Warsh. Rinse. Repeat.

We talked before about how important the signal from the new Fed Chair would be. It may be even bigger than we thought.

Two weeks ago, in my post called What is the Common Thread?, I wrote:

“Kevin Warsh in now the new Fed Chair and has his first meeting next week. Inflation and growth are clearly going to be the focus, as they always are. The market will be intently focused not on what the FOMC will do (there is no move expected), but more importantly on the commentary toward how the FOMC now sees the jobs and inflation backdrop. Concern on inflation will be negative for rates, stocks, gold and crypto. Concern on growth could be negative for stocks and commodities but positive for rates and may give a relief to gold and crypto. Are Kevin Warsh and the Fed now the common thread that is weaving through the markets? I think so.”

In the week since his first meeting and press conference as Fed Chair, the markets are responding even more than they were, and there is a new appreciation for what Kevin Warsh may mean for markets going forward.

It is neither all bad, nor all good. It is different. Different isn’t always bad, though it takes some period of adjustment when we are confronted with different. All investment processes should be disciplined, but also adaptable. There should be elements that are ‘non-negotiable’ such as asset classes traded, sectors, styles etc. However, there should also be parts that adapt to changing market circumstances, or new investment regimes.

Once we get used to the new normal, and embed in our process, we need to make sure we continue to iterate over and over. As the meme goes, we need to Wash, Rinse and Repeat. For the current environment, we may need to Warsh, Rinse and Repeat.

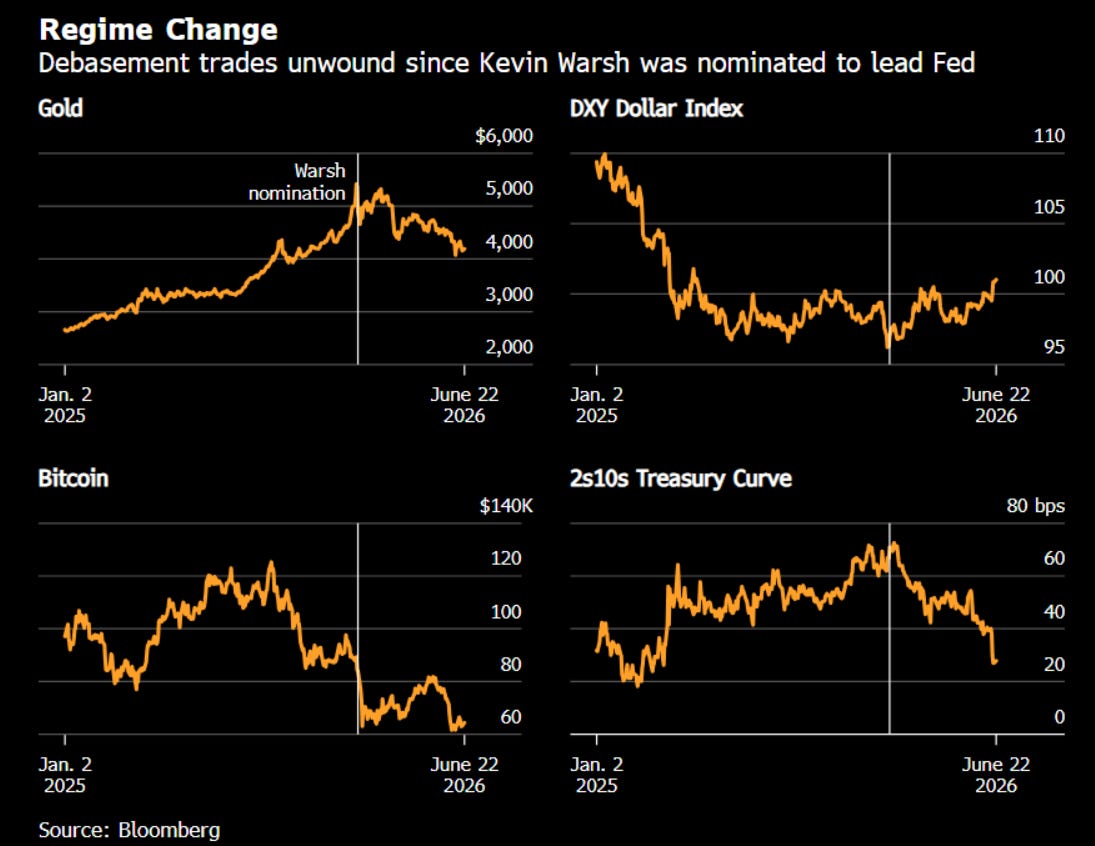

Debasment, what debasement?

