My trip through Europe with our trading and investing students is at the halfway point. We saw a number of companies in Frankfurt, learning about the derivatives, flow trading and structured product markets. We then moved to Paris where we had one meeting on Friday, focused on private debt/direct lending in Europe.

In our conversations with finance professionals and the person on the street, one theme keeps coming up - tariffs. This was even before the 50% tariffs to be enacted on June 1 were announced. It is even more so now. While people in Europe certainly care about tariffs, the people in financial surveys do not seem to. Survey after survey that I see shows investors still think the tariffs will be delayed or even simply negotiated away. No one seems to think they will last.

It has me thinking about what medium term effect this tariff discussion will have. Could it cripple the economy in the near-term, as businesses and consumers alike simply put off investment and discretionary consumption given the uncertainty? That crippling of the economy inspired the picture above of the church at the Invalides, the hospital built by Napoleon for the soldiers wounded in his various battles. Much like Trump now, Napoleon was liked by many but also hated by many. He was also willing to pick quite a few fights. Finally, after periods of exile, he was able to come back to power. Napoleon is buried in the church, finding his final resting space with those who also perished in his many battles. Will Trump be buried by his tariffs?

Whether or not tariffs are inflationary is the source of a large debate. There are some very smart people on the side that says no, including Barry Knapp of Ironsides Macroeconomics where he recently wrote a piece called “Tariff Inflation Mythology” arguing that markets would turn their attention to the budget battle and away from trade (more on that below). However, there are others like Jim Bianco who are empirically arguing that maybe we are already seeing inflation.

On Bianco’s X account he posted a thread which argues we may already be seeing inflation from the tariffs, and this may be impacting Fed thinking. In the chart above, he shows that the dollar amount of tariffs collected year to date have soared by more than $24 bb.

Of course there was a front-running of the tariffs, as goods were brought into the US ahead of time. By doing some back of the envelope math on the goods brought in and the tariffs collected on them, we can see that the price of goods coming into the US is about 3.6% higher this year. Not all consumer spending is on goods. In fact, the vast majority is on services, and tariffs will not impact our services (though the immigration argument may). Not only is not all of our spending on goods, but only about 15% of our goods spending is imported. If we look at this 15% amount of goods being 3.6% higher in price, it suggests that inflation would go up about 0.54%

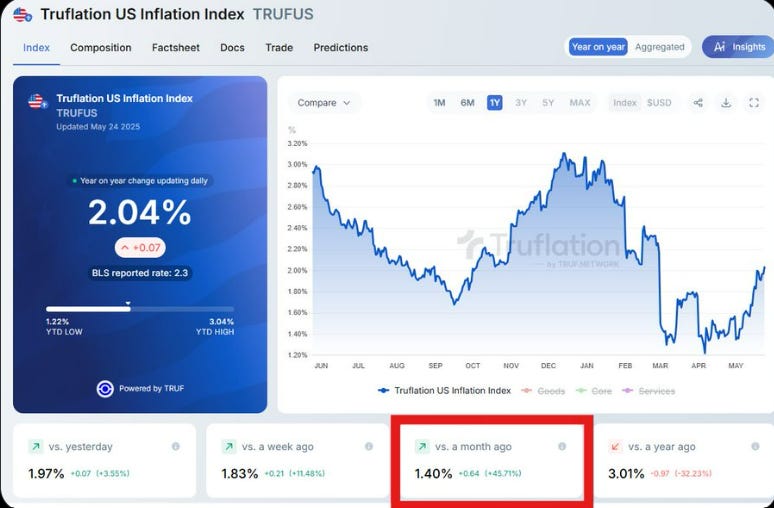

Then Jim shows that the latest Truflation report shows inflation up about 0.64% from one month ago vs. the 0.54% the back-of-the-envelope math would suggest. A pretty good guess and indicative that perhaps the Fed should and will remain in a wait-and-see mode when it comes to the cuts that risky assets want to see.

