This is where it gets interesting

The bear market rally continues. What if it is more than that?

I have been spending more time on Twitter lately, focusing primarily on the markets-related Tweets. I still try to avoid the rabbit hole that is the political Twitterdom as it feels pretty unhealthy to me. However, there is good banter and dialogue on Twitter and it reminds me a little bit of my time on the exchange floor. You can learn a lot when you discuss ideas with smart people. You can even learn by listening in to these discussions. However, it is also pretty easy to get distracted by a lot of noise from other people that aren’t really adding.

I watched a dialogue between a couple of popular market-watchers where one referred to the move this month as ‘a bear market rally’. The other responded ‘what if this is a bull market rally?’ I chimed in and said ‘this is where it gets interesting’. You see, I have been in the bear market rally camp all along.

In fact, you can go back the last couple months and I have talked about how would develop as a waterfall decline. In “History Doesn’t Repeat But It Rhymes”, I looked at past market crises and spoke about this time of decline. In bear markets though, we can often get big rallies.

In “Fireworks” at the start of July, I spoke about how the dialogue and conversations were all getting more negative. Two weeks later in “Inflection Point” I spoke about the reactions to the negative headlines and how that was suggesting everyone had actually gotten far too bearish and pessimistic. This didn’t mean that the news was good, just that no one was left to sell. So we highlighted the possibility that we could get a rally based on the negativity and the price action. This has happened. Do we just go back out and re-load on the short side? Or has new information come out that we must digest first?

As the question was posed, what if this is something different though? Can we all be so sure? It is easy and common to have cognitive dissonance and interpret the news that we see in the ways to fit our views. This is human nature. We must fight that as investors. We need to stay as objective as possible. This is why we all must have a disciplined investment process. My process, as you may know, consists of the Fundamental, Behavioral and Catalysts. In order to answer the question posed, I need to go through the process. Take a ride with me.

Fundamentals

When I refer to the Fundamentals in this way, I am referring to the Fundamentals driving the economy. These in turn will drive all risky assets. Therefore, by assessing the state of the Fundamentals, we can determine if at it’s core, the economy is a head wind or a tail wind to taking risk. It can also help us determine if this is a bull market or bear market rally.

There has been quite the debate on whether or not we are in a recession. Frankly, it really doesn’t matter to me. I am not going to get caught up in the political fray on that because that is all the discussion is. The fact is, we have had two consecutive quarters of negative GDP growth. That is historically not a good thing. It has historically meant we are in or close to a recession. It has been historically bad for risk-taking.

Nothing about Covid and the post-Covid environment, with ‘unprecedented’ lockdowns and historic levels of fiscal and monetary stimulus is consistent with much of what we have seen before. Why should we expect this downturn to look like what we have seen before either?

Back in June I suggested that with the rampant travel and the housing & construction already underway, the multiplier from this spending could be enough to keep the economy strong through the end of the year. I thought 2023 would be when the economy might really slow. That is looking more likely.

The National Bureau of Economic Research gets to determine if we are in a recession or not ultimately. However, it usually takes its time and by the time NBER gets around to calling a recession, the market is already debating about the shpe of the recovery. That is why it is largely a moot point. It is worth understanding what factors it looks at to determine a recession, and how those are doing now. Why? Because this can tell us how bad a recession might be and what sectors might be able to navigate it better. The chart below from BofA indicates the variables NBER uses and how each of those has expanded this year. Jobs, income, spending are all looking healthy. Industrial Production quite so. This would suggest it might be a little early to be calling anything a recession. It argues that this might be leaning more to bull market rally.

I also like to speak to bankers. It is the bankers that extend credit to companies and consumers. Some might argue that during the GFC, bankers showed how out of touch they really were. However, the GFC was caused by bankers getting away from the core of what they do and they got burned. Bankers are now back to being boring (at work at least). The misallocated capital in this cycle, and there surely was some, probably resides more on the Fintech and Crypto balance sheets as they have been more aggressive trying to disrupt and take share. We have seen these implosions. Traditional bankers? They are quite content right now. Balance sheets are fine, they are still looking to extend risk and looking to add to their workforce. Not the sign of a recession. In fact, in the report on the latest Master Trust Data, where banks talk about their credit portfolios, S&P Capital IQ wrote:

“Bank executives said the elevated payments and lower credit losses signify the health of customers.