Bloomberg had an article today that laid out how the popular debasement trade of the last few years has been under siege this year. It was not uncommon to hear, and for me to write, that the Dollar was at risk and this could lead to a flow of money out of US assets and into global assets. My how things have changed.

Per Bloomberg:

“(Bloomberg) -- In hindsight, the beginning of the end for the debasement trade can be traced back to Jan. 30. That’s when US President Donald Trump nominated Kevin Warsh to lead the Federal Reserve, prompting investors to reassess the popular macro play centered on diversifying away from the dollar. Gold tumbled as much as 13% that day from an all-time high, its steepest decline in more than four decades, while Bitcoin subsequently collapsed. The greenback found a bottom after a prolonged slide.

While Warsh got the nod from Trump by advocating for lower interest rates, it was his prior reputation as an inflation hawk that stuck in many investors’ minds. And it introduced enough doubts about which direction he would take to cause some of them

to hedge their bets when he was named.”

Put even more clearly, there is a quote in the article:

“Anyone who thinks that he is some kind of a stooge that’s been put in there to cut interest rates regardless of inflation is going to really, really be disappointed with Kevin Warsh,”said Gavyn Davies, co-founder and chairman of Fulcrum Asset

Management and a former chief economist at Goldman Sachs Group Inc. “He’s not that kind of chair.”

They show the movement in certain markets that highlights this change in market mindset:

Gold in particular is starting to look broken, now trading below the 1-year moving average and seeing relentless selling pressure and ETF outflows since earlier this year:

