Here we are in the days after the FOMC meeting, and it seems to me that we have as many questions as we have answers. Sure, we found out what the FOMC did on the 25 or 50 question but there still may be a disagreement about the direction of rates going forward. In addition, there still seem to be questions of whether we will have a recession or not and which way the market may head in the coming days and weeks. I thought I would dig into each of those.

Earlier this week, I posted my immediate reaction to the FOMC on the Macro Matters podcast I do for the CFA Society Chicago. I touched on the Dot Plots on the podcast, but I wanted to see how the market developed. This is what we know now:

The FOMC lowered their media expectation for 2025 from 4% to about 3.4%. However, the market was at 3% and it lowered its view to 2.8%. Thus, while the gap closed, there is still a pretty big gap in expectations. Not only that, look at the difference of opinion just for the rest of this year. The media FOMC member sees rates at 4.4% vs. the current 4.83%. So maybe 50 bps more of cuts at the median, but at the same time, there are a lot of dots that say either no cuts or maybe one cut. The FOMC is not looking to dramatically cut more this year. The market disagrees. The market sees another 3 cuts to 4.1% this year alone. The bond market continues to be much more dovish than the FOMC. My sense is the FOMC speakers will come out in the coming weeks and try to get the market to see their view. Is there a risk that the bond market will price some cuts out of the curve, especially for this year? That is a lingering question.

Then we get to the market interpretation of what this rate cut means. JP Morgan had this view:

“Over the past 40 years, the Fed has cut rates 12 times with the S&P 500 within 1% of an all-time highs. The market was higher a year later all 12 times with an average return of around 15%.”

Ed Yardeni had this view:

“Fed Chair Jerome Powell is forcing us to change our odds of a melt-up. In his August 23 Jackson Hole speech, he signaled that he was pivoting from an inflation hawk to an employment dove.” and "We will do everything we can to support a strong labor market as we make further progress toward price stability."

However, Lyric Hughes Hale shared this stat which might suggest that the 50bps is a sign that the FOMC seems something more negative than we are expecting on the horizon:

Jim Bianco shared this table and said with the SPX hitting all-time highs, the stock market is saying no recession yet:

Some in the market interpreting the FOMC move as a positive and some are suggesting it may be foreshadowing gloom on the horizon. There are lingering questions.

About that market reaction, I shared this post on LinkedIn this week:

Chart of the Day - churn cycle

In labor dynamics, churn is replacing departing workers with new ones as workers may move to more productive uses. Maybe this is going on in Silicon Valley with AI in the here & now. This can add to productivity

In accounting/finance, we may refer to churn as the rate at which a company loses customers or subscribers. Typically we want to see high retention so a low churn rate

In technical analysis, churn is when you are entering & exiting positions quickly, getting mixed signals from the market. It is a period of confusion that you hope resolves itself

The last two months have been a period of churn for traders, particularly those following the Nasdaq or other risky assets like crypto. Take the chart today for example

I have drawn the trend channel on the chart with defines well that the period form October 23 thru the end of July was a very obvious trend. The bulls were in control the entire way with a series of higher highs & higher lows. Everyone wants to ride this trend & not fade it

The early August de-risking event changed that. You can see the 1st of the red circles & this is the point at where the bulls riding the trend would stop themselves out & go to cash. The bears would enter the short trade as the trend may be changing

Then we get the second circle in later August. We move back into the trend channel. Bears would be stopping out their short positions here. Bulls might be inclined (were inclined) to get off the sidelines & back into the market

Move to the early September growth scare that led to a rapid repricing of Fed Funds. We again broke below so bulls would get out of their longs & bears would jump back in. We get to this week & get a dovish Fed & a mkt deeply believing a soft landing and 1995 redux

Yesterday might have been some bulls getting back in or some bears stopping out. However, if you look at the last of those circles, we really aren't yet at that level where stopping out or back in should happen

Today we get triple witching, with expirations in stock options, futures options & futures themselves. The focus will turn to the dynamics of exercise/assignment & rolling positions. Less about the Fed & the data

However, where we end up today might give us a clue as to whether the rest of the bulls get back in or the rest of the bears stop themselves out. Will we end up back into that channel or not

The churn continues. Not a particularly fun time to be a decision-maker on Wall Street. More fun to be executing orders on behalf of those accounts I would think

