Weekend in the City

A little late this week as I spent my anniversary weekend in the city

My wife and I celebrate 30 years together today. We decided to spend the weekend in the city to celebrate as we are just too busy this time of year to go on the big trip we want to go on. That will have to come when things slow down. However, we had an amazing time eating at North Pond, 3 Arts Cafe and J. Parker while visiting both Lincoln Park Zoo (for the lights) and Second City. It was an awesome weekend in the city. Again, I am really surprised anecdotally because everywhere we went it was quite busy. Even the Michelin-rated restaurant turned the tables over. For the imminent recession that I and others foresee, there were no signs in the city this weekend.

However, we did get signs from at least some of the data in the last week. Last week was packed with relevant data, some leading, some lagging, that everyone (all traders and investors and even the Fed) needed to pay attention to. Let’s look into some of that.

DATA

The biggest data point of the week, that comes out at the start of every month, is the non-farms payroll report. I have gone on and on this year about why I think this report is not the best data point, nor even the best look at the jobs market. However, given every punter, pundit and pol cares about it, we can’t just ignore it.

On the graph below, I have put the inverse of the non-farm payroll number as well as the U-3 unemployment rate. The jobs number was much better than expected at 263k and the unemployment rate stayed at a cycle tight of 3.7%. With my anecdotal evidence of the economy this weekend, neither of these number surprise me. Given Jay Powell’s focus on the strength of the jobs market as the rationale for backing off rate hikes, I find it hard to believe the Fed will not follow through on the next 100 bps of hikes priced in. The market tends to agree as it added back some of the cuts it was starting to price in, though there remains this looming view that we are at Peak Fed. Recall the Twin Peaks post from September.

Something to note from this data - it is lagging. We can see from the graph that when the unemployment rate moves higher, a recession is starting. It is a little harder to see but the same thing is true with the NFP number. As it goes below zero the recession is starting. As investors, though, we are already looking through this and will only see this as confirmation when it happens.

One of the FinTwit Illuminati - ProfPlum - pointed out that the strength of the employment report may have been due to the Birth/Death adjustment. You see, one of the fun things in this data (and one of the reasons I struggle with it) is the statistical adjustment the BLS does. The birth/death does not refer to people but to businesses. It attempts to approximate how many companies are starting or closing. As Prof Plum mentioned, the trailing 12 month adjustment is about 1.3 million companies starting in the past year. We can see how that has looked over the past few years too. Seem like too many to you?

We can look at the monthly changes in this data on Bloomberg. You can certainly see some pronounced seasonality in the birth/death adjustment. In fact, it looks so consistent as to be wrong. However, it is a statistical forecast/adjustment and not what has actually occurred which is reason to be skeptical. That said, the adjustments in 2022, outside of a massive outlier in April which appears intended to reverse some effects of 2020, have seemed to some in about what you might expect given the 15 year averages, so I am not sure this is the driver.

Another good dive into the data comes from another Twitter Illuminati Bob Elliott. He is a very good follow for an objective look at the data driving markets. There are market players that have seen recent weakness in the household survey and use that as a reason to discount the NFP numbers. He looks into those in detail. I would encourage you to read the full thread but some takeaways in summary:

Full-time vs. part-time is showing no pattern this year though you would expect them to be correlated. There are no outsized gains in either full or part-time work

There are also no largely correlated gains this year across age cohorts. Some might expect younger works to be disproportionately benefitting but it appears the gains this year are pretty evenly spread out

There are no trends or correlations if we look at the data by race either. Again, pretty balanced across the cohorts

According to Bob: Bob Elliott

“When I look at the above, its clear to me that anyone making claims made primarily based on HH survey should be treated caution and skepticism. The survey has many markings of poor quality and a large band of uncertainty. So be careful taking much from it alone.”

One point Bob makes that I would agree with is the necessity of triangulating the NFP data with other measures of employment we have seen to get a more full view of what is happening. Just within the BLS data we see a strong company survey number and a weak household survey number. What about in the other reports?

The bears also want to look at job cuts. One of the big stories of 2021 was the strength in the Challenger and Gray job cuts survey. Companies were not firing anyone because they couldn’t get staff in the first place. That has changed quite a bit as we know from the headlines related to the tech industry. From this time series, we can see sharp increases in the number of layoffs do in fact lead to a recession as we would expect. This is certainly what we see happening right now.

My preferred measure of jobs is the weekly jobless claims data. It is high frequency, it is based on fact (who is filing for benefits) and it is not adjusted by the government. I have also included on here in blue the continuing claims data. This is a bit more important to watch at inflections because it approximates better the longer term unemployed. As we can see the last 40 years, as these measures move higher, we are entering a recession. Both have come off the lows and seem to suggest this, though the low levels were historically low levels so we need to be a bit cautious. However, the move higher in both initial and continuing claims is a sign of caution on the economy for sure.