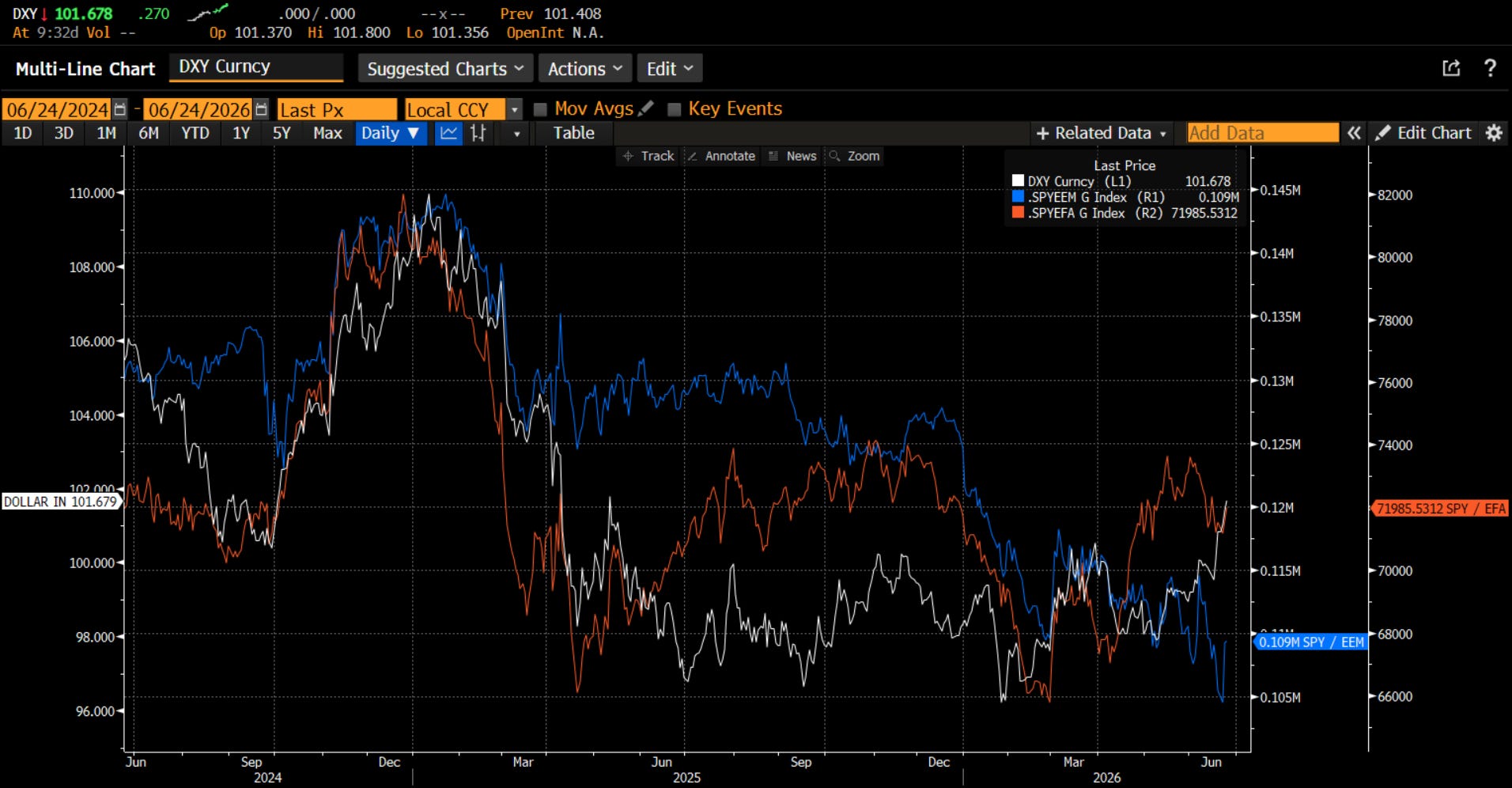

The move lower in the Dollar coincided with international stocks outperforming US stocks in 2025. As the Dollar is turning around, is it time for US stocks to assert their leadership again?

In his latest “Eye on the Market” podcast/report, JP Morgan Asset Management Vice Chair Michael Cembalest discussed the US stocks vis a vis the rest of world. It is clear JP Morgan is telling the clients to focus on the US:

This has implications particularly for the favored emerging markets, which until this week were markedly outperforming the US, led by the favored Korean market which MSCI just affirmed as an emerging market. While the KOSPI dropped by 10% on Monday, it is still up 88% this year alone. In addition, SK Hynix just announced a massive offering of ADR’s. Top of the market anyone?

What is changing?