"You can see how resilient the consumer is in the U.S. through the elevated payment rates and the low level of credit losses," Citigroup CEO Jane Fraser noted during Citigroup's second-quarter earnings call.

Bank of America CEO Brian Moynihan, meanwhile, pointed out on Bank of America's recent earnings call that such elevated payment rates on credit cards complete the resiliency picture.

"That means people paying off their debt at a good clip," Moynihan said.

This is another tick in the column for an economy that may be a tailwind for the market. Where does this negative sentiment come from after all?

You actually don’t have to look too far. One reason I don’t get caught up in the GDP debate is that the GDP is all backward looking. This week we got Q2 GDP. So this just tells us that from April-June the economy contracted. It still might be revised. Either way, the market looks forward, not backward. That is why I prefer the ISM data. It is at least coincident with the SPX and can be more useful. This data comes out on Monday and could set the tone for the rest of the summer. If we look at some indicators that anticipate ISM - namely New Orders or the ratio of New Orders to Inventories - both would suggest the ISM will fall even more than the consensus is expecting. These are pointing to an ISM well below 50 or even 45. That would be a recession. ISM below 50 is the one time stocks have consistently negative returns. This worries people.

Another worrying piece of data that looks forward comes from the housing market. Pick your favorite negative chart and you have seen it on Twitter. Housing generates new orders which lead to profits and then employment. That is why it is so critical. Right now, there are more new homes being listed than being sold. When this has happened before, it has led to a recession (red shaded areas). Another mark against the economy. Another headwind.

Back to employment. Jobs have held up this year, expectially the non-farm payroll number. It is well-followed but also backward-looking and subject to revisions. That is why I like to look at other gauges, like ISM employment or jobless claims. While the job market has held up well and is still in positive territory, there are signs it is weakening.

I talked about travel possibily holding up the economy. If you look at the number of people going through TSA, we are back to 2019 levels. Unfortunately, the airports and airlines are staffed more like the lows of 2020 which is why we are seeing so many delays, cancellations, lost luggage and the like. But, I am sure you can tell from your own work environment, but I can also tell by the highway traffic and empty coffee shops, people are traveling. This means spending that can hold up the economy a bit longer.

Speaking of driving, there is nothing but construction everywhere. Credit the infrastructure bill delivering funds to blue states. Construction jobs mean money in peoples pockets that can also hold up the economy. It still looks healthy.

I have shown this before. This is nominal vs. real GDP. Yes, we have two negative GDP quarters in a row but this is in real terms. In nominal terms, GDP is still strong. As long as one’s wages are keeping up (not the case for many), this economy feels pretty good. If your wages are not keeping up, this feels pretty bad. I think this is why we are getting so many mixed signals. We have only had periods like this in the 40s and 80s. This is not the economy of the 21st century most investors are used to.

Summing up the Fundamentals section, I would say right now it is still holding on but is deteriorating. We need to see more signs that are positive and improving instead of positive but getting worse. The ISM data may seal it for us. Therefore, the Fundamentals are a headwind for risk, just not yet the major headwind many think.

Behavioral

Next I look at what I call Behavioral. It is trying to assess the supply and demand for risk-taking. I look at more indicators than I have here but in the interests of keeping this shorter, I will go through quickly.