Finally, I look at the ISM employment survey, both for manufacturing and services. When it falls below 47, we are in a recession. It just fell to 49. Not there yet, but also not looking healthy. This also bears more watching.

Segueing from the ISM employment into the full ISM data, I find the ISM to be the most important metric that came out this week. I wrote about it on LinkedIn:

“Chart of the Day - this time is NOT different. I made my way home last night on the long, boring drive up I-57. It has been particularly dreadful this semester given the massive construction (aside: not sure how a broke state can afford this, oh wait now I remember). However much of that has been winding up so I thought this trip would be different. It was not. Slowed to a stop around Kankakee just like the other times. This time was NOT different.

That is the message the mkt needs to hear again. And again. And Again. You see, this time is different are the four most dangerous words in finance. To use another trite phrase (hat tip M. Twain): history doesn't repeat, but it rhymes. Finance, after all, is quite simple. It is about cash flows & discount rates. That is it. Show me any asset class, anywhere in the world & one can value it using this approach. Crypto? Yep. That is why so many coins that were valued on the greater fool theory are now on their way to zero. Those that generate cash flow? We can find the right discount rate to measure the risk associated & derive a value.

Cash flows are affected by the economy. It is a pretty clear link: the economy drives earnings & earnings drive stocks (or economy drives the ability to pay the coupon which drives bonds). So the economy leads earnings. Stocks are also forward looking so the early measures of the economy & the stock mkt are coincident. Exhibit 1 is the ISM data we got yesterday. It fell below the magic 50 line. Readers/students will recall the chart I have used many times that shows the one part of the quadrant when stocks have negative avg returns is when the ISM is below 50 and falling. Insert big 'You are Here' arrow. The top chart shows the ISM & ISM New Orders to Inventories which anticipates ISM. ISM is down but usually hits 47 or lower before a recession. That is coming soon. Why? Because New Orders to Inventories is telling us this. The economy is going into recession soon. Economy leads earnings & earnings lead stocks.

What about the discount rate that we use to assess risk? In the bottom chart you can see how the Fed Funds futures mkt has gotten more dovish in the last month. It has priced our 25 bp of hikes. It still sees hikes until March of next year & cuts at the end of 2023. While the mkt thought JayPo was dovish (not) he did say they would hike as long as jobs are strong & today we see they still are. Hikes will get put back in. This means discount rates are not going lower. So those falling cash flows from the economy will see the same, or higher, discount rate.

Cash flows & discount rates. Which of these are moving in the investor's favor right now? In order to take risk here, one needs to believe it will be a soft landing with little or no recession. The data suggests we are headed for an imminent recession while the Fed still hikes. That is not a good time to take risk. This time is NOT different.

Stay Vigilant

#markets #investing #stocks #bonds #economy”

Pulling the data together, I find more bad news than good news. Little of this suggests we are in a recession at the moment. Much of it suggests we are about to enter a recession in the next quarter. There are certainly some positive signs and the NFP number was one of those. However, when looking at a fuller picture of employment, there are more signs of weakness than strength. The one sign of strength will mean more Jay Powell and not less. In total, I find the data this week to be a net negative.

FLOWS

How as all of this data impacted the flows into and out of the equity market? It is important to understand what people say or what they think, but even more important to know what they are doing.

My first look at this is the monthly equity flows. The best analysis of this comes via Ed Yardeni, another good follow on social media. Ed not only looks at the aggregate data but breaks it into the active and passive flows which I think is important in trying to understand how this money might be invested. You see, passive investors put the money directly to work if it comes in. Dollar in = dollar instantly invested and vice versa. Active investors may be more discerning looking to buy defensive names or looking to build cash etc.

Investors looked to buy the dip ahead of positive Q4 seasonals perhaps as flows in October were positive after a couple months of outflows. You can see in the middle panel, investors continue, as they have for years, to take money out of active funds. Thus, the money coming into the market is not discerning. It is going entirely, and then some, into passive vehicles. Passive funds buy the market as money comes in. Money has been coming into passive regardless of the net inflow/outflow. When we wonder how come stocks can get so out of line, we can simply look to the flows data to know that it is due to passive investing.

