, but the stock market had tried to rally a few other times but could not follow through because the bond market traded so poorly. Every time stocks would rally for a couple days, but bonds sank, one knew that the stock market would eventually go lower again. However, on this latest rally, the bond market has found some footing. After peaking around 4.25%, the 10-year yield is now back to 4%. We can see the MACD crossing over lower which suggests that yields could head back to the 3.50-3.70% area. This would provide further support for stocks.

Another part of the risk-off story has been the dollar wrecking ball as it is called on Twitter. Not sure who coined that term, but it is good. Mr. Risk and I spoke about this a few weeks ago. In the last couple weeks, the dollar index is also showing signs of having peaked. As it has been a major driver of risk-off, is this now a sign of risk-on?

One of the issues we have been harping on since June is how bearish market players are. As a bear myself, this has always made me nervous. Positioning is not enough to get me to take a position. However, it is kindling for a fire that if any catalyst provides a spark, one might get burned. Bears in the SPX have been correct for most of the year. You can see the peak short was put on near the bounce in the market late August and early September. We are still close to that max short position, but now we are at an inflection. Will bears look to cover? Or is this a chance to add to the position?

Another sign of bearishness was in the options market. As I mentioned, I look at the 20-day moving average of the Put-Call ratio. People buy puts (insurance) when they are nervous. People trade calls when they are bored (sell them for income) or tactically positive (buying short-dated calls e.g. as in GameStop). We were at a peak in bearishness in early October. While we are still near that level, the moving average has rolled over and headed lower. When this average heads lower, it is positive for the market. Think of the period from early July to the end of August. Think of the start of the year. This is a positive sign for short-term risk taking.

One other measure of bearishness is the AAII bulls less bears. I know all of the negativity on this metric but frankly it works. It has been the most bearish this century. It is still at the -20 level that shows extreme bearishness. Retail has gotten a little less bearish but is still quite so. There is still more dry powder to assist this rally.

I also like to look at the internals of the market. I can recall back to late 2021. I would read people that said the equity market was too bullish, naively bullish, and it was ignoring trouble ahead. I disagreed at the time. I suggest the smarter money in equities was acting. I saw this because of relative sector performance but, more importantly, because the small caps had been meaningfully lagging the large caps all year long. This was a sign of trouble. The small caps had led from the Covid lows through early 2021 but peaked in relative terms in Q1. Thus, I found it easy to fade the market in Q3/Q4 of 2021. If we look at this internal performance now, we can see that the Russell 2k small caps relative to the S&P 500 large caps have been making a series of higher lows. The ratio is right at the resistance around .473. If we can sustain this level, it is a bullish sign for risk.

I wrote about this on LinkedIn this week:

“Maybe the US economy, while slowing, just looks materially better than everywhere else in the world. Perhaps this is why the USD is so strong. Perhaps this is why the SPX outperforms the rest of world. Perhaps this may even be why Treasury yields have moved higher vs. other sovereign debt if our expected growth rate is higher.

Somewhat corroborating the relative strength of the US economy vis a vis the rest of the world right now is the performance of IWM vs. SPY. Russell 2k is more loaded with domestic companies than the S&P 500. Not exclusively so, but more so. It is interesting to note that while the IWM has meaningfully lagged SPY for 8 yrs (or about a cycle), on this last sell-off in September/October, the relative price did not make a new low. In fact it bottomed at the 61.8% retracement of the entire 2000-2010 move in June, a level that has now held 4 times. Technically, this gives some hope of relative outperformance.

This is interesting because it comes at a time when every major country has begun to have more of an inward focus. We know what the UK did with Brexit a few years ago. This inward focus will continue even under another new PM because of the domestic issues. Europe is also focused on the continent because there is a war going on there after all.

Then we turn to China with the most stark changes. Xi Jingping was elected to a unusual third term. In so doing, and in the speech given, it s very clear Xi will have a focus solely on China domestically to the chagrin of companies outside that want to do business. He even awkwardly gave this signal publicly in removing Hu Jintao, who had been more West-friendly, from the CCP meeting.

Biden has continued Trump's foreign policy & upped the ante with NVDA, ASML & CHIPs Act. Countries around the world are focusing internally.