Let's see what today brings as it may set the tone for the rest of Sept & into October

I focused on the Nasdaq for this post because that is where the majority of the market attention is right now. I feel it is the best barometer of market sentiment. If I looked at the S&P 500 or Russell, those charts are looking a bit healthier right now. Bitcoin, another measure of market risk, is back at the average level of where people have bought ETFs this year so there is a struggle still between bulls and bears. The next week will be telling because the last two weeks of September have the worst seasonality of the year due to individuals selling stocks to raise money for taxes, companies going thru their own filing periods and larger companies in blackouts so not buying back stocks. The charts aren’t entirely clear, and I want to avoid some churn, but may be suggesting a better Q4 ahead.

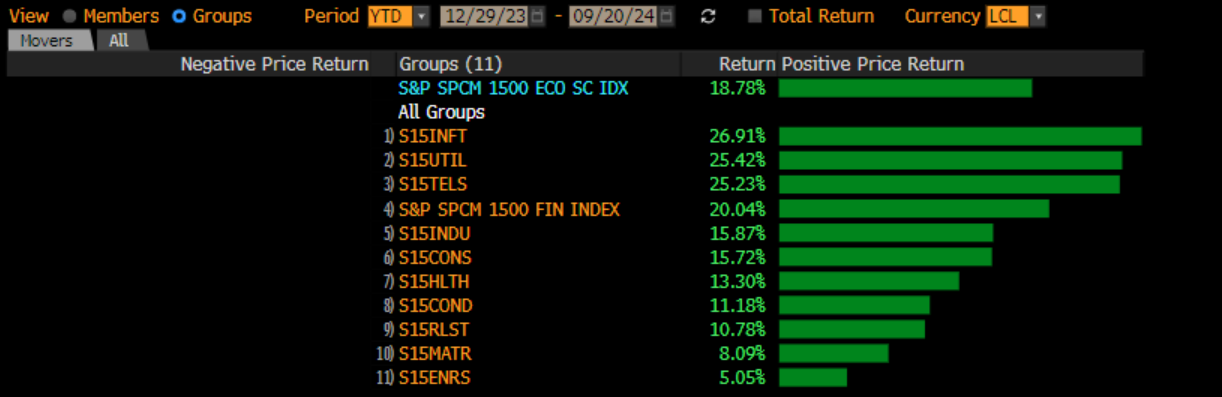

Speaking of the market, what has it been pricing in. This is year to date relative moves:

While this is the last 3 months:

You can see that year to date, tech is a top performer still. However, over the last few months, tech has dropped to the bottom as a source of funds. You also see capital intensive sectors like REIT, utilities and financials all near the top with energy and materials also at the bottom. This suggests to me that the market has given up on any fears of inflation whatsoever. It also says there are concerns about growth going forward, thus there is a preference for those names that may not have as clear of a growth profile, but which more clearly benefit from rate cuts. What happens then if the FOMC starts trying to take rate cuts out of the picture? The leaders of the market the last few months are rate cut beneficiaries. Could this hit the market? Another lingering question.

On that issue of whether inflation is completely gone, I have my doubts. As I have said before, inflation is a mindset more than a number. Hitting close to home, the SEIU is weighing the possibility of a strike at my university. In another story close to home, Boeing machinists rejected a contract that saw 25% wage gains over 4 years as not enough, but Boeing responded by saying employees elsewhere would be furloughed and deliveries of aircraft slashed. Thus, the unions are still feeling like wages are not keeping up with this inflation that the market and the FOMC are telling you is no longer an issue. Throw into the mix, we have two candidates in November that both want to spend. This chart from Don Schneider at Piper Sandler:

Perhaps we should be surprised that consumer inflation expectations for the next 5 years are going higher. Even a near term impact of inflation, falling oil prices, may be reversing course too. What will this mean for CPI going forward? A lingering question:

That’s okay, growth has our back, right? The story for the stock market will hinge on growth and it is clear we will have a soft landing and not a hard landing, right? On this front I have some … lingering questions