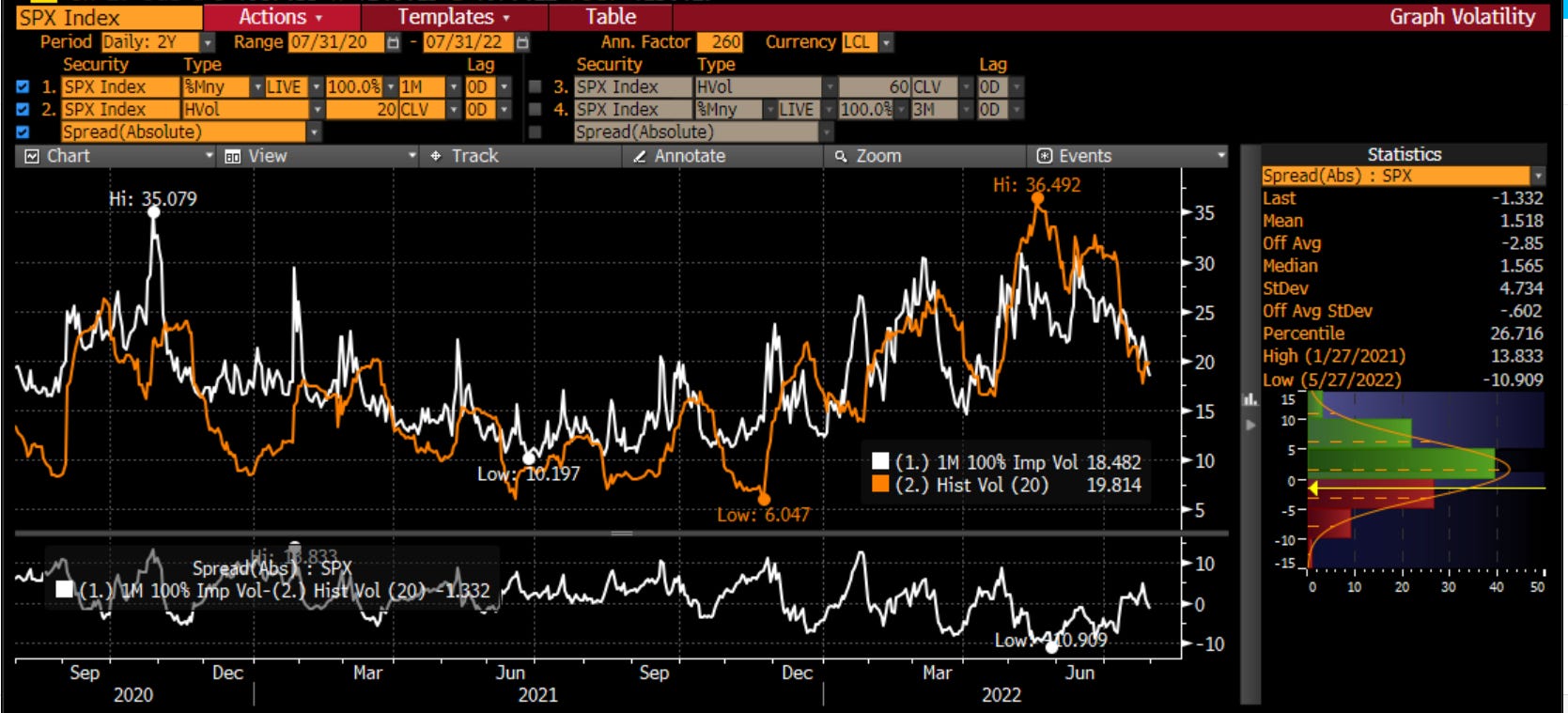

Implied volatility as measured by the VIX Index gives us an idea of how nervous investors are. It is a measure of the risk premium people will pay for insurance to protect their portfolios. The curve is normally upward sloping as we go out in time. When it inverts, and the cost for insurance is more expensive in near dates, that means the hurricane is about to hit shore. I measure this with the VIX Curve Index. Right now, it is giving very normal and boring readings suggesting to me neither euphoria or panic.

Another way to assess if there is panic or complacency is to compare the level of implied volatility to the actual (or realized) volatility in the market. When the spread is wide, there is more concern. Right now, there is none. This doesn’t suggest complacency, simply fair values.

Finally, the implied volatility across asset classes tends to move together for reasons I discussed before. Currently, fears and nervous are elevated in the FX and Interest Rate markets, but more subdued in the equity and credit markets. Said another way, the macro markets are nervous but the idiosyncratic markets are not. Neither is smarter than the other, but this does show these two pools of investors are out of synch.

I can also look at the number of puts vs. calls trading in the market. I smooth this over 1 month but when this number is rising, it means more insurance being bought. When it is falling, investors are looking to add risk back on. It has started to fall again.

Technical analysis is very useful for staying objective. Price is the intersection of supply and demand. There is no right or wrong, there just is. On the daily charts, the equity market is near resistance levels and looks to be trying to break out. However, I am worried it is doing that from an already extended level as we can tell from the MACD and RSI in the bottom two panels.

That said, the weekly charts are looking quite good. The lagging span in the cloud held support, the MACD is turning up and we are comign off oversold levels. This is a good looking chart.

However, if I go to the monthly, I get a very different view. I see a negative pattern as the chart has rolled over and the MACD turned lower. Collectively, this would tell me that if I bought stocks here, it would be in small amounts and as a trade and not an investment.