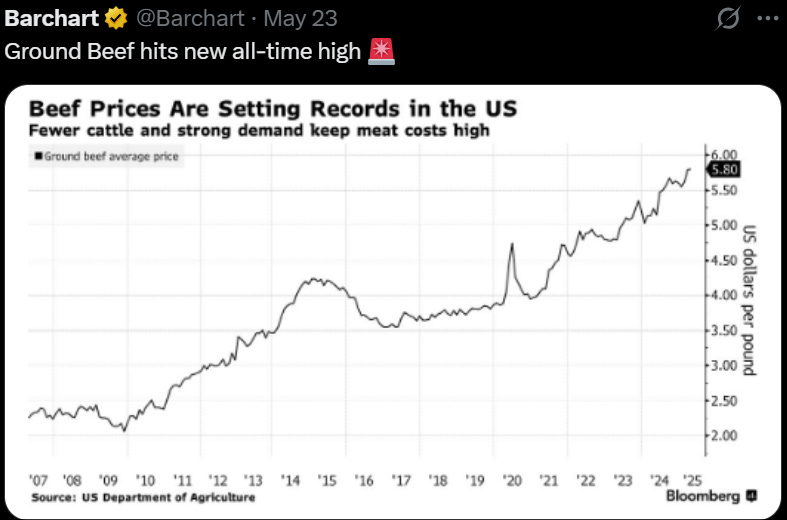

Often when you discuss inflation with people, they will tell you ‘yeah but look at gas prices going down so inflation is going to fall soon’. Gas prices do have a big impact, so I don’t want to diminish this, however, anecdotally, other costs are going up. For instance, I saw on X this week where ground beef prices are heading higher. I also know corn, soy, live cattle etc are all also heading higher. Food costs going higher may well more than offset the falling gas prices. When you go to Costco, you always buy gas too, but filling the tank on a monthly basis is not more than the amount you spend on other stuff.

What do higher prices mean for the bond market? The above is a very popular chart making its way around. In fact, Jared Dillian suggests that too many people are getting bearish on bonds and this could suggest they are about to rip higher. That is a fair point. However, asset owners and asset allocators might get some pause when they look at the rolling 10-year returns of bonds going negative for the first time. When the decision is made to allocate, will they assume that the future 10-year returns are going to be closer to the median? More than likely. However, knowing how poorly bonds have done, it could suggest these allocators are also willing to be patient and wait for the right price.

That patience is highlighted by this tweet by Nick Timiraos, the known mouthpiece of the Fed. He highlights how Fed governor Waller is having discussions where investors are indicating they would like to see more restraint in DC before getting excited about bonds. This may be to Barry’s point earlier that the market will turn its attention away from trade and onto the budget. With the budget bill getting through the House, the timing makes sense. However, as it sits in the Senate for the next 1-2 months, will trade come back to the forefront?

Perhaps, but this week, the discussion was on fiscal spending. The impact is seen much more in the very long end of the Treasury curve: 30 years versus even 10 years. Thus, it was notable that the 10-30 yield curve steepened this week from 25 bps to 50 bps indicating the market is not so confident that this bill is the right bill, preferring more fiscal restraint as the Fed’s Waller indicated.

Greg Ip, the former WSJ Fed mouthpiece, also wrote about rising 10-30 year yields but highlights the rising term premium. Greg correctly points out that Fed expectations staying constant helps us know more clearly that the move we are seeing does not have to do with changing Fed policy, but instead about fiscal policy. Rising term premia also suggests bond investors want to see higher yields before getting involved.

Brian Wesbury from First Trust, who I just had the privilege of interviewing, also indicates that DOGE failing and Congress not able to produce a bill with much restraint has caused bond markets to lose a fair bit of value. When stocks lost due to tariffs, Trump blinked. When bonds lose because of too much spending, will Trump blink? After all, he is the one that is chastising the hawks in DC for too much grand-standing.

It isn’t just the US bond market that is struggling. The Japanese bond market has started to notice. Yields in JGBs have gone up markedly, going up more than 2/3 in the last year and from 3 to 3.67% this year alone. That is a massive move and one that not only Japanese bind investors, but global bond investors will notice. Why?

Above you see the yields of both US and Japanese 30-year bonds. What you do not see is the hedging cost for global investors. In periods when the Dollar is clearly rising, many may choose to not hedge the Treasury buys. However, when tariffs are discussed, and the Dollar is thought to weaken, FX hedging becomes a bigger focus. Does this matter? The annual percent cost for FX hedging US vs. Japan is about 4%. Pretty massive huh? What does this mean? This means that 5% 30-year bond for a Japanese investor is actually 1% which doesn’t look as good as the 3% they get in JGBs. It also means that the 3% in JGB for a US investor is actually 7% which is better than the 5% they get in Treasuries. This means that for both Japanese and US investors, 30-year JGBs are the more attractive bonds.