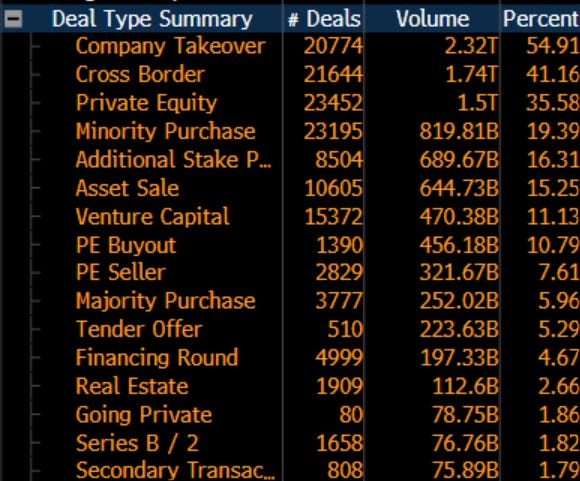

Another potential inflow into the market is via M&A flows. This is companies buying companies in total of course. We can see that this activity is not zero, but it is down considerably from 2021 and even from averages the last 5 years. 2021 was bull market activity and 2022 is a major return to the mean.

The biggest drivers of the activity we have seen come from cross border flow and from private equity. We know of the large pools of money that had been in the private markets. However, even this is drying up as we saw news this week that KKR was forced to do its latest deal (buying a French insurance company) in cash because it is not able to borrow in the private credit market to add leverage. This is an early sign that things are drying up and will continue to slow.

The last sign of rapidly slowing investor appetite comes from the IPO market. We can see the stark contrast versus the bull market of 2021. 2022 has also been much slower than in the pre-Covid era too. The deal flow has slowed rapidly which will negatively impact Wall Street bonuses and is indicative of slowing investor risk appetite.

The last place I look for what people are doing vs. what they are saying is the option market. I have discussed this Put vs Call ratio before and how/why I look at the 20 day moving average of such. If you squint at the far right you can see it is trying to move higher. If it does, this becomes a negative for risk-taking in the markets.

The summary of flows into or out of the market is negative. The money that is flowing in goes directly to passive vehicles which are supporting risk and are not discerning. However, the discerning flows whether via active managers, M&A, IPOs or the options market all are negative.

TRIGGERS

What can get people to change their minds? I have looked at many catalysts in this section in the past, but right now, with one month to go, there is really only one catalyst and that is the end of year seasonals. The so-called Santa Claus Rally. Or as Billy Ray Valentine told us in “Trading Places”, it has to do with the investors desire to buy the GI Joe with the kung-fu grip.

These seasonals are positive in Q4 to be sure; however, you can see all of this and then some has already been anticipated in the US markets which were up 8 & 5% the last two months. The Santa Claus Rally was front-loaded.

This was also true in the MSCI World (rest of World outside the US) which has even more positive Q4 seasonals but has seen big moves this quarter already. If we start to look into January, as surely many active players will, we can see for both SPX and MXWO there are negative seasonals in January on average the last 15 years.

Even emerging markets, which have been left for dead relative to the US given the strength of the dollar, showed amazing strength last month. Can this continue?

The Barclays US Aggregate bond index has more muted seasonals but also looks better in Q4 and even into Q1. This may be due to investors needed to reallocate out of stocks and into bonds at the start of the year to bring portfolios into balance.

The flows that most people care about are their target date funds in the 401k at work. Here I look at the Vanguard 2050 target date fund which is what people around 37 would be invested in at work. Interesting the December seasonals are negative for this over the last 15 years. Perhaps that individual rebalancing is done a little sooner. The performance the last two months will certainly be welcome in what has been a very difficult year. Will investors continue to dollar-cost average in their 401k in the new year? I would guess that answer is yes.

The Q4 and December seasonals are quite positive and quite strong. However, I am less worried about those right now given the strength we have seen in October and November. Yes, I understand the desire for many investors to try and get a better bonus, and if the market is moving higher, they will go along for the ride. However, I also know that investors will not want to see their bonuses reduced because of moves in illiquid markets after December expiration and ahead of negative January seasonals. Thus, I think they Q4 Santa Claus Rally is coming to an end on or before the December 16 options expiration.

Negative data, negative flows and a waning positive catalyst that is almost at its expiration. As I said in my LinkedIn today:

“We aren't quite at the recession level in either but the trend is not our friend. At the very least we need to see a bottom in the ISM in order to get more positive on stocks. We need to pay attention to the data & listen to the markets message.

If 30 years has taught me anything it is to pay attention & listen.”

Stay Vigilant

Brilliant Work! Thank you for Sharin!. Also Congrats on your 30 Year Anniversary!

“Crypto? Yep. That is why so many coins that were valued on the greater fool theory are now on their way to zero.” That’s a great point and that made me laugh.