Leading Economic Indicators did tick higher as did the Building Permits data. Average weekly hours has been trending lower and recently the ISM New Orders to Inventory plummeted. I think there is something for both the soft and hard landing crowd in here, and given the soft-landing crowd is 76% of the market while the hard landing crowd is 12%, I wish it was a clearer picture. I still fear this growth data will get murkier and cause a great number to question themselves. Why? Well the aforementioned BA is cutting aircraft deliveries. That will shut down plants which have an impact on a lot of workers and the surrounding towns. Not just Boeing that had bad news. Look at FedEx. Alan Greenspan used to talk to Fred Smith the CEO of FedEx because he thought it was an important barometer. Pick your favorite large cap names that impact the economy. We typically don’t see this price action in a soft landing:

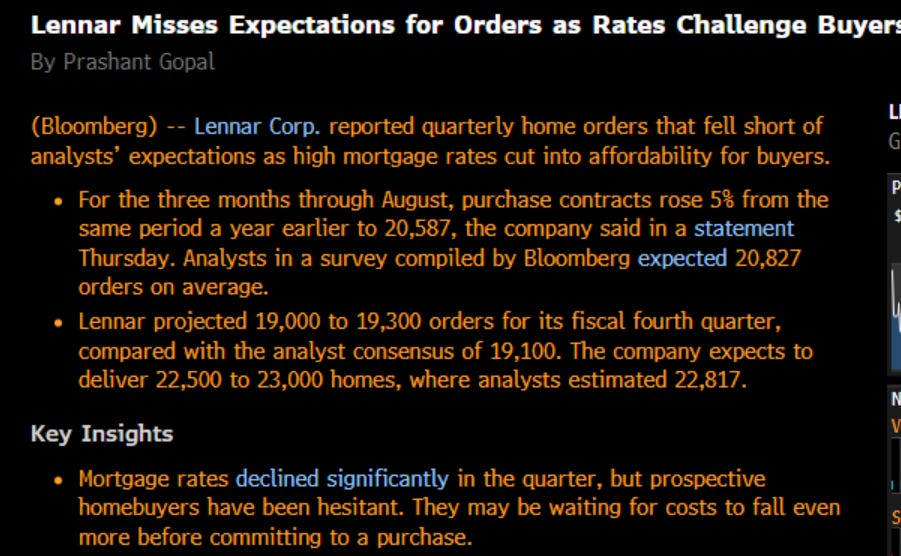

Another stock that had a really tough week was Lennar. We are excited about the impact of rate cuts on housing, but Lennar is telling us we are getting ahead of ourselves. You know how important I think housing is:

I could go on and on, but all I will be doing is adding more lingering questions to the discussion, which isn’t helping anyone. I will leave you with one final chart:

This is the 3-Treasury Bill yield which most can approximate in a money market account. In spite of the Fed cut, it still pays 4.8%. The blue line is the earnings yield on stocks, which went below cash yields in summer of 2023 and stays below. It is not asymptotic, but it does go to show that there is not only no margin of safety. The only other time we have seen this situation was the late 90s. Yes, it can last for a long time. It has persisted for over a year now. For me, I only want to invest in stocks when there is a clearer path toward growth, a clearer path on rates, a clearer path on earnings, and of course, more margin of safety in case I am wrong. Right now, none of those things are in place, so given these lingering questions, I am happy to sit in cash and wait for a fatter pitch.

Stay Vigilant

Thanks for reading Stay Vigilant! Subscribe for free to receive new posts and support my work.

Thanks for reading Stay Vigilant! This post is public so feel free to share it.

I agree. I'm not saying the bond market is wrong. I am saying the Fed disagrees and the Fed has a microphone. I think Fed and equities see a soft landing and bonds see a harder landing. Something has to give imho

Yep. I agree. The markets expects a hard landing while the Fed is still trying to convince us that they manufactured a soft landing. That’s the disconnect.

I’d fade the Fed before fading the army of rates traders. The gold story hasn’t changed although the drivers of that rally may have expanded.

At the start of the year, the army of rates traders had 8 cuts priced in for 2024 and within 3 months it was 2. Not sure market is always right

As new signals enter the market, good traders willingly change their position.

I agree. I'm not saying the bond market is wrong. I am saying the Fed disagrees and the Fed has a microphone. I think Fed and equities see a soft landing and bonds see a harder landing. Something has to give imho

Yep. I agree. The markets expects a hard landing while the Fed is still trying to convince us that they manufactured a soft landing. That’s the disconnect.