Looking at other markets, the 10 year yield has formed a head and shoulders pattern. Measuring this, it points to a move to about 1.95-2%. This would clearly only happen if we were seeing negative economic news and a Fed that was slowing down its rate hikes. It would add credence to the economy and earnings slowing but might help support equity multiples. This is a chart that gets macro investors beared up on risk.

Let me add to the confusion though. Copper, which is closely tied to the economy given its uses in housing, autos and the electrifcation of the economy, had a tough Q2 but the chart here is showing some possibility of near term upside.

If I look at the Bloomberg Commodity Index, all commodities are showing this same strength. This does not suggest the economy or inflation are falling too much.

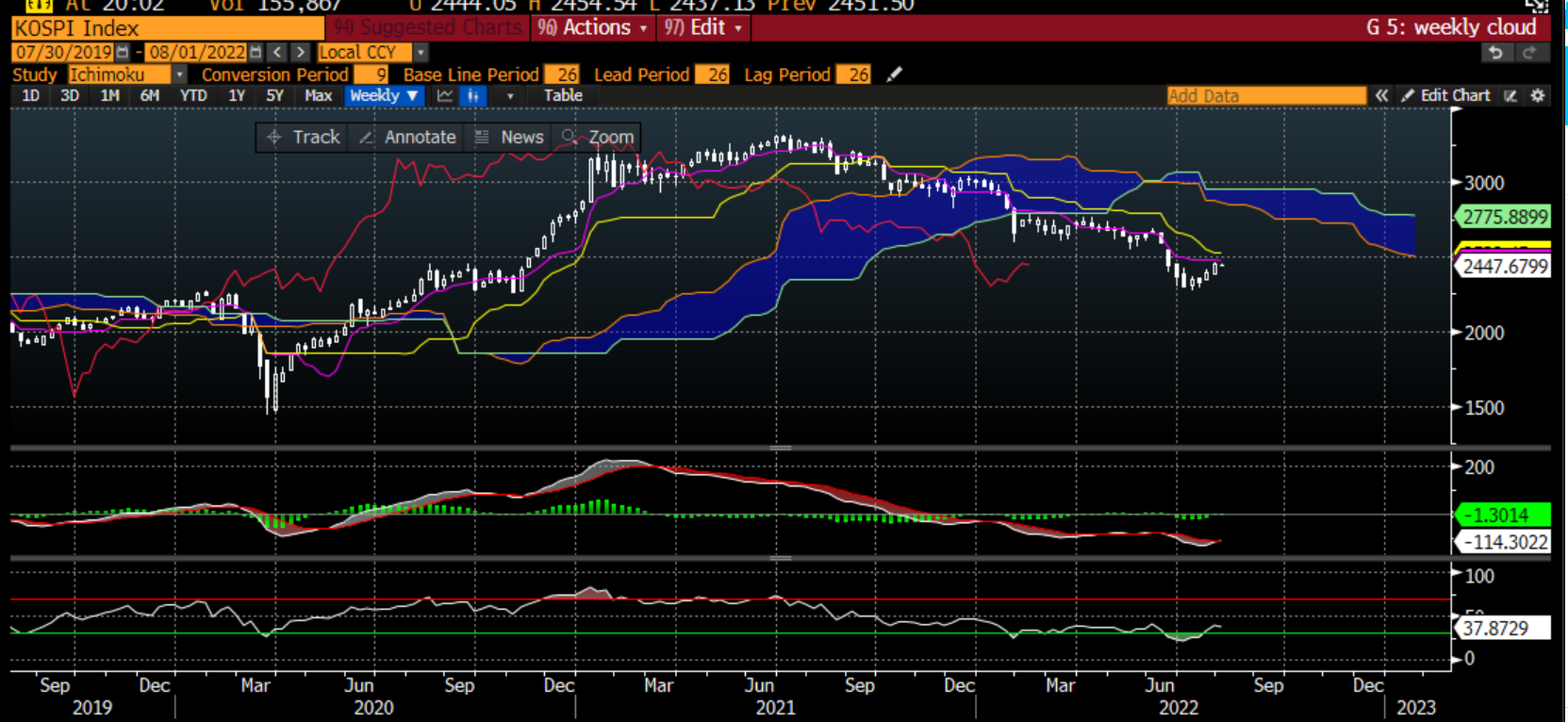

Emerging markets stocks are also very economically senstive. They have been under siege this year. The Kospi in Korea is the best one to follow given its global cyclical focus. There are signs of life on the weekly chart.