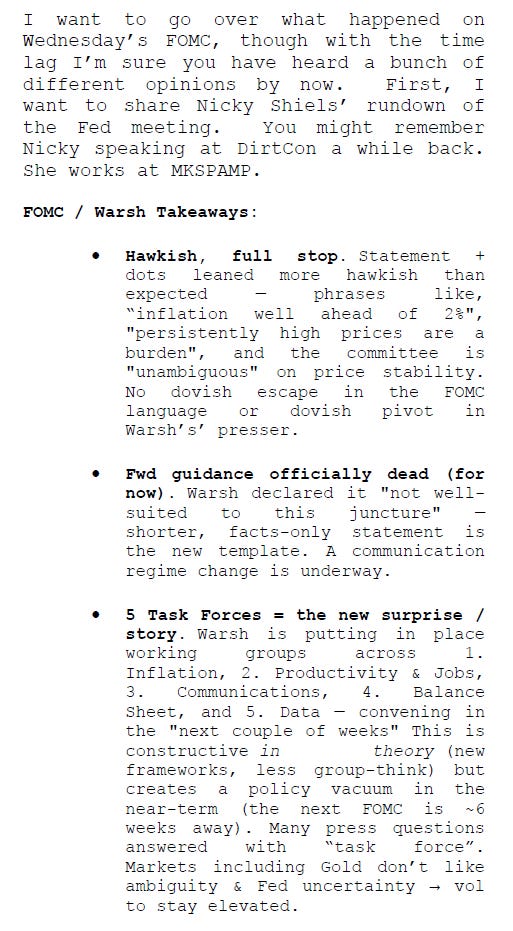

When I have questions about the bond market price action or what the bond market is thinking, I make sure to read Barry C. Knapp at Ironsides Macro. Barry is incredibly experienced, connected and articulate. He wrote a piece on the weekend after Warsh’s first meeting called “Uncle Milty’s Revenge” and in it he wrote:

“Friedman’s Revenge

The bottom line: the sharp bear flattening of the Treasury curve, presumably due to a hawkish DOT plot that is living on borrowed time, as well as Chairman Warsh’s commitment to the Fed’s stable price mandate, like the reporters in the room, completely missed the implications of eliminating forward guidance, shrinking the balance sheet and shortening the duration of the System Open Market Account portfolio, integrating market prices into economic forecasting, and a greater emphasis of supply side economic analysis on their employment mandate and inflation forecasts.

The Fed is not going to hike the policy rate. If our forecast for a resumption of disinflation later this summer is early or less likely, directionally incorrect, the Fed is more likely to respond by tightening using their balance sheet. 2s are a buy and the curve will bull steepen. We’ve been critical of the FOMC’s lack of capital markets expertise, and inability to integrate market signals into their forecasting process. A stark example was the reaction to Trump Administration tariffs, the market message was unequivocal, tariffs were a bigger risk to growth than inflation, yet the Fed focused on the first order price effect. The same is true with the Iran War and energy spike, our first chart below shows the breakeven inflation curve below where it was in September before they cut the policy rate.

The unspoken objectives of the five task forces are to reduce the Fed’s footprint and shift power to determine the cost of capital back to markets or what Hayek called the spontaneous economic order. This was an exceptionally consequential meeting, the most important since the launch of QE2 in November 2010 when the Bernanke Fed took a crucial step towards what Treasury Secretary Bessent called gain of function monetary policy.”

Jared Dillian who writes “The Daily Dirtnap” and is a former Lehman colleague of Barry’s thinks Warsh was more hawkish even. He wrote in his newsletter this week:

Tyler Neville on X.com shared this video from Warsh’s press conference:

As Tyler says, “am I hearing this right?” Warsh wants the Fed to respond to markets, not the market respond to the Fed. This is a subtle but MASSIVE difference. As Barry wrote, Warsh wants to eliminate forward guidance, which Bernanke started on Warsh’s last stint at the FOMC and that has continued with subsequent Fed Chairs. We are headed to a return to the days of Alan Greenspan (may he rest in peace). This has enormous implications for forward pricing and volatility.