This presents a lot of risks. However, in the mkts, there may be winners as well as losers.”

Continuing on with the internals, I want to consider the Nasdaq tech stocks vs. the S&P 500. This ratio has also struggled mightily since the end of 2021. It continues to trade lower but is currently at the 252 week moving average. Tech bulls better hope that it holds this level. This is not a positive sign for risk, unless we are about to get new leadership in the market. Most would say I am crazy. However, the NDX to SPX ratio basically went sideways for all of 2003-2008. The market moved higher. There was leadership that came from outside of tech. Could it happen again?

We definitely are seeing a changing of the guard at the very top of tech. The mega-cap FANG names: Facebook (now Meta), Apple, Amazon, Netflix, Google etc. in the 5 years ended 2021, the mega-cap tech was up 400+% while the SPX was up 125%. Anyone who didn’t own the mega-names was left in the dust. Given the market-capitalization weighted nature of indexes, now those indexes are disproportionately weighted in those names. The top 5 are more than 25% of the index. In order to move higher, the market needs new leadership. Without new leadership, this is just a headfake.

Recall at the top I mentioned the seasonality. You can see that the 25-year average shows you August and September are worse months than October on average, even though October gets all of the press. This is because of the positive drift in stocks we typically see and because October is an earnings month, so earnings + drift means typically a good month. While October has been positive, November and December are considerably better, coming in 2nd & 3rd of all of the months (after April) over the last 25 years. One word of caution, though. This seasonality is biased by direction. The best end of year rallies happen in years when the market is positive. It is a continuation of the move. It is less likely to happen in years when returns are negative. Callum Thomas from TopDown Charts just did this analysis this past week. Check out his work on Substack if you are interested.

If we are going to see a continued rally it needs to come from earnings. Mr. Blonde does a much more thorough job on going through all of the earnings than I can or will. You can check out his Substack too. However, a quick look through earnings suggests that at the top level, earnings are coming in better than expected. Yes, there is a game played on Wall Street between companies and analysts. Earnings generally come in better than expected. However, with half of the market having reported, you can see that we are averting the worst fears right now. This is largely across the board with the notable exceptions of Materials, Industrials and Communications which i will go into below. You can see from the lower rightm though, that there is not much correlation to the reported earnings surprise and the 1 day stock reaction.

If we look at sales and earnings growth, it is also positive in aggregate. Companies are still seeing strong topline growth in sales because of inflation. However, it is harder to see that drop to the bottom line because now we are seeing margins suffer. Energy is the standout performer so far this quarter. Materials and Communications are the big losers. Seeing Communications and Tech struggle in this environment does not surprise me. These are businesses with high % of variable costs. Higher wages really hurt. That is why we are seeing the biggest layoffs in these sectors. Materials is the one that surprises me.

Materials bothers be because these businesses are high fixed cost businesses, typically with little pricing power. In inflation, these business should do well, as the higher top line can drop straight through with little margin pressure. In business cycle investing, if we are in inflation or stagflation, Materials are a good sector to own. However, Materials do very poorly when we move into deflation, when prices start to move lower and growth is really slowing. The performance of Materials earnings gives me a warning that we may be moving into this next phase.

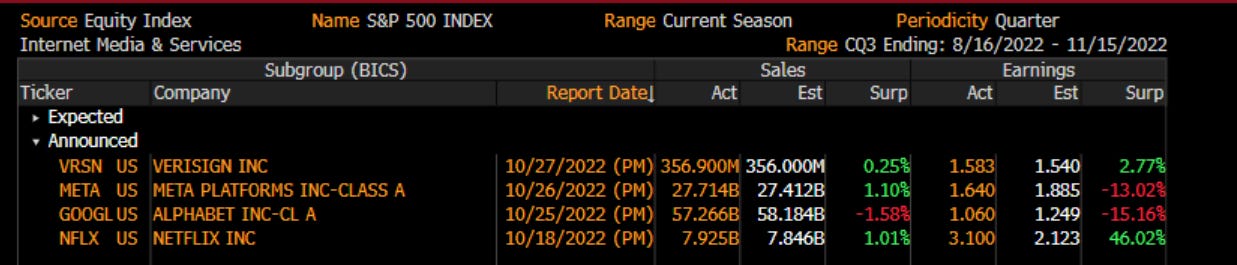

The weakness in Communications is entirely (and then some) from the weakness in Meta and Google. These former leaders are dragging down the group.