Another good measure of sentiment is the Bloomberg Crypto Index. It has led tech stocks lower. Its weekly chart is also turning up and could be good for a rally here.

Pulling together, there are more good signals than bad signals. There is scope for a rally in many of the risk indices, especially on a weekly basis. The daily looks stretched in some places so you can probably get in cheaper. Also, the longer term trends are rolling over. This suggests caution as we look at the end of the year. For now, over the next month or two, it is a good sign.

Catalyst

The last section looks at catalysts - what gets people to change their minds. We had a major week of earnings this week. I have the charts below to show but I will let CS summarize for you:

With 80% of TECH+ market cap having reported (including 5 mega caps – AAPL, MSFT, AMZN, GOOGL, META), earnings are marginally missing expectations by -0.1% for the group. By contrast, the rest of S&P 500 are beating bottom-line by +5.8%.

2Q expectations are for revenues and EPS growth of 11.9% and 6.7%. Ex-Financials, these jump to 14.2% and 15.6%. Consensus projections are for EPS growth of +59.8% for Cyclicals, +2.5% for Non-Cyclicals, -5.3% for TECH+ and -21.6% for Financials.

67.5% of the S&P 500's market cap has reported. Earnings are topping consensus by 4.0%, with 70% of companies topping projections. EPS is on pace for 8.0%, assuming the current beat rate for the rest of the season.

Value is delivering stronger revenue and EPS growth (12.9% and 15.2%) than Growth (9.5% and -1.5%). Margins are growing faster in Value in 10 of 11 sectors vs. Growth. Value results are surpassing estimates by 4.7% vs. 3.1% for Growth.