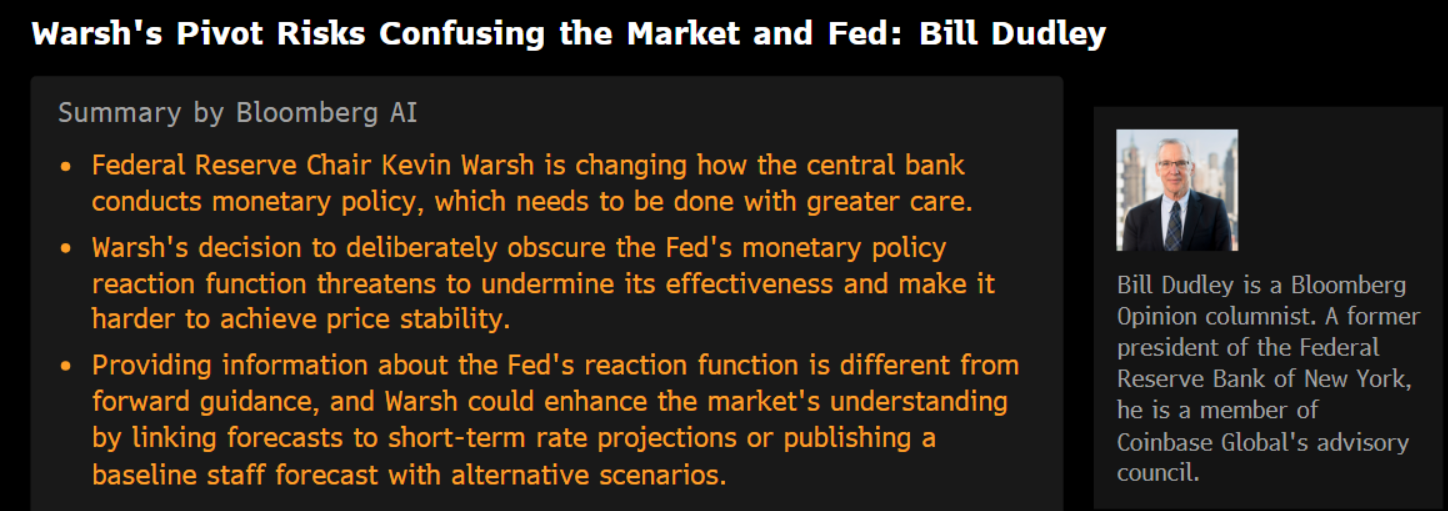

Not everyone is a fan of this new policy. Bill Dudley, a former President of the NY Fed, thinks this ‘decision to deliberately obscure the Fed’s monetary policy reaction function’ will make it ‘harder to achieve price stability’.