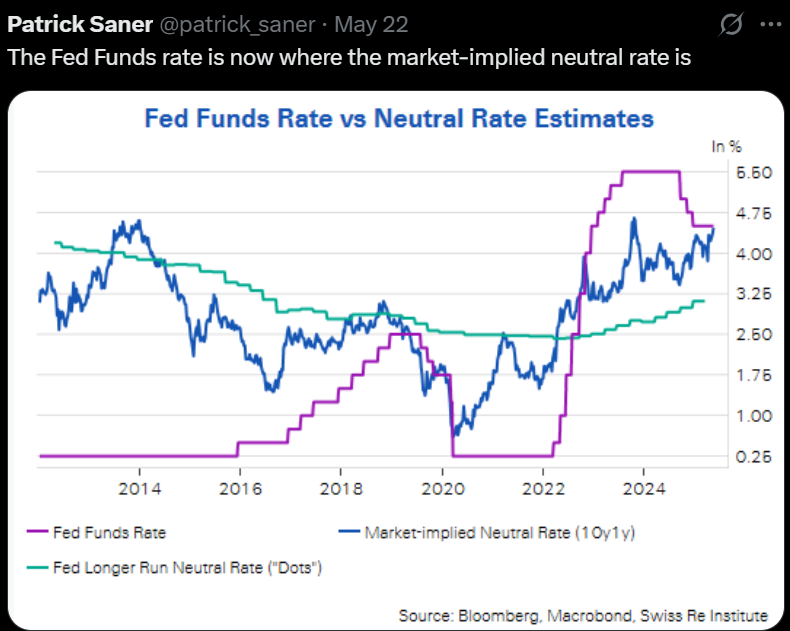

Perhaps it changes if the Fed blinks. What if the Fed decides to cut rates the way the market thinks? Greg Ip told us these moves we are seeing all assume the Fed is not moving. Patrick Saner (who we will luckily see in Zurich next week) pointed out on X that the Fed policy rate is now where the neutral rate is, further proof perhaps that the Fed may not be cutting rates at all this year. Is this what risky markets want to see?

Lack of fiscal restraint sounds like the ideal market for gold, right? Well, maybe it’s been too much of a good thing in gold. BAML points out that the 4-week moving average of flows to gold has actually turned negative. This, at a time when Bitcoin is hitting all-time highs on the back of the crypto stabilization bill making its way through Congress. Is Bitcoin preferred?

We can see the flow out of gold and the flow into Bitcoin most recently. I actually doubt that it is from one into the other, but gold investors took profits while Bitcoin investors moved in. I still think that these two groups need to get together because it is more powerful together than apart. As a side note, Invalides is covered in gold leaf. There is a total of 12 kg of gold leaf on the dome which is about $1.5mm in today’s dollars. Talk about a lack of fiscal restraint!

In a period lacking fiscal restraint, rising tariffs, global uncertainty, both gold and Bitcoin should do well. A 50-50 index is breaking out. I showed before how since late 2022, after a period of consolidation it breaks out to the upside. In fairness, I show back in 2021, after consolidation, it broke lower. Nothing only goes higher. However, what has changed since that period? Rising inflation.

In a period of rising inflation, like the 70s, both bonds and stocks go lower. Where are investors to turn? Perhaps it is into assets like gold & Bitcoin. We will learn more about gold and Bitcoin when we visit Switzerland next week so I will have more to discuss on it at that time. Until then, pay attention to the budget debate but also to the tariff debate and June 1 deadline. I know investors in Europe care about it. Maybe these tariffs will end up being Trump’s Invalides.

Restez Vigilant

You mentioned "about 15% of our goods spending is imported", implying that tarrifs may not contribute to inflation all that much. A fair point. But my gut tells me a lot of imported goods are big ticket items ... cars, machinery, equipment, white goods, electronics, mobile phones etc. Sticker shock will probably impact or delay spending for these items, and have a negative sentiment effect. Which could cloud overall spending in general?

Richard - how are things in Europe generally for US tourists these days? I am heading there in a couple of weeks. Stuff relatively expensive now given the rise in the euro? Lots of tourists or smaller crowds? Enjoy your trip and thanks.