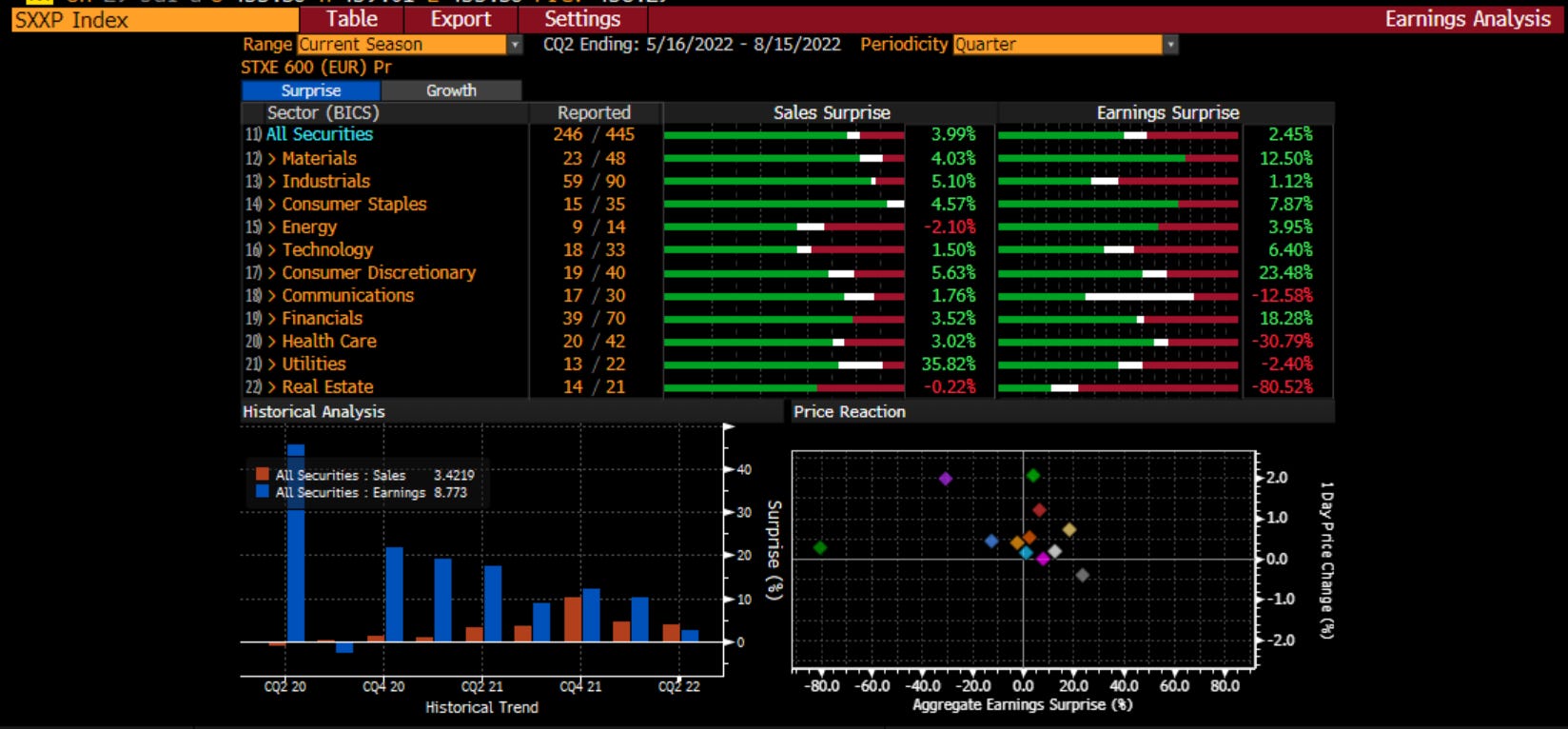

EAFE is delivering higher revenue and EPS growth (13.5% and 12.3%) vs. the U.S. (11.9% and 6.7%). EAFE results are topping estimates by 8.6% vs. 4.0% for the U.S.

More globally-oriented S&P 500 companies are delivering faster EPS growth than their more domestically-oriented peers: 17.7% vs. 13.0%.

Companies beating on both revenues and EPS are outperforming the market by +1.3% vs. an average of +1.7%, while ones missing on both are underperforming by -2.1% vs. -3.1%.

2Q earnings trends are quite solid, with EPS revisions running 1.1% above their historical trend (negative revisions prior to reporting season followed by positive beats).

This is the picture for the US:

Europe:

Kospi (not enough companies have reported in China or Japan yet)

Earnings lead stocks. Have you heard that anywhere? Well, if we look at the actual SPX eps being reported vs the total return of the index, we can see that there is a disconnect. The expectation coming into the quarter was that the earnings number would fall to catch up with the market. It has not. Does this mean the market has some catching up to do?

Last thing to look at is the economic surprise data. I look at US, Europe, China and the Global Index below. These indices are mean-reverting by nature. These indices are all starting to move higher. This would suggest seeing a series of economic releases that are better than expected. If we start to see that on top of the earnings coming in better, what will investors do?

I set out to determine if what we are seeing is a bull market or bear market rally. I also wanted to see if this rally had further legs to it. After looking through the indicators in my process, I still come out that this is a bear market rally. The Fundamentals are weakening. Perhaps not as fast as many had hoped. They may hold up through the end of the year and not collapse until 2023. This would just keep the Fed in play though. If the Fundamentals are not strong, we cannot have a bull market.

However, that doesn’t mean we can’t rally. Looking through the Behavioral, while we have surely taken out some of the most pessimistic traders, people still seem offsides. Real money investors are underweight equities. Some may have panicked out of their commodities. The prices in these are showing the signs of a bottom. How does a hedge fund react if the news keeps coming in incrementally better and they are still short? How does an RIA act if the market is up 13% from the lows and they have their clients in cash. When the client is back from vacation, will they be happy?

The ISM tomorrow will be telling. If it does not slow as expected, the market could be set up for another good month into Jackson Hole. If it is weak, combined with some stretched short-term charts, we could see a pull back in risk. However, we have to respect that this will also add to the Fed pivot narrative and this dip might be bought until the Fed disappoints.

I vote bear market rally. I still vote waterfall decline. However, I think the real selling shouldn’t be done until we are at higher levels than now. Be careful in your investing. This is a very tactical and short-term market. This is not a market to be making big calls. It is ‘interesting’ as I said.

Stay Vigilant.

Excellent write up!

I believe the rally will be driven by large tech earnings (Apple, Microsoft). I like your travel component and agree that it is an economic driver that will fall off in the near future.

I do not believe real positive economic change can happen without oil falling.

I do not understand how gold and silver have declined while the dollar has weakened.

I do not know if the gdp numbers are adjusted for inflation.