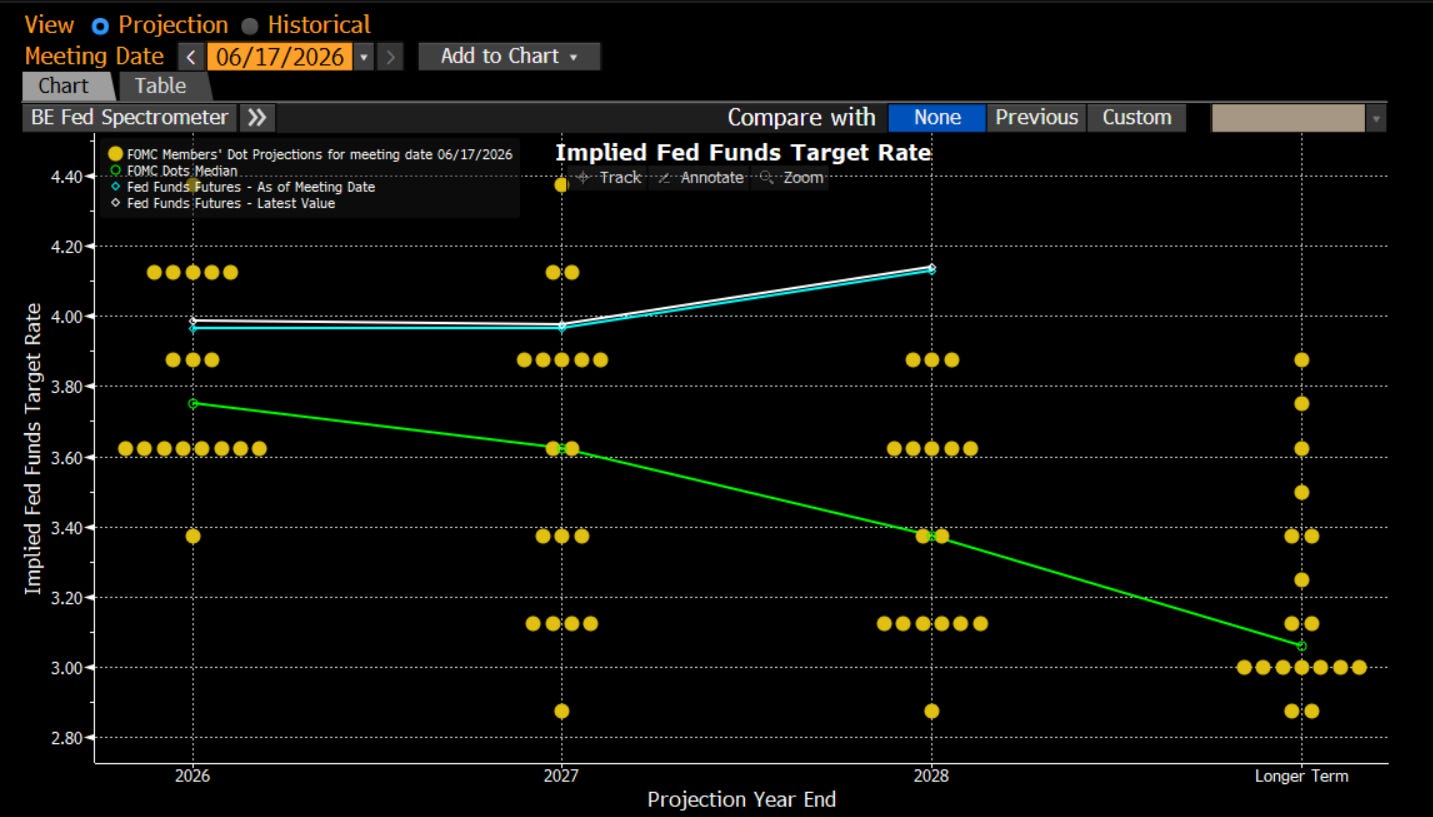

We shouldn’t be surprised, then, that there is considerable difference of opinion about the path of rates going forward, not as much in the market, but on the FOMC itself. The Fed dot plots, which are updated each quarter, show an even split between hawks and doves. Noticeably one dot, presumably Warsh’s, is missing.

With an even split about the path of rates, it is unlikely to see the rate hikes that the market is now fearing. However, as Barry laid out, price stability is still of the essence. The tightening of policy will more likely come from the shrinking of the Fed’s balance sheet. The balance sheet is laid out as an additional focus for the task forces. Warsh isn’t dumb. He knows how organizations work and how the FOMC itself works. He will need buy-in to achieve his objectives and the way to do this is to get the FOMC research staff to support his ideas with their research. Watch for the reports from these task forces.

What does this mean for markets?

I showed above that gold, and by extension other precious metals, are under siege. The link with real rates has returned and real rates are likely headed higher, not lower. This is not good for gold. If it is a core holding of your portfolio as it is for many, you may want to look to generate some income by over-writing if you hold it via ETF or futures. If you hold it via physical, that is more difficult for sure. Be ready for some price pressure. However, in the grand scheme, the relative performance of gold vs. the SPX looks about normal, and I would expect it to stay this way:

The bond market is likely the most interesting place to look. I agree with many that Warsh may be more hawkish than anyone anticipated. However, I also don’t think this comes via rate moves, not the least of which is because the FOMC won’t want to appear too political. They will need to wait for data on the twin forces of commodity supply chain shock inflation and AI disinflation. By the time that get that, it could be the September meeting and that is far too close to the election. The market is pricing in a full rate hike. The 2-year bond looks like it might be a buy as Jared discusses, but as I wrote for the CME this week, SOFR futures for this year may be the best trade on this. As always, do you own homework. You may not even be able to trade these:

Importantly for other markets, though, is the 10-year yield. I have discussed the “line in the sand” that my co-host Tony Zhang and I discuss on our ‘Macro Matters” podcast. The market tried to breach that level. However, since Warsh was approved by Congress in the 3rd week of May, the yield has only gone lower and is below the line in the sand. While the FOMC unwinding its balance sheet could be seen as negative, this will likely take some time (we need the research to support it). So, for now, as Warsh builds credibility on his price stability focus, expect lower yields and lower yields should be supportive of riskier assets