The weakness in Industrials is entirely due to one name, Boeing, that reported a ‘one-off’ $3.3 billion loss. Ironically, the stock ended the day higher because it spoke about higher Chinese aerospace demand over the next 20 years. Color me skeptical, but is this a reason to buy the stock? Do we think there is any chance that Boeing will be a pawn as Xi Jingping looks to retaliate over the CHIPS Act that the US passed?

I mentioned Mr. Blonde above, but another person that does a really good job of sorting through earnings is Jonathan Golub at Credit Suisse. He broke down the results so far (going so far as to break out Boeing) to show you what is driving earnings. As we can see, the topline growth is strong, and margins are hurting. However, on net, it is leading to a positive earnings which is then augmented with buybacks. The cyclical parts of the market are really driving the story, led by Energy.

If we just look at this relative to expectations, you can see that the surprises are positive across the board except in the big names like Meta, Google, Amazon and Boeing.

I love this chart because it shows very succinctly what investors are rewarding. Revenue beats are the big driver of positive performance. If you miss on both revenues and earnings, you can expect your stock to be materially punished. If someone tells you that stocks are not moving on fundamentals right now, show them this chart.

Speaking of earnings, Nancy Lazar at Piper Sandler just put out her 2023 forecast. She sees earnings for next year at $180. This is a major drop from the $220 expected for this year. She sees earnings dropping more and this year ending at $200 with next year down to $180. You can see the inputs to her model below.

This all goes back to HOPE which we have talked about. Housing leads the economy into and out of recession. Housing is unmistakably negative (in blue) and continuing to fall. This is pulling down the ISM economic survey in white. S&P 500 earnings expectations are now starting to roll over. Will they fall all the way to $180 as Nancy suggests? Hard to say but it would not be a surprise to see a $200 number for sure.

If we look on a quarterly basis, we can try to parse it further. For $200 it is roughly $50 per quarter (it is not that smooth) and for $180 it is $45. A move to $50 would only bring us back in line with long-term averages. It is hard to rule out $200 for 2023 even if we don’t want to look at the most bearish forecasts.

What multiple would investors put on those earnings. Below I plot the Fed Funds future for early next year. I compare it to the Moody’s Corporate Baa yield and the S&P 500 earnings yield. You can see there is a tight relationship here. Stocks are the one place not keeping up. Even if we think bond yields are a little extended and these lines meet int he middle, that could suggest an earnings yield in the 7-7.25% area. That would put the forward P/E for stocks around 14x. $200 earnings * 14x P/E would put the market around 2800 vs. 3800 where it is now. This is a rough back of the envelope but gives a useful idea of what could happen. I am not even trying to be that bearish. If I wanted to be bearish, I would suggest a 12.5x P/E (yield of 8%) on $180 eps. That would be 2250. I personally do not see things getting that bad, but it is within the realm of possibilities.

I showed you the positive short-term chart when we began, but now let’s look at a longer-term chart. A retracement into that red rectangle, which is the 50-61.8% retracement of the entire move from the bottom in 2020 to the top in 2021. This would put a fall into the 3250-3500 range. On the plus side, the weekly MACD is turning higher so perhaps this fall is into next year. However, the damage doesn’t appear to be finished yet.

I had this discussion with a friend and former broker this week. He mentioned how it was clear in the price action that someone was accumulating Bitcoin. I suggested that if someone was looking for an end of year risk-on trade, this was not a bad place to look. Why? You can see from the horizontal line I drew, there is a strong demand for Bitcoin in the 18,500 area. It has tested and not gone below that level for 4 months. On the positive side, it has moved above the downtrend from this year and there is no resistance really until 28,000. So, if you buy it at 20,000, where it was at the time, you would be risking 1500 to make 8k or more than 5 to 1 reward to risk. Yes, it could go below 18500 of course but one could put their stop-loss there. For an end of year risk-on trade, this sounded better to me than stocks where the upside might be to 4200 and the downside is 3500 for sure. So with SPX at 3800 where it was, this was a 1.33 to 1 reward to risk. Doesn’t seem as appealing does it.

I also spoke about this on Ether on LinkedIn this week:

“Chart of the Day - subsidiarity. As parents of 20-something children, my wife & I are going through the phase where they no longer need us for every decision that needs to be made. The vast majority of their decisions are made by them. They are in a better position to make them, are closer to the situation & have more facts. They should make the decisions.

Such is the principle of subsidiarity. Merriam-Webster defines it as: a principle that functions which are performed effectively by subordinate or local organizations belong more properly to them than to a dominant central organization. We seem to be at a point in time where this issue is coming to the forefront.

If we go back 100+years, there was a great debate in the world. We had the so-called robber barons, a term used frequently during America's Gilded Age to describe successful industrialists whose business practices were often considered ruthless or unethical. Included in the list are Carnegie, Vanderbilt & Rockefeller. They enabled great advancements in the economy. However, it was winner take all & so they did. There was animosity toward this & thus the impulse of socialism rose in prominence in the early 20th century.

We may be going through something similar now. We have a similar set of 'industrialists' whose names are Bezos, Musk & Zuckerberg. They have enabled great advancements in the economy. However Silicon Valley is winner take all & so they have. There is animosity toward this & thus the impulse of socialism is creeping in.

100+ years ago while the debate was raging between capitalism & socialism, there was another theory put forth by Chesterton called Distributism. It asserts that the world's productive assets should be widely owned rather than concentrated. The theory views laissez-faire capitalism & state socialism as equally flawed and exploitative, favoring instead small independent craftsmen & producers, or if that is not possible, cooperatives & mutual organizations. It favors small companies to large (see yesterday's post). It is built on the notion of subsidiarity.

We can compare that to what we see right now with a push toward decentralization. We see that push in politics, with some pushing toward decisions being made at the state or local level instead of the federal level. We see that view in the food & clothes preferences as there is an upswing in artisanal production.

The chart today shows Ether, the coin behind the Ethereum network. Decentralization is also taking hold in finance, using this network. Smart contracts allow peer to peer transactions & things done locally instead of at a central authority. DeFi is alive & well with proof of stake the catalyst and yield generation coming from staking. After the pain of the past year, price is picking up ever so slowly.

Sometimes there are more choices available than are tried. Distributism was never tried. Maybe Decentralization should be.”

We can see that Ether vs the NDX/SPX ratio has held well this entire year but there is a divergence of late. The failure of mega tech is weighing stocks down while the risk-on year end may benefit Ether which has had a positive and not negative catalyst.

I am not here to give you trade ideas but to point out what I am seeing. I see a market that is still too bearish and for good reason. The economy is rolling over and this will bring down earnings. Yields are much higher which means multiples can’t go higher and could move lower. There appears to be downside in the economy and market in 2023. However, year-end seasonals and recent news, combined with still negative positioning, suggests we could see some positive price action for the next month or two. What are the catalysts from here? This week we get the FOMC on November 2. Any hint of a pause would be favorable for risk. We also get the latest reading on ISM. Any sign that the bottom is not falling out of the economy would be favorable for risk. Finally, we have elections on November 8. Any gridlock that comes into Washington that prevents any more fiscal largesse could be favorable for risk.

So, there could be a short-term treat for traders and investors alike. Much like the candy we get on Halloween, it leads to a sugar buzz that makes us feel pretty good for a short time until we come off that high. We might see that same thing for risk-taking over the next month or so. Be careful to not get tricked.

Enjoy your Trick or Treating and …

Stay Vigilant

Excellent post, thank you for taking the time to write it up!

Another great piece this morning. I was intrigued by your findings on strength in small caps and weakness in materials. The former surprises me given signs of an economic slowdown in the US over the next 6-12 months. I have been watching $BILL as a proxy for SMB sentiment and it seems to be plodding along / basing for a few months now.

I also like the question about who will be the new "FAANG" leaders.

Lots to ponder over. Thanks and Happy Halloween.