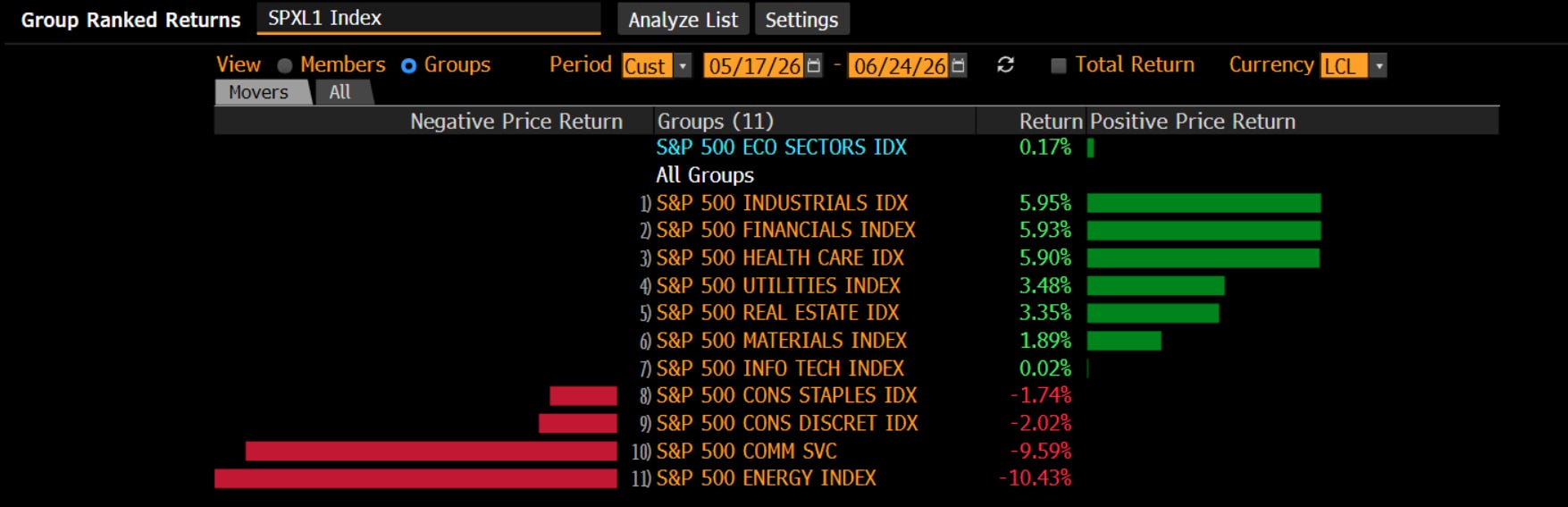

The equity market is trying to find its footing about what a new, hawkish Fed Chair could mean. I might suggest there are a lot of crosswinds. First, he is likely not hawkish on rates (good) but is hawkish on balance sheet reduction (bad). Second, lower yields mean multiples could expand (good); however, lack of forward guidance means uncertainty and volatility, and this would pressure multiples as it dampens investor enthusiasm (bad). Finally, a focus on price stability is good because of what it means for margins. This should support earnings, which we have discussed is the most important driver of markets. Since Warsh was confirmed, the market is flat. The AI theme has seen profit-taking. The Iran War energy trade is under-pressure. However, the companies expected to show earnings growth in the coming quarter are starting to rise to the top. Look at Industrials, Financials and Healthcare leading the way. I showed last week the performance of Momentum vs. Low Volatility. The relative performance in the last month has been pretty flat. Investors look to be, at the very least, bringing their portfolios back into line a bit before quarter end.

It may be time to prepare your portfolio for the coming earnings season and set it up for the rest of the year. It is certainly time to consider how you need to adapt your process for the new Fed Chair Warsh. Only then will you be comfortable to Rinse and Repeat in your investing.

Stay Vigilant

Great piece - I agree that the rate regime will be very tricky (different) from here on out very likely - lest the U.S. go bankrupt quicker than they can manage to gradually increase inflation.

Very well expressed. I have been of similar views myself. I think a rate hike is highly unlikely, in fact a smaller balance sheet and rate cut by year end is entirely possible.